Financial advice is professional guidance that helps individuals make informed decisions about saving, investing, tax strategy, retirement, and wealth protection.

It is one of the most-requested yet least-understood services in personal finance.

Done well, financial advice changes outcomes. Done poorly, it costs more than it saves.

Este artículo trata:

- What is financial advising in layman’s terms?

- What is the difference between financial planning and financial advice?

- What is the best financial advice?

- Who can offer financial advice?

Principales conclusiones

- Financial advice covers investing, tax planning, retirement, and wealth protection strategies.

- Good advice begins with your goals, not the advisor’s product menu.

- Experience and transparency matter more than titles alone.

- Digital and human advice models each serve different needs and cost levels.

Mis datos de contacto son hello@adamfayed.com y WhatsApp +44-7393-450-837 si tiene alguna pregunta.

La información contenida en este artículo es meramente orientativa. No constituye asesoramiento financiero, jurídico o fiscal, ni una recomendación o solicitud de inversión. Algunos hechos pueden haber cambiado desde el momento de su redacción.

What is financial advising in simple terms?

Financial advising is the process of a qualified professional assessing your financial situation and recommending a course of action aligned with your goals and risk tolerance.

It is not simply telling you where to invest.

It includes understanding where you are financially, where you want to go, and what obstacles sit between the two points.

At its core, financial advice is about making better money decisions with expert support rather than guessing on your own.

This applies whether you are:

- A first-time investor unsure how to allocate savings

- An expat managing money across two or more countries

- A high-net-worth individual trying to protect assets and reduce tax exposure

- Someone approaching retirement with no structured drawdown plan

The value of financial advice is not in the recommendations alone but in avoiding costly mistakes, reducing emotional decision-making, and building a strategy that fits your life.

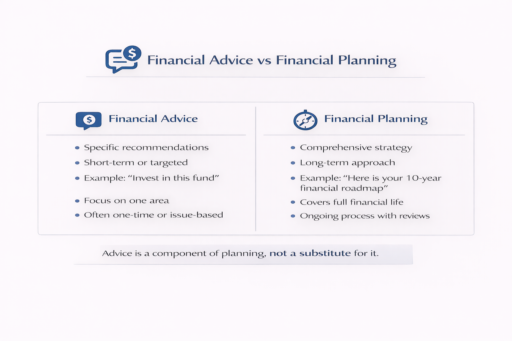

What is the difference between financial advice and financial planning?

Financial advice and planificación financiera are related but distinct.

Financial advice refers to specific, targeted recommendations, such as which investment to buy or how to structure a pension.

Financial planning is the broader, ongoing process of mapping your entire financial life.

Think of it this way: financial planning is the architecture of your financial future. Financial advice is what fills each room.

A financial planner takes a big-picture approach, helping you align budgeting, investing, retirement, estate planning, and tax into one cohesive strategy.

A asesor financiero may specialize in one element of that picture, such as portfolio management or insurance.

For most people, especially those with cross-border assets or complex income structures, both services are valuable.

What is good financial advice?

Good financial advice is advice that is relevant, practical, and genuinely aligned with your interests, not with the advisor’s commission structure.

It is not generic.

That said, several principles hold across most situations:

- Start with an emergency fund.

Before investing anything, hold three to six months of expenses in accessible cash. This protects your investments from being liquidated in a crisis.

- Invest early and consistently.

Starting earlier generally increases the long-term benefits of compounding.

- Diversify across asset classes and geographies.

Concentration in one country, one sector, or one currency is a risk that many investors underestimate. Global diversification reduces volatility.

- Minimize tax drag on investments.

In many jurisdictions, it is not what you earn but what you keep that determines long-term wealth. Tax-efficient structuring through the right wrappers, accounts, or jurisdictions makes a measurable difference.

- Avoid lifestyle inflation.

Increasing spending every time income rises is the most common reason people with high salaries fail to build wealth.

- Review your plan annually.

Life changes. Plans must too. What made sense at 30 may be entirely wrong at 45, especially if you have moved countries, changed employment status, or had dependants.

For expats, the quality of advice depends heavily on the advisor’s understanding of tax treaties, pension portability, and multi-jurisdictional investment access.

A locally focused advisor may give advice that is technically correct in one country but financially damaging in another.

Who provides financial advice professionally?

Financial advice may be provided by certified financial planners, investment advisors, wealth managers, and independent financial advisors.

Each of them has different scopes, qualifications, and compensation models.

Understanding who is advising you and how they are paid is essential before acting on any recommendation.

Certified Financial Planners (CFPs)

CFPs have completed rigorous training through the CFP Board of Standards and are held to high ethical standards, including a fiduciary duty to act in the client’s best interest.

They are registered professionals who advise on portfolio construction and asset management.

In the United States, they must be registered with the SEC or state regulators.

Wealth managers typically work with high-net-worth individuals and offer comprehensive services including estate planning, tax guidance, and investment management.

Independent Financial Advisors (IFAs)

IFAs are not tied to a specific institution or product provider, which can reduce conflicts of interest in their recommendations.

In international financial contexts, experience with cross-border clients often matters more than their domestic credentials.

An advisor is genuinely more valuable to you than one with impressive local qualifications but no international exposure, if they:

- Understand how your assets span multiple countries

- Understand how different pension systems interact

- Understand how residency status affects taxation

Regulation varies significantly by jurisdiction. The FCA governs UK advisors, ASIC oversees Australian advisors, MAS regulates Singapore-based professionals, and the SEC and FINRA cover US-registered advisors.

Regulatory registration is important for basic protection. However, regulation alone does not guarantee that an advisor understands your specific situation, particularly if you live abroad or hold assets across multiple countries.

Experience, fee transparency, and demonstrable client outcomes are often stronger indicators of quality.

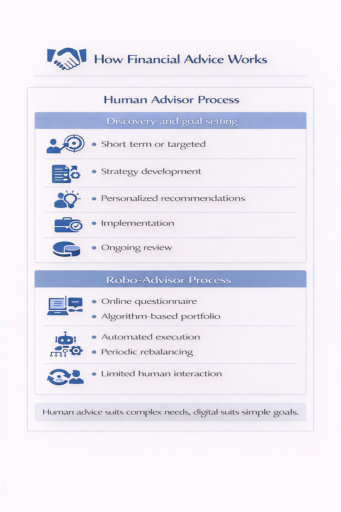

What is the financial advice process (digital vs human)?

En financial advice process typically begins with a discovery phase where an advisor assesses your financial position, goals, time horizon, and risk tolerance.

From there, a recommendation is developed, presented, and either implemented directly or executed by the client with guidance.

Ongoing advice includes regular reviews and adjustments as circumstances change.

Delivery models vary:

- Human advisors handle complex planning involving tax, estate, and cross-border considerations

- Digital platforms provide automated portfolio construction for simpler needs

- Hybrid models combine automation with access to human input for complex decisions

Human advisors provide depth. They can handle complex tax situations, cross-border asset structures, planificación patrimonial nuances, and emotional decision-making under market stress.

What is the cost of financial advice?

Financial advice typically costs anywhere from a few hundred dollars for one-off consultations to several thousand dollars per year for ongoing advisory services.

Common fee structures include:

AUM (Assets Under Management) Fee

The most widely used model for ongoing investment management. The average fixed percentage is approximately 1.05% of assets managed annually.

Robo-advisors typically charge 0.25% to 0.50% AUM.

Hourly Rate

For one-off or project-based advice. In the UK, hourly rates typically range from £150 to £300. In the US, the average hourly rate is approximately $268.

Flat Fee/Fixed Fee:

For a comprehensive financial plan delivered as a one-time engagement.

Average flat fees in the US are around $2,554. In the UK, a comprehensive plan often costs around £3,000.

Annual Retainer

For ongoing, broad-spectrum advice. These range from approximately $4,484 per year in the US to £2,500–£9,200 annually in the UK, depending on scope.

Subscription Model

A growing model where clients pay a monthly fee, averaging around $215/month in the US.

In international wealth management, pricing tends to reflect the complexity of services.

Cross-border tax planning, multi-jurisdictional portfolio management, and estate structuring across different legal systems command higher fees.

Whether higher fees are justified depends on the complexity of the advice provided.

Always ask for full fee disclosure before engaging any advisor. A transparent advisor will explain their fee, third-party charges, platform costs, and product commissions.

What is personalized financial advice?

Personalized financial advice is advice built entirely around an individual’s specific circumstances, not a templated solution applied to everyone with a similar age or income.

It accounts for:

- Your goals (retirement, education funding, property purchase, wealth transfer)

- Your tax residency and applicable tax laws

- Your risk tolerance and investment time horizon

- Your existing assets, liabilities, and income streams

For expats, personalization becomes more important due to global differences in taxation, residency, and investment access.

Standard domestic advice often does not translate cleanly across jurisdictions. What works in one country may be inefficient or unsuitable in another.

Effective international financial advice therefore requires an understanding of how multiple systems interact, including tax rules, investment structures, and legal frameworks.

Why Regulated Does Not Always Mean Compatibility

Regulation is a baseline, not a guarantee of suitability.

Credentials and registration matter, but experience, fee transparency, and familiarity with cross-border issues may be equally important.

The right questions to ask any advisor are:

- How many clients do you serve with similar international profiles?

- How are you compensated, and are there any conflicts of interest?

- Can you demonstrate outcomes for clients in similar situations?

- How do you handle cross-border tax and pension questions?

An advisor’s ability to answer these clearly is often more relevant than credentials alone in determining suitability.

Preguntas frecuentes

What is the standard 5 financial advice?

The standard five financial principles are to spend less than you earn. They also include building an emergency fund covering three to twelve months of expenses.

They involve avoiding or managing high-interest debt and investing consistently for long-term growth. They also include diversifying income and investments to reduce risk.

These principles form the foundation of long-term financial stability.

What kind of financial advisor do I need?

The right advisor depends on whether your needs involve gestión de inversiones, retirement planning, tax complexity, or cross-border issues.

What is a red flag for a financial advisor?

A red flag for a financial advisor includes guaranteeing returns, lacking transparency on fees, or pressuring you to invest quickly.

It also includes overly complex explanations that are hard to verify or missing regulatory credentials or licensing.

Is financial advice worth it?

For most people with meaningful assets or complex financial situations, professional advice generates a measurable net benefit.

The value comes not just from returns but from tax efficiency, behavioral coaching during market volatility, and avoiding costly structural mistakes.

The cost of not having a proper plan, particularly for expats or those with activos extraterritoriales, is often far greater than the cost of good advice.

How to be financially secure?

Financial security is achieved by maintaining diversified income, keeping expenses below income, and building emergency cash reserves.

It also requires long-term investing and protection against risks like war, job loss, health issues, and currency shifts.

¿Le duele la indecisión financiera?

Adam es un autor reconocido internacionalmente en temas financieros, con más de 830 millones de respuestas en Quora, un libro muy vendido en Amazon y colaborador de Forbes.