Many non-US residents consider US annuities as part of their retirement planning.

However, cross-border insurance regulations, IRS withholding rules, and tax treaty provisions make these products complex for foreign investors.

Este artículo trata:

- Can you buy an annuity in the US?

- What are the taxes on annuities in the US?

- How to buy an annuity in the US?

Principales conclusiones:

- Access is limited for non-US residents without a US address, TIN, or genuine US ties.

- Early-2026 Multi-Year Guaranteed Annuity rates are roughly 6–6.5%.

- NRA annuity income usually faces 30% US withholding unless reduced by treaty.

- An ITIN or SSN is required to claim treaty benefits or reduced withholding.

Mis datos de contacto son hello@adamfayed.com y WhatsApp +44-7393-450-837 si tiene alguna pregunta. También ofrecemos soluciones de estructuración a medida adaptadas a su situación.

La información contenida en este artículo es meramente orientativa, no constituye asesoramiento financiero, jurídico o fiscal y puede haber cambiado desde el momento de su redacción.

What is an annuity in the US?

In the US, an anualidad is a long-term insurance contract issued by a life insurance company that converts savings into future income payments.

Investors typically contribute a lump sum or a series of payments.

Then, the insurer guarantees either a fixed return or an income stream, depending on the product type.

Many annuities allow tax-deferred growth, meaning earnings are not taxed until withdrawals begin.

This feature makes annuities a common retirement planning tool for investors who want a predictable income later in life.

Annuities may be held inside retirement plans such as IRAs or 401(k)s (qualified annuities) or purchased with after-tax money as non-qualified annuities.

What are the types of annuities in the US?

In the US, the common types of annuities include fixed annuity, multi-year guaranteed annuity, variable annuity, fixed indexed annuity, immediate annuity, and deferred annuity.

- Fixed annuity: Pays a guaranteed interest rate for a set period, similar to a bank CD but issued by an insurer.

- Multi-Year Guaranteed Annuity (MYGA): A type of fixed annuity with a guaranteed rate for 3–10 years, often marketed as an alternative to CDs or bonds.

- Variable annuity: Lets you invest in sub-accounts similar to mutual funds, so value and income depend on market performance.

- Fixed indexed annuity: Credits interest based on an index (like the S&P 500) with caps and floors, offering downside protection but limited upside.

- Immediate vs deferred: Immediate annuities start paying income right away; deferred annuities grow first and pay later.

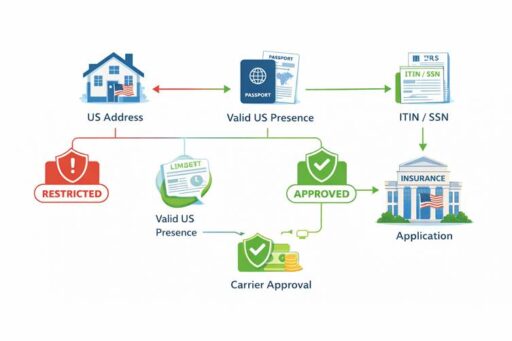

Can non-residents buy annuities in the US?

Non-US residents generally cannot easily buy US annuities unless they have a genuine US presence, such as legal residency, a US address, or an ongoing financial connection to the country.

Many US insurers only sell annuities to people who are physically and legally resident in the US, but rules vary by company and state.

Some carriers will allow a foreign national to own a US annuity if they have a valid US presence (like a US address, visa, or business connection), but others prohibit this entirely.

Cross-border sales are tightly controlled, and “fly in just to buy an annuity” is usually not allowed.

Can foreigners buy annuities in the US?

Foreign nationals who live in the US (for example, on a work visa) can often buy annuities if they meet the insurer’s underwriting and residency rules.

They typically need to buy in the state where they actually reside, and the application, issuance, and delivery should happen there.

Foreigners living abroad have far fewer options, and many insurers will decline the application if the buyer’s primary residence is outside the US.

Can a non-resident alien buy an annuity in the US?

Non-resident aliens (NRAs) may be able to buy a US annuity in limited cases, such as when they own property or a business in a US state and have a legitimate ongoing connection to that state.

However, many carriers’ compliance policies either restrict or ban sales to NRAs who are not US residents, because this can create regulatory issues and complex tax withholding obligations.

Availability is highly company-specific.

ITIN / SSN requirements:

A US TIN (SSN or ITIN) is usually required for reporting, withholding, and treaty claims. Without one, 30% default withholding generally applies.

US address rules:

Insurers usually require a permanent US mailing address in the state of sale and may ask for proof of residency (such as utility bills or lease agreements).

Carrier restrictions:

Each insurer sets its own cross-border policy, and many prohibit issuing contracts when the owner lives abroad or is in the state only to purchase.

Even when technically possible, applications from NRAs are heavily scrutinized and often declined.

How to buy an annuity in the US as a non-resident?

Non-residents need a genuine US connection, a TIN, and a carrier that permits foreign owners to buy a US annuity.

Step‑by‑step in simple terms:

1. Confirm eligibility. Check whether the insurer allows non-citizen or non-resident owners and in which states.

2. Get a US taxpayer identification number. Apply for an ITIN using Form W-7 if needed.

3. Establish a valid US address and connection. If you live in the US, use your actual residence in the state of sale.

4. Choose the annuity type and term. Decide between fixed, MYGA, indexed, or variable annuities based on risk tolerance and time horizon.

5. Complete application and tax forms. Submit the application and Form W-8BEN to confirm NRA status and treaty eligibility.

6. Fund the annuity. Fund with a wire or check in US dollars; for retirement rollovers, follow the carrier’s 401(k)/IRA rollover instructions.

7. Receive policy and confirm details. Review guarantees, surrender terms, payment destination, and withholding.

Annuity Payments: Currency and International Transfers

US annuity payments can usually be sent abroad, but many insurers require payments to be deposited into a US bank account first.

- Can annuity income be paid to a foreign bank account?

Some insurers can remit payments to foreign bank accounts, but others require payment to a US bank account in your name; rules vary by company and country risk.

- Receiving US annuity income outside the US

Many NRAs route annuity income to a US bank account and then transfer funds abroad, incurring FX and transfer fees; direct foreign payments may be slower or more restricted.

- Currency and exchange‑rate risk for overseas retirees

If you live outside the US, you are exposed to USD vs home‑currency movements: your real spending power can rise or fall with FX rates, which is a key risk when using US dollar annuities for local expenses.

What are the annuity rates in the US?

Many 5-year MYGA contracts currently offer around 6–6.5%, while some longer-term fixed annuities from highly rated insurers approach 7%.

However, this depends on market conditions and surrender terms.

Annuity rates largely move with long-term US interest rates, particularly Treasury yields and corporate bond markets.

This is because insurers invest premiums primarily in fixed-income securities to support their guarantees.

When long-term interest rates rise, insurers can generally offer higher annuity yields.

For context, the US Federal Reserve’s monetary tightening cycle in 2022–2024 pushed Treasury yields to their highest levels in more than a decade.

This allowed insurers to increase annuity crediting rates.

According to US government data, long-term Treasury yields and other interest benchmarks have remained elevated compared with the previous decade.

Thus, supporting higher fixed annuity rates.

Nevertheless, the exact rate available to a buyer depends on several factors:

- Guarantee period (for example: 3, 5, or 10 years)

- Insurer credit rating

- State regulations

- Surrender period length

- Distribution channel and commissions

Because rates change frequently, investors usually compare quotes from multiple insurers before purchasing.

What are the costs of annuities?

Annuities are priced through spreads, surrender charges, and optional rider fees.

Fixed and MYGA contracts usually have no visible annual charge, while variable annuities often exceed 2% per year.

- Variable annuity M&E: 0.9%–1.5%

- Fund expenses: 0.5%–1.5%

- Riders: 0.5%–1.2%

- Surrender charges: 5%–10% declining

What are the fees for annuities in the US?

Beyond ongoing charges, some annuities include sales commissions embedded into the pricing.

There may also be surrender penalties for early withdrawals and market value adjustments on some fixed annuities if you cash out before the end of the guarantee term.

For NRAs, add potential foreign bank transfer fees and currency conversion spreads when moving income abroad.

How much money do you need to buy an annuity in the US?

Minimum purchase amounts for annuities vary by product and insurer, but many fixed or MYGA annuities require at least 10,000–25,000 US dollars.

Some high-rate offers require 100,000 or more.

How are annuities taxed in the US?

For non-resident aliens (NRAs), US-source annuity payments not connected to a US business are taxed as FDAP income.

The default withholding is 30% on the taxable portion.

If the income is effectively connected (ECI), it is taxed at graduated rates on net income and requires filing a US tax return.

Qualified annuities (inside plans like 401(k)s and IRAs) are generally fully taxable when distributed, while non-qualified annuities are taxable only on the earnings portion.

How do tax treaties work for the US annuity withholding tax?

Many US tax treaties reduce or even eliminate US withholding on annuity and pension payments to residents of treaty partner countries, sometimes treating annuities similarly to pensions.

To claim treaty benefits, an NRA usually must provide a correct TIN and a completed form (e.g., W‑8BEN) to the payer, specifying the treaty article and rate.

The actual rate depends on the specific treaty, and not all countries have the same treatment.

Are annuity payments taxable in your home country?

In most cases, yes, your home country can tax annuity income according to its domestic rules, even if the US has already withheld tax.

Some countries tax only the growth portion, others treat annuities like pensions, and some give credits for US tax paid under a treaty.

You need local advice to understand how US annuity income fits into your home tax return.

What Are The Pros And Cons Of Annuities For Non-US Residents?

US annuities can offer attractive fixed returns and stable income, but access restrictions, tax rules, and currency risk can significantly affect outcomes for non-US residents.

Key advantages:

- Guaranteed income: Fixed annuities offer predictable interest and, if annuitized, stable lifetime income, reducing longevity risk.

- Attractive current rates: Early‑2026 MYGA rates around 6–6.3% and some longer-term fixed deals above 7% can be appealing in a diversified portfolio.

- US‑dollar exposure: For NRAs with USD liabilities or assets (like kids studying in the US or USD mortgages), US dollar income can be a good match.

- Professional regulation: US insurers and annuities are regulated at the state level and subject to solvency and consumer‑protection rules.

Key disadvantages:

- Access and compliance: Many carriers will not issue annuities to non-residents, or make the process difficult, especially for those living entirely abroad.

- Withholding tax and treaties: Default 30% US withholding on FDAP annuity income can significantly reduce net income if treaty relief does not apply or is not claimed properly.

- Currency and transfer risk: Income is in USD, and converting to local currency introduces FX volatility and banking fees.

- Estate tax exposure: Some US annuities can create US-situs exposure for NRAs, so estate-tax advice is essential

Who should consider an annuity?

US annuities may be suitable for non-resident aliens who have meaningful US ties, hold significant US‑dollar assets, and value guaranteed income more than liquidity.

They can also fit global expats planning partial retirement in the US or with beneficiaries in the US.

Others may find local or offshore retirement products more straightforward.

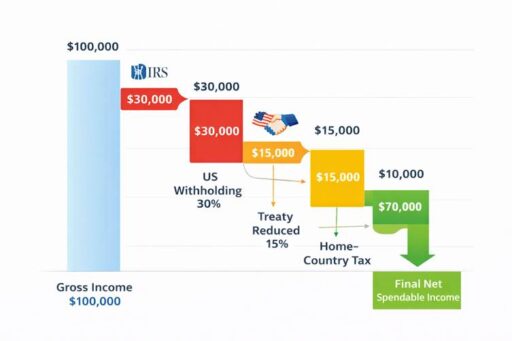

US Annuity Example For A Non-Resident Alien

Consider a non-resident alien who invests $500,000 in a fixed annuity paying about 6.5% interest.

This generates roughly $32,500 in annual income before taxes.

If the investor’s country has a tax treaty reducing US withholding from 30% to 15%, the US tax withheld would be about $4,875, leaving roughly $27,625 before home-country taxes.

The final income depends on local tax treatment and exchange-rate movements.

If the investor’s currency weakens against the US dollar, their local spending power may increase, while a stronger home currency could reduce the effective income.

What are the alternatives to annuities for non-US residents?

Alternatives to annuities include IRA drawdowns, lump-sum rollovers into global portfolios, international pension transfers, and offshore insurance wrappers.

These usually offer better currency alignment and simpler taxation but remove guaranteed lifetime income.

Keeping funds in an IRA with drawdowns

Keeping funds in an IRA allows flexible withdrawals but shifts market and longevity risk to the investor.

Lump-sum distribution

You may take a full lump‑sum payout from a US retirement plan, then invest in local or global portfolios.

This maximizes control and portability, but can trigger concentrated tax in the year of distribution and removes any built-in US tax deferral going forward.

International pension transfers

Some jurisdictions offer qualifying recognized overseas pension schemes (QROPS-style models outside the US context) or international pension plans that accept rollovers from various sources.

Transfers usually involve strict rules and advice requirements, and tax consequences differ by country.

Offshore retirement solutions

Bonos extraterritoriales, portfolio bonds, and international insurance wrappers let you invest globally with tax deferral in some jurisdictions.

These often offer more flexible currency options and estate‑planning tools, but fees can be high, and regulations vary widely.

Conclusión

US annuities can provide predictable income and relatively attractive fixed returns, particularly during periods when interest rates are elevated.

Even so, they are not always easy for non-US residents to access, as many insurers restrict sales to individuals who live or have a genuine financial presence in the United States.

For foreign investors who do qualify, the decision involves more than simply comparing interest rates.

Buyers must consider IRS withholding rules, tax treaty eligibility, and the potential for double taxation in their home country.

Currency fluctuations and international transfer costs can also affect the real value of annuity income received abroad.

Because of these complexities, non-resident aliens often evaluate US annuities alongside other retirement options such as global portfolios or offshore retirement structures.

Professional tax and asesoramiento financiero is usually essential before making a cross-border annuity decision.

Preguntas frecuentes

Who should not buy an annuity?

You probably should not buy a US annuity if you are a non-resident with no strong US ties, need high liquidity, or dislike complex tax reporting.

People with significant high‑interest debt, very small retirement balances, or short time horizons often find annuities inflexible.

How much does a 500,000 USD annuity pay per month?

It varies based on age, gender, rates, and whether payments last for life or a fixed term.

With today’s fixed rates around 6–6.5%, a simple rough estimate might be in the 2,000–3,000 USD per month range, but actual quotes vary by insurer and product design.

Are annuities FDIC insured?

No. Annuities are not FDIC‑insured; they are obligations of the issuing insurance company.

State guaranty associations provide limited protection, subject to state residency and coverage caps.

¿Le duele la indecisión financiera?

Adam es un autor reconocido internacionalmente en temas financieros, con más de 830 millones de respuestas en Quora, un libro muy vendido en Amazon y colaborador de Forbes.