Evelyn Partners is a financial services and professional services company based in the United Kingdom. It was previously recognized as Tilney Smith & Williamson.

Its establishment stemmed from a merger in 2020 between Tilney and Smith & Williamson. The company also manages the online investment platform known as Bestinvest.

Sometimes Tilney will be used interchangeably with Evelyn Partners.

The article will talk about the positives, negatives, and suggest what you can do if you aren’t satisfied with the investment.

It will mainly focus on Evelyn Partners products sold to expats, but it will briefly mention about the options for UK clients, and how the two can differ dramatically.

My overall position is that much better options exist for expats and investors in general.

Si desea invertir como expatriado o particular con un elevado patrimonio neto, puede enviarme un correo electrónico (advice@adamfayed.com) o utilizar estas opciones de contacto.

Whilst this article has been updated over time, some information might be outdated.

Who is Evelyn Partners/ Tilney BestInvest?

Tilney BestInvest Ltd, or Tilney Group, is a planificación financiera and investment company. Their assets under management exceed 20 billion.

They became famous for their `spot the dog` commentary, where they critique bad funds that under-perform.

They have an office in London, but also have worldwide clients, due to their distribution networks across the Middle and Far East.

Where is Tilney BestInvest sold?

They have offices in London, Glasgow, Liverpool and Edinburgh. They are sold worldwide in Hong Kong, Malaysia (Kuala Lumpur), Qatar, Cambodia (Phnom Penh), Thailand (Bangkok, Pattaya and Phuket especially) and Mainland China (Shanghai mainly) due to broker relationships they have, including with Infinity Financial Solutions.

In the overseas market, Tilney is usually sold via third party platforms, and is typically much more expensive than buying from the UK.

So this revise article should be more considered a review of Tilney BestInvest for expats in the Middle East, South East Asia and beyond, rather than a UK review, even though a percentage of what I will say will be relevant to UK investors as well.

What services do Evelyn Partners offer in the UK?

It isn’t within this articles scope to mention their UK-specific services, as it focuses on expats.

However, they do offer some UK-specific services directly – in other words through Tilney and not third party platforms or brokers.

Those services include the BestInvest Junior ISA, Bestinvest SIPP and BestInvest Investment Account.

The Junior ISAs allow parents to save and invest for their children’s future, in a tax-efficient manner.

In general, the reviews on these are more positive than their overseas expat offerings, but better solutions still exist nevertheless.

What is BestInvest’s performance relative to the stock markets?

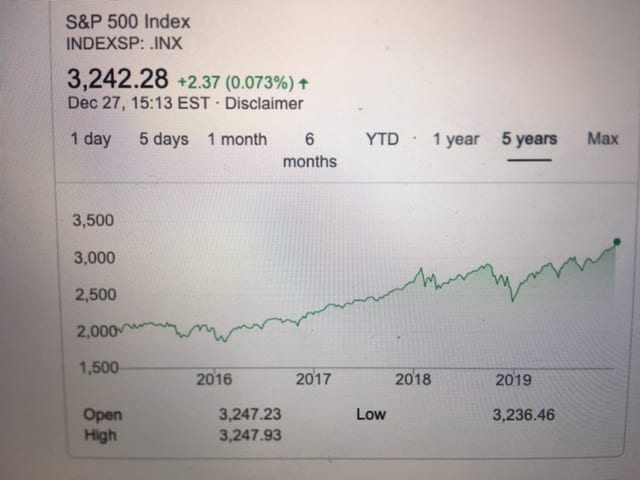

The US S&P has increased by 11.48% so far this year – as of March 6, 2019. 2018 was -4.38%. 2017, 2016 and 2015 was 21.83%, 11.96% ands 1.38% respectively. The accumulative performance has been over 42%.

If you would have invested $100,000 in the US S&P in 2015, therefore, you would have more than $142,000 today. Even if you added 10% government bonds, and 90% S&P as per Warren Buffett’s suggestion,you would now have well over $130,000.

If you had invested in the BestInvest aggressive portfolio, in comparison, from 2015 until now, you would have about $129,000 before the aforementioned fees.

The BestInvest Defensive Portfolio has only produced about 2% per year before fees, meaning several offshore investors are seeing negative returns, despite markets being up.

It is a numbers game – compounded fees harm compounded gains. 2% per year easily gets wiped out by the aforementioned high fees. Even 7%-8% per year gets reduced to 3%-4% if the compounded, indirect, fees are high.

So, does that mean that BestInvest never performs well?

BestInvest funds have of course performed well during some period, especially if markets are performing very well.

However, that doesn’t mean they have performed well compared to the overall market.

Take some recent years as an example. On the surface some of the funds haven’t done badly.

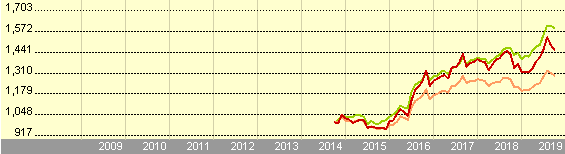

The red line shows that one of Tilney BestInvest’s Euro growth funds has performed quite well, with the red line illustrating this points

It has certainly performed better than most of Tilney’s other funds. However, look at how the S&P 500 has performed during a similar period, which has gone up by more than 62% excluding dividends.

And that is excluding the fact that the huge fees would have eaten into the BestInvest performance.

In reality, those 50% returns with the BestInvest Portfolio, might well have ended up being closer to 20% over a 5 year period for this very reason.

These huge fees, in turn, will compound over a long period of time. That means that over a 20-30 year period, they will really eat into your returns.

How about during periods like in 2022 with falling markets?

Nobody knows how well Tilney’s portfolios will perform during periods of falling markets.

It appeared to be a good time to invest in markets, but there was no indication that BestInvest’s portfolios will do better during such periods. They didn’t in 2008-2009. What is certain is it isn’t a good idea to “wait and see” if you aren’t happy with your existing portfolio.

Evelyn Partners/ Tilney BestInvest Funds

What funds are most widely sold?

Some of the main funds sold are:

- IFSL Tilney Bestinvest Aggressive Growth Portfolio

- IFSL Tilney Bestinvest Growth Portfolio

- IFSL Tilney Bestinvest Income Portfolio

- IFSL Tilney Defensive

- IFSL Bestinvest Income Portfolio R GBP

Each funds will come with a certain class, and associated charge. As an example, IFSL Tilney Bestinvest aggressive growth portfolio clean acc is slightly different to the “unclean” version.

In human terms, the clean version pays less in terms of fees to the advisors.

Who usually buys the funds outside of the UK?

It varies but typically British expats, alongside Japanese, South Africa, Korean, Norwegian, Swedish and other expat groups.

Many of these expats are looking for something specific, like expat advice for British expats in Cambodia or expat advice for Japanese people in Malaysia or Thailand.

Some are looking for something more vague, like financial advice in Hong Kong or another location.

Which offshore products are BestInvest sold through?

The main providers are the same ones that are reviewed in the article referred to at the start of this piece.

These providers are usually in Isle of Man, Guernsey, Bermuda, British Virgin Islands, Cayman Islands and Jersey.

It makes sense, in many ways, for expats to invest overseas and offshore, when they live outside their home country.

So the issue isn’t where the money is invested geographically, but the fees and charges within the plans. This results in many complaints and bad reviews, especially when early surrender and redemption charges aren’t mentioned.

Moreover, whilst Tilney are regulated by the Financial Conduct Authority, the firms selling them overseas are not. That isn’t a problem in of itself, but don’t think you are getting enhanced protection.

The Labuan license, moreover, is more of an insurance license, than a financial license. Life insurance -related products can be connected to investments though; they are just more expensive than pure investment platforms.

What are the fees like within these products ?

It varies, but typically 1%-4% per year depending on many factors, including whether you contribute in these plans until the end of the term.

On the savings plans, you often can’t get bonuses if you fail to contribute every month, meaning you only get the fees and not bonuses.

Are there charges for getting out of BestInvest products?

The funds are liquid, so often UK investors can get out without penalty. However, if you have bought BestInvest through an offshore life insurance company, there are charges for getting out.

On lump sum products, the charges last for 5-14 years, depending on the terms and conditions of the product.

On regular savings plans, charges last for 5-30 years, depending on the terms of the contract.

If there are charges for getting out of the product, what can you do?

It depends. In some cases fund changes within the existing product makes sense. In other cases, you can do a maximum penalty free surrender. For example, if you have $100,000 in your account, you can withdraw $50,000 or $70,000 without penalty, and invest in a cheaper alternative.

How high this maximum penalty free surrender is usually depends on how long you have been invested in the account.

On day 1, you often have $0 penalty free surrenders available, especially on the savings plans. Most savings plans have a 1-2 year initial period. If you fail to pay in for this period, you lose all your money.

After that initial period, your surrender value gradually increases. So on a 25 year plan, for example, after 5 years, your surrender value may be 20%-30% of the account value. After 22 years, your surrender value may be 95% or more, but the specifics depend on the offshore life insurance provider.

However, over time, the amount you can withdraw penalty free increases.

Rendimiento de las inversiones

Are most clients happy with the returns?

In general, I have noticed a trend. Clients tend to be happy in the early years of expat accounts associated with this option.

This is often because the fees are lower in the early years, and also in part because of the welcome bonuses that third party providers give as an incentive to sign up.

However, by year five, six and seven, the situation starts to change. Very seldom have I found a happy client that has been in these policies for ten years or more.

Have the returns been good in 2022?

The stock market hasn’t performed well in 2022. Most markets are down about 10%-15% until May 4, 2022.

Therefore, we can’t blame Tilney for bad performance, but the average returns have been the same or lower than comparable funds in the market.

This suggests that the lower performance of the funds, compared to some competitors, doesn’t decrease risks for the clients.

Will the bonus make a difference?

Many of the providers that are sold in conjunction with this option, will claim that bonuses and extra allocations will decrease the fees substantially.

In reality, even adjusted for any bonus, this option is too expensive. That isn’t even taking into account the fact that there are so many terms and conditions for getting those bonuses in the first place.

Mistakes to avoid

In investing one of the biggest mistakes investors makes is called loss aversion in cognitive psychology. This means that if investors are down, or not doing well, they wait until the accounts are breaking even before selling.

A simple example would be if you have $100,000 in your account. The value is $95,000. After more reading, you know that deep down the fees are eating into returns. However, as the account briefly hit $101,000 before, you wait until the account recovers to $100,000+ before selling as you don’t want a loss.

I have even seen investors wait 2-10 years to avoid this loss.The rational thing to do is accept the $5000 loss in this situation, as that money can be made up quickly in a cheaper structure.

In addition to that, many investors think size is always good. Having 24/7 account access and log in, flash IT systems and an office in Mayfair doesn’t help client returns; lower fees and better funds would help that.

When do most people take action?

Due to the fact that the fees compound and get worse over time, most people wait 5-8 years+, before taking action as expats. It makes sense to do something sooner.

The reason that many people wait so long to take action is that first and even second year performance can be good, because welcome bonuses disguise the huge fees.

What are the positives and negatives about BestInvest?

The positives

- They are a large and established group……although large doesn’t mean better! It can just mean you are treated as a number.

- You probably won’t lose a lot of money in the funds. You might see a stagnating portfolio or get lowish returns, but you likely won’t see huge losses if you hold on long-term.

- For UK-only clients investing through SIPPs, the fees are more reasonable than for overseas clients. They typically charge 0.2%-0.4% service fees, depending on the account size. There are additional fund fees, however, which are quite high – as much as 1.60% per year.

- The funds are liquid, meaning they are daily priced. That doesn’t mean there aren’t charges for getting out of the investments, but they are not opaque and highly illiquid investments. In other words, if you have an $100,000 investment, even if the fees are $10,000 for getting out as an example, you will be able to exit quickly. This is unlike some other investments like some corporate bonds, which often can’t be sold before a specific date.

- A small percentage of their funds have performed well. However, as the article will explain in more detail below, it is often impossible to know which funds will do well in advance. Even their best performing funds, have also struggled to beat the market.

- They can be held in a tax-efficient manner, both in the UK, and outside the UK. However, so can many other investments, so this isn’t a positive compared to all other investments. It is merely a positive compared to some of the less tax-efficient options in the market. An example of a tax-inefficient option is usually sending money back to your home country, unless you are American.

The negatives of

In general, the negatives are far bigger than the positives, especially for expats. These negatives include:

1. The fees are high. Not the service fees but the fees within the funds. The Evelyn Partners BestInvest Defensive Portfolio and Evelyn Partners BestInvest Aggressive Portfolio both charge up to 1.60% per year + up to 5% initial charge. You can invest in index trackers from 0.03% per year. There is an incredible amount of academic data that shows that fees matter in investing over the long-term.

2. Fees in the UK aren’t the best compared to some providers, but pale in comparison with the charges in the overseas expat market. The reason is simple; there are multiple fees:

- 1.5% annual management charge (AMC)

- Over 2% per annum ongoing charge

- Up to 5% upfront

- Up to 1%-2% yearly depending on which bond and QROPS/provider is used.

To put it simply, you are getting numerous fees and these compound over time.

The life insurance fee, BestInvest fee, broker fees and sometimes QROPS and SIPPS fees all add up over the years.

3. Some brokers will claim that they have given discounted fees – in other words rebated the fees. Even if this is true, the net fees are still very high.

4. Numerous reviews online have suggested that withdrawing the money can be difficult, with plenty of procedures to jump over. In other words, in a digital age, the firm hasn’t adapted. Or at least, the international brokers selling Tilney, haven’t adapted. Often withdrawing and adding money online isn’t an option…….in 2020 this isn’t good enough.

5. Linked to the last point, as Tilney is sold overseas in conjunction with some old fashioned products, the procedures are even more complicated than in the UK.

Often to withdraw from these investments, the third party providers, often ask for physical paperwork, updated proof of address and other things.

I have helped people withdraw from these investments and it has often taken over 1 month, for some small silly reasons, like the signature on the withdrawal form isn’t an exact 100% match to the one they have on record!

Added to the hefty penalties for getting out of the investment, this was a tough pill to shallow for these investors

6. Passing the buck is easy. If a broker outsources their investment process, they will claim that is to reduce conflicts of interest.

This might have some merits. However, many brokers will be able to blame Evelyn Partners for under-performance, claiming that it is simply their job to “be the financial planner” and not “financial advisor”.

7. The outsourcing process often creates not only multiple layers of fees, but multiple layers of complexity.

8. The customer service has been referred to as “uncaring”. In effect this means that you are treated as customer number 102,022, rather than an individual. There have also been reports about regular trading and IT error.

9. It is a myth that Evelyn Partners can give you a better “risk adjusted return”.

Advocates for the company might argue that they won’t beat indexes like the S&P500, but they can offer you less volatile and safer returns.

This is largely a myth as you have addition risks going with this option, including “human error”. This also means that as the management team that runs your funds changes, your returns might change.

Another issue is complacency. Even many top performing managers can struggle after many good years – indeed today’s winners are often tomorrow’s losers in the fund industry.

Every dog has its day, as the expression goes, and relying on Evelyn Partners to beat the market on a regular basis, or even reduce your risk whilst failing to beat the market, is statistically unlikely.

10. Your mileage will certainly vary in terms of the service you get in the overseas market. Investor A, with advisory company A, might get much worse service than Investor B, with advisory company B. Even within those firms, the individual advisors will have contrasting levels of service.

11. Linked to point 10, they aren’t especially careful with the introducers they pick in the expat market. So your mileage will vary even more overseas, compared to in the UK.

Evelyn Partners Review: Final Thoughts

Evelyn Partners is a very expensive option for expat investors. Buying this product inside of the UK, is completely different to buying it as an expat, for the reasons given above.

Many expats buy into the plans thinking they are getting a UK-regulated solution, when that isn’t the case. Just because the funds are regulated in the UK, doesn’t mean the expat platforms are also regulated.

Regulation though, is the smaller issue compared to cost. In sum then, it is ironic that Evelyn Partners do a “spot the dog” feature, where they mention the worse performing funds.

The recent stock market declines and volatility in March 2020, caused due to the shutdown of the economy as a result of the global health care pandemic, is a good warning to potential investors.

Despite being told that diversified funds would reduce the volatility during bad times, even if they don’t beat the market long-term, Evelyn Partner’s funds haven’t beaten a diversified portfolio of index and bond funds.

Perhaps one day they could mention some of their own funds in the spot of the dog commentary!

What can you do if you have a Evelyn Partners policy offshore?

There are three options I have explored with people in the past: completely surrendering the policy, partially surrendering, and stopping contributions.

It isn’t easy to say which option is usually best for people, as that depends on each clients situation.

If you have a policy and would like a conversation please contact me via advice@adamfayed.com or use the chat function below.

Case study

To read a case study of an expat in an overpriced policy, and how I helped, please haga clic aquí.

As per Graham’s review, he explains the problem, how he got in contact me with and the end solution.

1-2 of my LinkedIn recommendations has also come from former BestInvest clients.

A more in-depth article

For an even more updated article, alongside customer reviews and questions at the bottom of the page, haga clic aquí.

The article goes into more detail about the kinds of insurance companies that are used in conjunction with BestInvest in the overseas market.

¿Le duele la indecisión financiera? ¿Quiere invertir con Adam?

Adam es un autor reconocido internacionalmente en temas financieros, con más de 225 millones de respuestas vistas en Quora.com y un libro muy vendido en Amazon.