El derecho de sucesiones en el Islam, también conocido como Mirath, es un sistema bien definido que tiene sus raíces en el Corán y los hadices. Establece cómo debe distribuirse el patrimonio de una persona fallecida entre sus herederos.

Las normas están diseñadas para mantener la equidad, proteger a los miembros de la familia y mantener el equilibrio social.

Comprender estas normas es esencial tanto para los musulmanes como para quienes se ocupan de la herencia islámica como parte de la planificación patrimonial global.

Este artículo trata:

- ¿Cómo se divide la herencia en el Islam?

- ¿Quién tiene derecho a la herencia en el Islam?

- ¿Reciben los hijos más herencia que las hijas en el Islam?

- ¿Se puede renunciar a la herencia?

Principales conclusiones:

- El derecho islámico de sucesiones protege a los miembros de la familia y evita disputas.

- Los hombres suelen recibir mayores participaciones; las mujeres, protección financiera.

- La herencia sigue cuotas fijas, asignación residual y ajustes de ‘lezna.

- Los herederos pueden renunciar voluntariamente a su parte sin vulnerar los derechos de los demás.

Mis datos de contacto son hello@adamfayed.com y WhatsApp +44-7393-450-837 si tiene alguna pregunta.

La información contenida en este artículo es meramente orientativa. No constituye asesoramiento financiero, jurídico o fiscal, ni una recomendación o solicitud de inversión. Algunos hechos pueden haber cambiado desde el momento de su redacción.

¿Qué es la regla de la herencia en el Islam?

La regla de la herencia en el Islam se basa en el principio coránico de que cada heredero recibe una parte fija del patrimonio. Estas partes se determinan en función de las relaciones familiares y de la presencia de otros herederos.

La herencia islámica se divide principalmente entre herederos primarios (como cónyuge, hijos, padres) y secundarios (hermanos, abuelos o parientes lejanos si faltan los primarios).

Entre los principios clave figuran:

- El patrimonio se distribuye de forma justa y proporcional.

- En determinadas circunstancias, los herederos varones suelen recibir el doble que las herederas mujeres.

- Una persona fallecida no puede anular la asignación coránica, aunque puede hacer testamento para destinar hasta un tercio de su patrimonio a no herederos o fines benéficos.

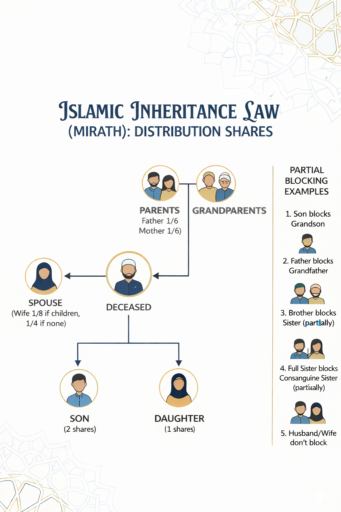

¿Qué es la Regla 14 de la Herencia en el Islam?

En la herencia islámica normas de bloqueo total, Artículo 14 establece que el padre del padre (o el padre del padre del padre, por muy alto que sea) impide que los hermanos maternos hereden.

Entre los hermanos maternos se incluyen hermanos y hermanas maternos.

Cuando existe un ascendiente paterno, los hermanos maternos quedan totalmente excluidos de la herencia.

La regla 14 es una de las dieciséis reglas de bloqueo completo (numeradas de la regla 0 a la 15) utilizadas en las tablas de bloqueo de herencia (ḥajb) del islam suní.

Estas normas determinan cuándo determinados herederos quedan totalmente excluidos debido a la presencia de parientes más próximos o prioritarios.

También hay cinco situaciones reconocidas en las que se aplica el bloqueo parcial, lo que significa que la parte de un heredero se reduce pero no se elimina.

- Marido: Su parte disminuye de 1/2 a 1/4 si el fallecido deja hijos o nietos por línea masculina, independientemente de la distancia generacional.

- Esposa: Su parte se reduce de 1/4 a 1/8 cuando existen hijos o nietos de línea masculina.

- Madre: Su parte baja de 1/3 a 1/6 en presencia de hijos, nietos o hermanos múltiples de cualquier categoría.

- Hija de hijo soltero: Su derecho disminuye de 1/2 a 1/6 cuando está presente una hija soltera del difunto.

- Hermana paterna soltera: Su parte se reduce de 1/2 a 1/6 si existe una única hermana de pleno derecho. Esta reducción no se aplica cuando hay una hija o la hija de un hijo, ya que la hermana paterna se convierte entonces en Asaba, heredando una parte variable en lugar de una parte fija.

Por lo que respecta a la abuela (materna o paterna, sea cual sea su altura), o hereda la parte que le corresponde o queda totalmente excluida.

Las reducciones causadas meramente por el número de herederos no se clasifican como bloqueo parcial, por lo que las abuelas no se incluyen en esta categoría.

¿Por qué es importante la ley islámica de sucesiones?

El derecho islámico de sucesiones es importante porque garantiza un reparto justo, estructurado y ejecutorio del patrimonio de una persona fallecida.

Sirve para varios propósitos clave:

- Protege a los miembros de la familia garantizando a los padres, cónyuges e hijos las partes que les corresponden.

- Evita disputas mediante normas claras y predefinidas que limitan los conflictos entre herederos.

- Promueve la justicia social impidiendo la asignación arbitraria o el favoritismo.

- Preserva el patrimonio familiar apoyando la sucesión ordenada y la continuidad de los activos.

Este marco es especialmente pertinente para las familias musulmanas con bienes en varias jurisdicciones, donde la claridad y la coherencia son esenciales.

¿Cómo calcular la herencia en el Islam?

En el Islam, la herencia se calcula identificando a los herederos, aplicando las cuotas coránicas, ajustando el exceso mediante el ‘awl’ y distribuyendo las porciones residuales.

El proceso consta de varios pasos:

1. Identificar a los herederos - determinar los herederos primarios y secundarios.

2. Determinar las cuotas fijas - consultar las asignaciones coránicas para cónyuges, padres e hijos.

3. Aplicar el principio del ‘punzón’ si es necesario - ajustar las partes proporcionalmente si el total supera el patrimonio.

4. Asignación de cuotas residuales - distribuir los bienes restantes entre los herederos varones o los parientes más cercanos.

Las calculadoras y los programas informáticos modernos pueden ayudar a calcular con precisión las acciones según los principios de la sharia.

Supongamos que un hombre fallece dejando:

- Esposa

- Madre

- 2 Hijos

- 1 Hija

- Propiedad por valor de $120.000

Paso 1: Identificar a los herederos

- Herederos principales: esposa, madre, hijos, hija

Paso 2: Determinar las cuotas fijas (asignaciones coránicas)

- Esposa: 1/8 (porque existen hijos) → $15.000

- Madre: 1/6 → $20.000

Paso 3: Aplicar el ‘punzón’ si es necesario

- Patrimonio restante = $120.000 - ($15.000 + $20.000) = $85.000

- Hijos e hijas se reparten el resto, y los hijos reciben el doble que las hijas.

- Proporción total de acciones: 2 hijos : 1 hija = 2 : 2 : 1 = 5 partes

- Valor por pieza = $85.000 ÷ 5 = $17.000

- Cada hijo = 2 × $17.000 = $34.000

- Hija = $17.000

Paso 4: Asignación de participaciones residuales

- Totalmente distribuido:

- Esposa: $15.000

- Madre: $20,000

- Hijo 1: $34.000

- Hijo 2: $34.000

- Hija: $17,000

¿Quién recibe más herencia en el Islam?

Por lo general, los hijos varones son los que más herencia reciben en el Islam, ya que reciben el doble que las hijas.

Con ello se pretende reflejar su responsabilidad económica dentro de la familia.

Los maridos supervivientes también pueden recibir partes sustanciales si la esposa no deja hijos, mientras que las partes de los padres son fijas pero menores en relación con los descendientes varones.

¿Por qué las hijas reciben menos herencia en el Islam?

Las hijas reciben menos herencia que los hijos porque las normas islámicas sobre la herencia tienen en cuenta las responsabilidades financieras.

Se espera que los hombres mantengan a la familia, incluidas las esposas, los hijos y los familiares dependientes.

Las mujeres, aunque reciben una parte menor, obtienen protección financiera e independencia sin obligaciones familiares directas, lo que equilibra el reparto en la práctica.

¿Se puede renunciar a la herencia en el Islam?

Sí, un heredero puede renunciar voluntariamente a su herencia, total o parcialmente.

Esta renuncia puede hacerse con fines benéficos o para resolver disputas familiares, pero debe hacerse libremente y por escrito.

Es importante destacar que la renuncia no puede vulnerar los derechos fijos de otros herederos, ya que la ley islámica protege sus partes prescritas.

¿Hay que seguir la herencia islámica?

Sí, los musulmanes están obligados a seguir las normas islámicas sobre herencia, aunque su aplicación puede variar en función del derecho civil local.

Los musulmanes están obligados legal y religiosamente a seguir las normas islámicas sobre la herencia, especialmente en lo que respecta a las partes fijas señaladas en el Corán.

Sin embargo, en los países en los que rige el Derecho civil en materia de sucesiones, la aplicabilidad depende de la legislación local.

Los no musulmanes no están obligados a seguir estas normas.

Derecho islámico de sucesiones frente a sistemas civiles de sucesiones

El derecho islámico de sucesiones difiere fundamentalmente de la mayoría de los sistemas de derecho civil occidentales en el grado de libertad que tiene una persona para distribuir su patrimonio.

En el derecho islámico, la herencia es en gran medida obligatoria y basada en fórmulas, con partes fijas prescritas por el Corán para herederos específicos.

Un musulmán sólo puede asignar hasta un tercio de su patrimonio mediante testamento, e incluso entonces, generalmente no puede beneficiar a los herederos existentes.

Esto limita drásticamente la discrecionalidad, pero garantiza resultados predecibles y la protección de la familia.

En cambio, muchos sistemas de derecho civil y de common law permiten una amplia libertad testamentaria.

A menudo, los particulares pueden legar sus bienes a quien deseen, con sujeción únicamente a unos límites. normas sobre herencia forzosa (como los de algunas partes de Europa).

Esta flexibilidad puede aumentar las opciones de planificación, pero también aumenta el riesgo de disputas, desheredación y resultados desiguales.

Para los musulmanes que viven en jurisdicciones no islámicas, esto crea una tensión práctica.

Los tribunales civiles pueden aplicar por defecto el derecho sucesorio local a menos que la herencia islámica esté claramente documentada y legalmente reconocida mediante un documento válido. se, fideicomiso conforme a la sharia o las normas aplicables en materia de elección de la ley aplicable.

Sin una planificación adecuada, las herencias pueden distribuirse de forma contraria a las obligaciones religiosas.

Adaptar los principios islámicos de sucesión a los marcos jurídicos locales requiere a menudo una estructuración proactiva para garantizar tanto el cumplimiento religioso como la exigibilidad legal, especialmente cuando los activos abarcan varios países.

Conclusión

El derecho islámico de sucesiones es más que un conjunto de normas. Es un sistema diseñado para promover la justicia, la responsabilidad y la armonía en las familias.

Al definir claramente las partes, dar prioridad a los herederos y permitir ajustes mediante mecanismos como el ‘lezna, equilibra la equidad con las obligaciones financieras prácticas.

Comprender estos principios ayuda a las familias a gestionar la herencia sin problemas, evitar disputas y garantizar que se preserva la riqueza de forma responsable para las generaciones futuras.

Preguntas frecuentes

¿Cuáles son los impedimentos para heredar en el Islam?

Un heredero no puede heredar en el Islam en circunstancias específicas, entre ellas: asesinato intencionado del difunto, abandono del Islam (apostasía), muerte simultánea con orden incierto, li'an (negación de la paternidad mediante juramento coránico) y esclavitud.

En raras ocasiones, también puede restringirse la herencia en un matrimonio de urgencia si el fallecimiento se produce por enfermedad antes de la recuperación total.

¿Cuál era el derecho de sucesión preislámico?

En la Arabia preislámica, la herencia se regía por las costumbres tribales y favorecía a los parientes paternos varones, a los herederos adoptivos y a los aliados tribales, mientras que excluía a las mujeres y a los menores.

El Islam reformó este sistema estableciendo cuotas fijas para mujeres y niños y protegiendo los derechos de las viudas.

¿Cuál es el concepto de lezna en la herencia islámica?

‘Awl es un ajuste correctivo que se aplica cuando las cuotas fijas totales superan el patrimonio.

En estos casos, las participaciones se reducen proporcionalmente para ajustarse al patrimonio disponible sin violar los principios de equidad.

¿Qué es el derecho de sucesión suní?

El derecho de sucesiones suní aplica las normas coránicas de partes fijas y reparto residual, interpretadas a través de las cuatro escuelas suníes: Hanafi, Shafi'i, Maliki y Hanbali.

Aunque los hijos suelen recibir el doble que las hijas, y los cónyuges y los padres tienen partes fijas, cada escuela difiere ligeramente en el cálculo de las partes, el tratamiento de los parientes lejanos y la aplicación de ajustes como el ‘lezna cuando el patrimonio es insuficiente.

La ley suní garantiza que los herederos reciban las partes que les corresponden con justicia y claridad en virtud de la sharia.

¿Le duele la indecisión financiera?

Adam es un autor reconocido internacionalmente en temas financieros, con más de 830 millones de respuestas en Quora, un libro muy vendido en Amazon y colaborador de Forbes.