If you’re wondering how is inheritance tax calculated in Japan, it’s important to know that the country imposes one of the highest inheritance tax rates in the world, with rates reaching more than 50% for large estates.

The tax applies not only to Japanese citizens but also to some foreign heirs, depending on residency and asset location.

For foreign nationals and expats, navigating Japan’s complex inheritance tax rules is critical to avoid unexpected liabilities.

Si desea invertir como expatriado o particular con un elevado patrimonio neto, que es en lo que estoy especializado, puede enviarme un correo electrónico (hello@adamfayed.com) o WhatsApp (+44-7393-450-837).

Esto incluye si busca una cartera de expatriados gratuita revise para optimizar sus inversiones e identificar perspectivas de crecimiento.

Algunos hechos podrían cambiar desde el momento de la redacción. Nada de lo aquí escrito constituye asesoramiento financiero, jurídico, fiscal o de ningún tipo, ni una invitación a invertir.

In this article, we’ll explore how to calculate Japan inheritance tax, covering tax rates, exemptions, and key rules every heir and property owner should know.

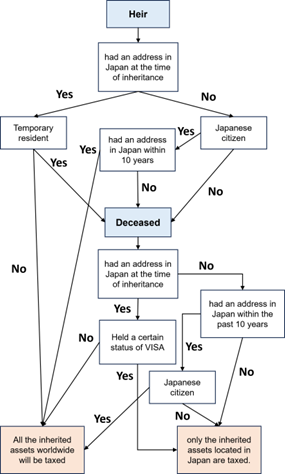

What Is the Inheritance Rule in Japan?

Japan’s inheritance tax applies to assets passed from the deceased (decedent) to their heirs, with taxation based on both residency and asset location.

If either the decedent or the heir is a Japanese resident at the time of death, inheritance tax is levied on worldwide assets.

If both are non-residents, only assets located in Japan are taxable.

The tax is calculated individually for each heir, based on their share of the inheritance and their relationship to the decedent.

Closer relatives like spouses and children generally benefit from higher exenciones and lower tax rates compared to distant relatives or unrelated heirs.

In short, the inheritance rule in Japan imposes tax obligations not only on assets within Japan but also on global assets when residency conditions apply, making tax planning essential for families with diverse holdings.

For a deeper understanding of the inheritance rule in Japan, it is also important to be familiarized with the Japanese line of succession under the Japanese Civil code which governs it.

Japan Inheritance Tax Rate: How Much Will You Pay?

Japan’s inheritance tax is known for its high progressive rates, reaching up to 55% for large estates.

The tax is calculated based on the share each heir receives, with rates increasing as the inherited amount grows.

Current Tax Brackets (as of 2025):

- Up to ¥10 million: 10%

- ¥10 million – ¥30 million: 15%

- ¥30 million – ¥50 million: 20%

- ¥50 million – ¥100 million: 30%

- ¥100 million – ¥200 million: 40%

- ¥200 million – ¥300 million: 45%

- ¥300 million – ¥600 million: 50%

- Over ¥600 million: 55%

The high rates are due to Japan’s policy of wealth redistribution and efforts to discourage the concentration of wealth across generations.

Combined with relatively low exemption thresholds, many heirs end up facing significant tax liabilities even on modest inheritances.

This is why Japan inheritance tax is so big—the combination of steep progressive rates, limited exemptions, and taxation of worldwide assets for residents results in heavier tax burdens compared to many other countries.

Careful planning is essential to reduce tax exposure.

Japan Inheritance Tax Exemption: What Allowances Apply?

Japan offers a basic inheritance tax exemption that reduces the taxable estate before tax is calculated.

The exemption is: ¥30 million plus ¥6 million per statutory heir.

For example, if there are three heirs, the total exemption is ¥30 million + (¥6 million × 3) = ¥48 million.

Special Exemptions:

- Spousal deduction: A surviving spouse can inherit up to ¥160 million tax-free or the legally entitled share, whichever is greater.

- Minor and disabled heirs: Additional deductions apply for underage children and heirs with disabilities, based on age and disability level.

These exemptions can significantly lower the taxable amount, but with high property values in Japan, many estates still exceed these thresholds.

Japan Inheritance Tax on Property: Special Considerations

In Japan, inmobiliario is assessed at its official government valuation rather than market price for inheritance tax purposes.

This valuation is often lower than the actual market value but can still result in significant tax liabilities, especially in high-demand areas.

Key points to consider:

Fixed Asset Tax Evaluation: The property’s taxable value is determined by government appraisals, updated periodically.

Land vs. Building Valuation: Land and structures are assessed separately, and special reductions (like small residential land deductions) may apply for family homes.

Liquidity Challenge: Property is taxed based on value, not cash flow, meaning heirs may face large tax bills without liquid assets to cover them.

If the inherited property is sold, impuesto sobre plusvalías may also apply on any appreciation since the decedent’s acquisition.

What Is Foreign Inheritance Tax in Japan?

In Japan, inheritance tax applies to both residents and non-residents, with the scope of taxation determined by the estatuto de residencia of the decedent and the heir.

Residents: If either the decedent or the heir is a Japanese resident at the time of inheritance, the tax applies to worldwide assets.

Non-Residents: When both the decedent and the heir are non-residents, only assets located within Japan are subject to inheritance tax.

It’s important to note that the definition of “resident” for inheritance tax purposes may differ from that used for income tax.

For instance, temporary residents—those who have lived in Japan for less than 10 years within the last 15 years—may be taxed only on assets located in Japan.

Japan Inheritance Tax Calculator

Estimating your potential inheritance tax in Japan is crucial for planificación financiera, especially given the country’s high tax rates.

Step-by-Step Manual Calculation:

- Determine the gross estate value: Add up the market value of all inherited assets, including property, cash, investments, and valuables.

- Subtract debts and funeral expenses: Legitimate debts and final expenses reduce the taxable estate.

- Apply exemptions: Deduct the basic exemption (¥30 million + ¥6 million × number of statutory heirs) and any special exemptions like spousal or dependent deductions.

- Divide the taxable estate: Split the taxable estate according to legal heir shares to calculate each heir’s portion.

- Apply tax rates: Use Japan’s progressive inheritance tax rates (ranging from 10% to 55%) to determine the tax per heir.

Example: How Inheritance Tax is Calculated in Japan

Heirs: Spouse, Child 1, Child 2

1. Gross estate value:

- Total assets = ¥350 million

2. Debts and funeral expenses:

- Debts + funeral expenses = ¥20 million

- Net estate = ¥350 million – ¥20 million = ¥330 million

3. Apply exemption:

The basic exemption is:

- ¥30 million + (¥6 million × number of heirs)

- Since 3 heirs: ¥30 million + ¥6 million × 3 = ¥48 million

Taxable estate = ¥330 million – ¥48 million = ¥282 million (Aggregate Tax Base)

4. Determine legal share:

| Herencia | Individual Taxable Base | ||

| Successor | Statutory Share | Aggregate Tax Base | |

| Cónyuge | 1/2 | 282,000,000 | 141,000,000 |

| Child 1 | 1/4 | 282,000,000 | 70,500,000 |

| Child 2 | 1/4 | 282,000,000 | 70,500,000 |

5. Apply tax rates:

| Tax base | Tax rate (Multiply) | Marginal Deduction (Subtract) | |

| up to | 10,000,000 | 10% | – |

| up to | 30,000,000 | 15% | 500,000 |

| up to | 50,000,000 | 20% | 2,000,000 |

| up to | 100,000,000 | 30% | 7,000,000 |

| up to | 200,000,000 | 40% | 17,000,000 |

| up to | 300,000,000 | 45% | 27,000,000 |

| up to | 600,000,000 | 50% | 42,000,000 |

| above | 600,000,000 | 55% | 72,000,000 |

Applying the marginal tax rate, it would be:

| Heir | Individual Tax Base | Gross Tax Liability |

| Cónyuge | 141,000,000 x 40% – 17,000,000 | 39,400,000 |

| Child 1 | 70,500,000 x 30% – 7,000,000 | 14,150,000 |

| Child 2 | 70,500,000 x 30% – 7,000,000 | 14,150,000 |

Now, apply the spousal tax credit: ¥160 million.

This tax credit offsets up to ¥160 million of inheritance tax for the spouse.

Since the spouse’s gross tax liability is ¥39,400,000, the entire tax is wiped out by the credit:

| Heir | Gross Tax Liability | Spousal Tax Credit | Final Tax Payable |

| Cónyuge | ¥39,400,000 | ¥160,000,000 | ¥0 |

| Child 1 | ¥14,150,000 | ¥0 | ¥14,150,000 |

| Child 2 | ¥14,150,000 | ¥0 | ¥14,150,000 |

Japan Inheritance Tax Calculator Tools for Foreigners

Several online tools can simplify this process by automatically factoring exemptions and rates.

While most are in Japanese, international tax advisory firms or bilingual legal websites often offer English-language calculators tailored for foreign heirs.

These tools provide estimates but should not replace advice from a qualified tax professional.

Planning Strategies to Reduce Japan Inheritance Tax

Reducing Japan inheritance tax liability requires early and strategic planning, especially for high-net-worth individuals and international families.

Here are key strategies:

- Lifetime gifting:

- Gradually transfer assets to heirs during your lifetime to reduce the taxable estate.

- Be mindful of gift tax thresholds to avoid unintended tax burdens.

- Trusts and estate planning structures:

- Cierto fideicomisos can help manage assets across generations, though Japan’s trust taxation is complex.

- Professional advice is essential to ensure compliance and effectiveness.

- Cross-border tax planning:

- Review tax treaties between Japan and other countries to minimize double taxation.

- Structure foreign assets in a way that aligns with both Japanese and international tax rules.

- Understand reporting requirements for overseas assets to avoid penalties.

Principales conclusiones

- Japan’s inheritance tax system is highly progressive, with rates up to 55%.

- Both residents and certain non-residents may be taxed on worldwide assets.

- Exemptions and deductions are available but require proper documentation and planning.

Given the complexity, engaging a qualified tax advisor or legal professional specializing in Japan inheritance tax is critical.

With professional guidance, you can manage your tax exposure, protect family wealth, and ensure a smoother transfer of assets.

¿Le duele la indecisión financiera?

Adam es un autor reconocido internacionalmente en temas financieros, con más de 830 millones de respuestas en Quora, un libro muy vendido en Amazon y colaborador de Forbes.