Existen muchas opciones en el mundo de la inversión. En este artículo hablaremos de 10 de ellas.

Si quieres invertir y estás confuso con todas las opciones que hay, puedes ponerte en contacto conmigo utilizando este formulario, o utilice la función de chat que aparece a continuación.

1 ¡Invierte en ti mismo!

Invertir en uno mismo da sus frutos, si se hace de la manera correcta.

La educación formal y la autoeducación pueden ofrecer un gran retorno de la inversión, si estás centrado.

En la web hay casi todas las herramientas que necesitas para hacerte más fuerte con un poco de esfuerzo.

Aprende un idioma, certifícate, conviértete en traductor y duplica tu dinero como autónomo, o estudia un lenguaje de programación de gran importancia que sepas que la mayoría de las empresas necesitarían, luego coge un libro sobre inversiones, lee este artículo o busca un consultor que pueda enseñarte lo básico en poco tiempo.

Cuando no hay dinero para invertir, tus ideas son dinero, y tu tiempo para hacerlas realidad también es una inversión. Ten en cuenta que el inversor medio sólo gana 2,5% anuales con su capital.

Por lo tanto sólo con ser más productivo o frugal, puedes conseguir hacer 100% a infinito más ingresos que antes. Siendo más productivo, siendo más eficiente en lo que sabes hacer, el dinero vendrá a ti, no necesitarás perseguirlo.

Y no importa si lo aprendes en una escuela, en un centro de aprendizaje o por ti mismo, si realmente te comprometes a entender cómo funciona algo y consigues hacerlo funcionar, seguro que funcionará.

No hay otra opción, ¿has oído hablar de todos los hombres de negocios que leen varios libros a la semana?

Leer diferentes libros puede darte diferentes impresiones y hacer que absorbas algunas ideas y conceptos importantes a través de sus páginas, pero si aprendes lo suficiente de un solo libro y lo aplicas, ¡lo has conseguido!

2 Invierta en su empresa

Muchos ricos mantienen su patrimonio invertido en sus empresas o en otras más rentables, como inversiones privadas o empresas que cotizan en bolsa.

Por supuesto, la mayoría de la gente fracasa a la hora de crear su propia empresa. Un método de probada eficacia es conseguir primero un trabajo, ser bueno en algo y luego montar un negocio en ese nicho.

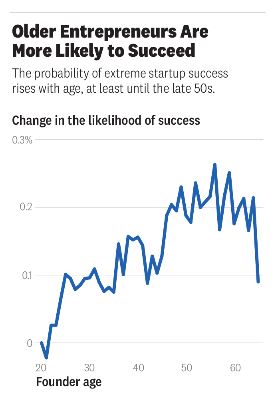

Las estadísticas muestran que las personas con experiencia tienen más probabilidades de éxito a la hora de crear su propia empresa, aunque la situación empieza a igualarse por encima de los 55 o 60 años:

Esto no significa que haya que esperar a tener 60 años para crear una empresa, sino simplemente que es más probable tener éxito después de los 20 y los 30 años.

3 La Bolsa

Ya hemos hablado de invertir en nuestras propias empresas. Siendo racionales, seguramente querríamos invertir en la flor y nata, en esas pocas empresas que consiguen salir a bolsa.

Existen numerosas formas de acceder al mercado bursátil. Por ejemplo, invirtiendo en acciones individuales, lo cual es más arriesgado que invertir en todo el mercado o en índices como el S&P500 o el Dow Jones.

Hay otras formas de invertir en acciones:

Acciones: Puede comprar las acciones de las empresas que crea que crecerán más en el futuro, aprovechando el crecimiento compuesto que, como una bola de nieve, no deja de hacerse más y más grande. Sin embargo, los selectores de acciones no suelen batir al mercado a largo plazo.

ETFs: ¿Quiere comprar a la vez acciones de varias empresas pertenecientes al mismo sector? Los ETF pueden ser para usted. Existen ETF vinculados a índices, que son similares a los fondos indexados en la práctica, y ETF específicos de un sector, como el tecnológico, por ejemplo.

Hay cientos de opciones para elegir en función de sus necesidades.

4 Depósito bancario en efectivo

Un depósito bancario en efectivo es una de las inversiones más sencillas que se puedan imaginar.

El problema es que hoy en día te enfrentas a los siguientes riesgos:

- Riesgo de inflación. ¿Los tipos de interés ofrecidos son inferiores a la inflación? En cuyo caso tiene garantizado perder dinero

- Riesgo de divisas. ¿Vive en un mercado emergente? Podrías perder mucho en relación con el dólar, la libra y el euro. En los últimos 10 años, muchos inversores sudafricanos y de otros países han perdido mucho efectivo en divisas fuertes, a pesar de los altos tipos de interés

- Riesgo relativo. El efectivo nunca ha batido a las acciones ni a los bonos a largo plazo.

- Riesgo de ruina. En situaciones muy graves, como en algunos países de América Latina y Zimbabue en los últimos tiempos, puedes perder casi todo tu dinero por la hiperinflación.

5 Comprar tierras o propiedades

Hay muchas formas de comprar una propiedad. Por ejemplo:

- Su propia casa

- Alquileres

- REITS y pagarés de préstamo

- Formas alternativas de poseer una propiedad, de las que hablaremos más adelante

En general, el rendimiento de la propiedad es más importante que las perspectivas de crecimiento del capital para los inversores inmobiliarios.

Depender de que un bien se deprecie, es decir, de que una persona gaste más dinero que usted por el mismo bien, es una forma de especulación.

En comparación, una de las “reglas de inversión de Warren Buffett” es que siempre hay que centrarse en lo que un activo puede reportarle.

Si no te gusta este enfoque ‘’pasivo’’, puedes optar por uno activo, por:

- Huertos.

- Tierras de cultivo de hortalizas.

- Tierras de cultivo en hileras.

- Terreno ganadero.

- Timberland.

- Suelo urbanizable residencial

- Suelo urbanizable comercial

- Tierras de producción minera

- Viñedos

- Terrenos de recreo.

La mayoría de las veces, sin embargo, los terrenos no pueden ser a la vez agrícolas y residenciales o comerciales. De hecho, debido a diversas causas geológicas, construir casas sobre un sólido inadecuado podría provocar el derrumbe del mismo y su hundimiento, como está ocurriendo con la actual Yakarta, en Indonesia, ya que el suelo no puede soportar todo el peso que tiene encima.

Un inconveniente a tener en cuenta es que si desea comprar tierras, como ciudadano en su país, o invirtiendo en otros países, podría enfrentarse a numerosos y complicados problemas fiscales derivados de ser el propietario de la misma.

En cualquier caso, es un gran error sugerir que “el alquiler es dinero muerto”.

Alquilar frente a comprar (por lo que su residencia principal) es un juego de pelota totalmente diferente a considerar las propiedades de alquiler.

Incluso conozco a algunos inversores inmobiliarios profesionales que alquilan su propia casa, pero poseen varias propiedades en alquiler, por este motivo.

5 Materias primas y recogida

Mucha gente asume que las materias primas son buenas inversiones. ¡El petróleo se acaba! ¡El agua se acaba! ¡Los minerales son limitados! Las hemos oído todas.

Sin embargo, a largo plazo, las materias primas han sido muy malas inversiones. oro.

Las materias primas tienen su tiempo al sol. El oro y la plata registraron buenos resultados entre 2000 y 2011. Los diamantes, el petróleo y el cobre también lo han hecho bien durante numerosos periodos en el pasado.

No cabe duda de que tendrán otros buenos periodos en el futuro. Sin embargo, el problema fundamental de las materias primas es el mismo que el de su residencia principal:

- No producen un cupón o rendimiento a menos que compre acciones de empresas productoras de petróleo como BP o Shell.

- No pagan dividendos a menos que sean una acción

Una vez más, volvemos a la situación en la que esperamos que la persona que venga detrás de nosotros pague más por el mismo bien.

6 Invertir en REIT

Ya hemos hablado de los bienes inmuebles, pero habría que dedicar toda una sección a los fondos de inversión inmobiliaria (REITS).

Un REIT es una empresa que se centra en la compra de bienes inmuebles que producen ingresos.

Los activos típicos incluyen edificios de apartamentos, oficinas, centros comerciales, viviendas para estudiantes, almacenes y otras propiedades que podrían alquilarse a inquilinos. No suelen poseer muchos terrenos en bruto, por ejemplo.

Algunos de los inmuebles más grandes y aclamados del mundo han sido, o son actualmente, propiedad de REITs, por ejemplo, el Empire State Building.

Los REIT distribuyen la mayor parte de sus ingresos netos a los inversores. En Canadá se hace mensualmente, es trimestral en EE.UU., eso los convierte en activos productores populares.

Muchos REIT son fácilmente accesibles y pueden adquirirse a través de una cuenta de corretaje en línea. De este modo, los inversores pueden exponerse al mercado inmobiliario por apenas un par de cientos de dólares.

Existen riesgos. El riesgo más conocido es que son susceptibles a las subidas de los tipos de interés.

Como son propietarios, tienen enormes deudas en forma de hipotecas y líneas de crédito, etc. Si los tipos de interés suben rápidamente, podría causarles problemas. Un REIT bien gestionado se esforzará por mitigar ese riesgo en consecuencia.

Un peligro menos conocido es que los grandes REIT suelen pagar de más por los inmuebles.

Necesitan desplegar enormes sumas de efectivo rápidamente para generar un rendimiento para los inversores. Por ejemplo, un REIT puede tener $100.000.000 en el banco que necesita invertir en algún sitio. No hay muchas propiedades que se vendan por $100.000.000, así que sus opciones son limitadas.

Podría buscar 2 propiedades por $50.000.000 cada una para abrir opciones, pero aun así, no hay demasiado con lo que trabajar. Los grandes REIT tienen mucho dinero y no mucho tiempo para invertirlo, por lo que a veces se ven obligados a hacer compras relativamente ineficaces. Por ello, pueden sufrir fuertes caídas de precios si los mercados inmobiliarios se desploman.

Algunas personas prefieren los REIT pequeños por esa razón, pero aun así, los REIT son generalmente apreciados por los inversores orientados a los ingresos.

También pueden ser una buena forma de participar en el sector inmobiliario sin tener que comprar una propiedad. Y, como en cualquier inversión, la clave está en investigar antes de comprar.

Los REITS de buena calidad pueden ser inversiones excelentes que añaden diversificación a una cartera.

7 Notas estructuradas

Notas estructuradas pueden ser formas de inversión arriesgadas, como ya he mencionado antes.

Si se utilizan correctamente, los pagarés estructurados ofrecen a los inversores una amplia gama de oportunidades a pesar de los riesgos.

Los pagarés estructurados son obligaciones de deuda emitidas por entidades financieras, que también contienen un componente derivado incorporado que ajusta el perfil de riesgo-rentabilidad del valor. Con los pagarés estructurados, puede invertir en varias clases de activos, regiones o sectores que pueden no ser fácilmente accesibles para los inversores privados.

Su rendimiento depende de varios activos subyacentes, como un índice de renta variable, una cesta de acciones individuales o un índice de crédito. Si el activo subyacente se comporta como se espera, la rentabilidad será positiva. Por lo tanto, la rentabilidad de una nota estructurada seguirá tanto a la obligación de deuda subyacente como al derivado implícito en ella.

Un ejemplo de pagaré estructurado sería un bono a tres años combinado con un contrato de futuros sobre cacahuetes. Los pagarés estructurados más comunes incluyen pagarés protegidos por el principal, pagarés convertibles inversos y pagarés apalancados. Con mayor frecuencia, una nota estructurada ofrecerá pérdidas limitadas a cambio de ganancias limitadas en comparación con otros activos.

Un gran inconveniente es que los derivados siempre son complicados, aún más, cuando se combinan con otros productos financieros.

Esto hace que una nota estructurada sea un producto muy complejo, ya que el inversor tiene que entender perfectamente el producto que está comprando, y ya que funciona a la vez como un instrumento de deuda y como un derivado.

Por lo tanto, sólo deben ser utilizados por inversores profesionales, y como un pequeño porcentaje de una cartera.

8 Financiación colectiva

Crowdfunding es cuando individuos o startups utilizan una plataforma online para conseguir financiación para un proyecto a nivel global.

Aprovecha la facilidad de acceso a vastas redes de personas a través de los medios sociales para reunir a inversores y empresarios, con el potencial de aumentar el espíritu empresarial ampliando el grupo de inversores más allá del círculo tradicional de propietarios, familiares y capitalistas de riesgo.

El crowdfunding mundial recaudó 16$ mil millones de dólares de 2000 a 2005 y se prevé que alcance los 100$ mil millones en 2025.

Existen 4 tipos de crowdfunding, deuda, capital, recompensas y donación.

- Basado en deuda: Es cuando los contribuyentes reciben un tipo de interés a cambio de su contribución, ejemplos incluyen plataformas como FundedHere, CROWDO y MoolahSense.

- Basadas en acciones: Los contribuyentes reciben acciones a cambio de sus aportaciones. Algunos ejemplos son AngelList, FUNDNEL, SEEDRS y CAPBRIDGE.

- Basadas en recompensas: Cuando a los contribuyentes se les prometen recompensas a cambio de su contribución, como el acceso prioritario a un producto una vez que esté en el mercado, ejemplos incluyen KICKSTARTER, Indiegogo y Ulule.

- Basadas en donaciones: Cuando las donaciones son benéficas y generalmente deducibles de impuestos, los ejemplos incluyen, Indiegogo, Patreon, YOUCARING y FriendFund.

Antes de invertir en una plataforma de crowdfunding es mejor tener en cuenta su antigüedad. De hecho, la mayoría de ellas son nuevas en el mercado y las plataformas de crowdfunding necesitan mucho dinero por adelantado en sus primeros años de actividad.

Un caso curioso de crowdfunding fue el de un individuo que quería crear una nueva receta de ensalada de patata. Su objetivo era recaudar $10, pero consiguió más de $55.000 de 7.000 avalistas. Los inversores pueden elegir entre cientos de proyectos e invertir tan sólo $10.

De nuevo, el crowdfunding es una inversión muy arriesgada en comparación con algunas de las alternativas.

9 Compartir coche

El medio ambiente y las “cuestiones verdes” son cada vez más importantes para los jóvenes.

La atención a nuestro entorno hizo que surgieran nuevas líneas de tendencia y oportunidades económicas y que otras se hundieran.

Ahora puedes generar ingresos con un coche extra alquilándolo a diario. Si lo guardas en un garaje, su valor se depreciará hasta 60% en 5 años desde el momento de la compra.

Entonces, ¿por qué no mantenerlo activo todo el tiempo cuando no lo necesitas? No todo el mundo tiene coche, como en Estados Unidos.

Por lo tanto, si vives en una ciudad poblada, principalmente en los países occidentales, podrías ofrecer tu coche por un precio razonable en el mercado y mantenerlo activo y crear un buen flujo de ingresos. Seguramente tendrás algunos costes detrás, como el seguro, arreglarlo y quizás gente borracha-irresponsable.

Compartir coche no es una inversión probada a largo plazo para la inmensa mayoría de la gente.

10 Productos de consumo descatalogados.

Si compra bienes de consumo al por mayor cuando hay rebajas o descuentos, puede ahorrar 6%-10%.

También ocurre que una gran marca mundial se declara en quiebra, podría ser un gran negocio coger todo lo que se pueda, esperar unos años y venderlos a un precio más alto a los nostálgicos.

Esto ocurre cada vez que se lanza un nuevo producto en cantidad limitada.

Los grandes inversores o también los particulares que tengan algo de dinero ahorrado, empezarán a comprar cientos de camisetas Supreme o iPhones para venderlos entre 3 y 4 veces más que su precio inicial, ya sea físicamente o en eBay/Amazon.

Esto ocurrió hace poco con el brote de COVID, cuando algunos individuos almacenaron máscaras planas y máscaras 3D y las vendieron a un precio entre 10 y 20 veces superior al original, enriqueciéndose con el sufrimiento y el pánico de otras personas.

No es raro ver que, todavía hoy, hay coleccionistas que pagarían millones sólo por tener el objeto que necesitan en su colección para sentirse satisfechos, ya sea un cuadro, una botella o un sello de correos.

Sin embargo, en general, este tipo de cosas son más un pasatiempo y para ahorrar dinero que una inversión.

Conclusión

En general, los fondos indexados y de renta fija y otros tipos de inversión a largo plazo, ofrecen la mejor oportunidad de inversión ajustada al riesgo, suponiendo que se pueda ser a largo plazo.

Otros tipos de inversiones pueden aportarle diversificación. Si se utilizan con moderación, pueden ser buenas inversiones alternativas.

Un error clave que hay que evitar es esperar que la persona que venga detrás de usted pague más por el mismo bien que usted pagó por él.

Esa es la razón principal por la que el oro, la mayoría de las materias primas y varios activos simplemente han mantenido su valor después de la inflación durante 2.000 años aproximadamente: no ofrecen un cupón, rendimiento o dividendo.

Por tanto, lo único que mantiene el precio es la esperanza de que la persona que venga detrás pague más por él.

¿Le duele la indecisión financiera?

Adam es un autor reconocido internacionalmente en temas financieros, con más de 830 millones de respuestas en Quora, un libro muy vendido en Amazon y colaborador de Forbes.

Me gusta lo de “invierte en ti mismo’ si no tienes suficiente capital para poner en marcha un negocio.

gracias me alegro que te guste

requiere mucho trabajo