Knighthead International provides annuity products that can suit expatriates and international investors seeking retirement income and long-term capital preservation.

While the products provide stability and international exposure, investors should weigh product complexity, capped returns, and limited direct access before committing.

Knighthead International is the brand name used by Knighthead Annuity & Life Assurance Company, an insurance company incorporated in the Cayman Islands.

Because of this structure, the company may also be referred to informally as Knighthead Annuity or Knighthead Cayman Islands.

Questo articolo tratta di:

- What does Knighthead do?

- Knighthead Annuity & Life Assurance Company products list

- What is the rating of Knighthead?

- Knighthead Annuity rates

- Pros and cons of Knighthead Annuity and Life Assurance Company

Punti di forza:

- Knighthead International focuses on annuities for retirement income and wealth preservation.

- Knighthead products are used in international financial planning and insurance-based investment strategies.

- Knighthead holds an A- (Excellent) financial strength rating from AM Best.

- Products include MYGAs, fixed index annuities, and immediate annuities.

I miei recapiti sono hello@adamfayed.com e WhatsApp +44-7393-450-837 se avete domande.

Le informazioni contenute in questo articolo hanno un valore puramente indicativo. Non costituiscono consulenza finanziaria, legale o fiscale e non rappresentano una raccomandazione o una sollecitazione a investire. Alcuni fatti potrebbero essere cambiati dal momento della stesura.

What is Knighthead Annuity & Life Assurance Company?

Knighthead Annuity & Life Assurance Company is an international insurance provider that specializes in rendite and retirement income solutions.

The insurer was established in 2014 and operates from the Cayman Islands, a jurisdiction known for hosting global insurance and reinsurance firms.

The company is regulated by the Cayman Islands Monetary Authority (CIMA) and is part of the broader Knighthead Insurance Group.

Knighthead’s business model centers on providing insurance-based financial products to wealth managers, consulenti finanziari, and institutional partners who serve international clients.

What is the rating of Knighthead insurance?

Knighthead Annuity & Life Assurance Co. currently holds financial strength ratings of A- (Excellent) from AM Best and A assicurazione financial strength rating from Kroll Bond Rating Agency (KBRA).

These ratings reflect the insurer’s capital strength, balance sheet stability, and ability to meet policyholder obligations.

However, ratings apply to the insurer itself and do not guarantee the performance of specific prodotti di investimento.

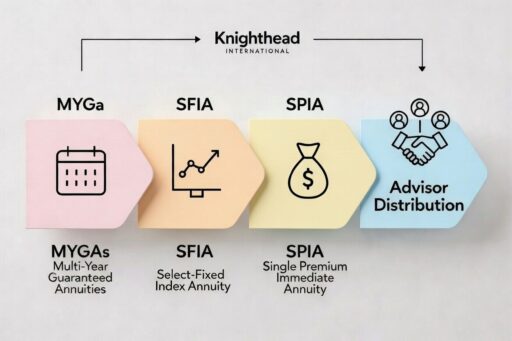

What are Knighthead International products?

Knighthead International focuses primarily on rendita-based insurance products.

These policies are designed to provide long-term income streams, capital growth potential, or tax-efficient wealth planning depending on the policy structure.

Multi-Year Guaranteed Annuities (MYGAs)

MYGAs provide a fixed interest rate for a defined period, typically between 3 and 10 years.

These products aim to offer stable returns without exposure to market volatility.

Gli esempi includono:

- Knighthead Safe Harbour MYGA

- Knighthead Navigator MYGA

Both products emphasize capital preservation and predictable growth.

Select Fixed Index Annuity (SFIA)

A fixed index annuity allows investors to earn returns linked to equity indices while maintaining protection against losses.

The contract usually includes a 0% floor, meaning the account value does not decline during market downturns.

Returns are capped, so investors may not receive the full upside of the underlying index.

Single Premium Immediate Annuity (SPIA)

An SPIA converts a lump sum investment into a guaranteed income stream, often beginning immediately after purchase.

This type of annuity is typically used for retirement income planning or as a private pension alternative.

These products are typically distributed through financial advisors and international insurance platforms rather than sold directly to retail customers.

Knighthead Cayman Islands Rates

Knighthead annuity rates vary by product, term length, and market conditions, but comparable fixed annuity structures have historically offered returns in the mid-single-digit range.

Multi-year guaranteed annuities generally offer fixed interest for a selected term, such as three, five, seven, or ten years.

Fixed index annuities provide returns linked to indices such as the S&P 500 but subject to caps.

Immediate annuities provide guaranteed income payments after a lump-sum premium.

Actual rates are provided through advisors rather than published publicly.

Is Knighthead Annuity safe?

Knighthead is regulated in the Cayman Islands and holds strong financial strength ratings from independent agencies.

The company operates under the supervision of the Cayman Islands Monetary Authority and is licensed as a Class D insurance and reinsurance entity.

While ratings such as A- indicate a relatively strong insurer, investors should still evaluate product structure, surrender terms, and counterparty risk before committing capital.

Is an annuity 100% safe?

No, an annuity is not 100% risk-free. While certain types of annuities, like fixed or immediate annuities, guarantee a steady income stream, the safety hinges on the financial strength of the issuing insurer.

If the insurance company faces financial difficulties, payments could be delayed or reduced.

Additionally, investment-linked or indexed annuities expose your policy value to market fluctuations, so returns are not guaranteed and could be lower than expected.

Knighthead International Pros and Cons

Knighthead International offers annuity products designed for capital preservation and retirement income, but like most annuities, they come with trade-offs such as capped returns and potential surrender charges.

Pro

- Competitive guaranteed annuity structures designed for long-term income

- Exposure to market gains through fixed index annuities without direct downside risk

- International insurer targeting expatriates and global investors

- Strong insurer ratings from AM Best and KBRA

Contro

- Products may be complex for investors unfamiliar with annuities

- Returns in indexed annuities are usually capped

- Surrender charges may apply for early withdrawals

- Product availability may depend on jurisdiction and financial adviser access

What is an annuity and why is it bad?

An annuity is a contract with an insurance company that promises future income. Despite the guarantee annuities can be limiting because they trade flexibility and liquidity for security.

Fees and administrative costs can erode returns over time, while certain products limit upside potential, so investors may not fully benefit from strong market growth.

This combination makes annuities unsuitable for those seeking short-term access, higher returns, or investment flexibility. That doesn’t make them bad—only intended for long-term security and stability.

VUL vs Annuities: Swiss Life Alpha Plus and Knighthead International Compared

Variable universal life (VUL) policies like Swiss Life Alpha Plus offer market-linked growth and life coverage, while Knighthead International annuities provide predictable, lower-risk income.

For investors deciding between life insurance with investment potential and annuities, the differences between a VUL policy and a Cayman Islands annuity can be significant.

Investment Structure

- Swiss Life Alpha Plus (VUL) allows policyholders to allocate premiums across equity, bond, or balanced funds. Returns fluctuate with market performance, offering higher potential upside but also greater volatility.

- Knighthead International annuities (MYGAs, fixed index, and immediate annuities) provide guaranteed or index-linked income with limited exposure to market risk. Growth is predictable but often capped.

Income Flexibility

- A VUL policy can grow a cash value over time that policyholders can access through partial withdrawals or policy loans, though fees and market performance affect liquidity.

- Knighthead annuities convert premiums into a steady income stream, either immediately (SPIA) or after a term (MYGA), offering predictable retirement cash flow but limited early access without surrender penalties.

Risk and Return

- VULs like Alpha Plus expose investors to market risk but can generate significant long-term returns, which makes them suitable for those with higher risk tolerance and a long-term horizon.

- Knighthead annuities prioritize capital preservation and steady returns, appealing to investors seeking lower risk and guaranteed income, though upside is limited.

Swiss Life Alpha Plus targets investors who want life coverage and are comfortable with market-linked growth, fees, and active fund management.

Knighthead International annuities target investors who want predictable income, capital preservation, and lower volatility, especially expatriates or international clients relying on advisor-managed products.

Domande frequenti

What insurance companies have an A++ rating?

An A++ rating from AM Best is the highest financial strength category. Major insurers with this rating historically include companies such as Northwestern Mutual and New York Life.

Why are insurers taking your money to the Cayman Islands?

Some insurance companies operate in jurisdictions like the Cayman Islands because the regulatory framework supports international insurance and reinsurance markets.

Cayman is widely used for assicurazione globale structures and cross-border retirement products.

The Cayman Islands Monetary Authority regulates these insurers and requires capital standards, licensing, and ongoing supervision.

What is the highest rated annuity company?

The highest rated annuity companies are typically those with strong financial strength ratings from agencies like AM Best, Moody’s, and S&P, such as Prudential, Allianz, and New York Life.

Ratings can change over time and they don’t guarantee future performance, so always check the latest insurer ratings before investing.

Has anyone ever lost money in an annuity?

Yes, it is possible to lose money in certain annuities, especially variable annuities where returns rely on market performance.

Fees, early surrender charges, and poor investment choices can also reduce or eliminate gains.

How long can an annuity last?

An annuity can last for a fixed period (e.g., 5–20 years) or lifetime based on the product.

Lifetime annuities provide income for the rest of the annuitant’s life, while fixed-term annuities pay for a set number of years.

Siete afflitti dall'indecisione finanziaria?

Adam è un autore riconosciuto a livello internazionale in materia finanziaria con oltre 830 milioni di visualizzazioni di risposte su Quora, un libro molto venduto su Amazon e un contributo su Forbes.