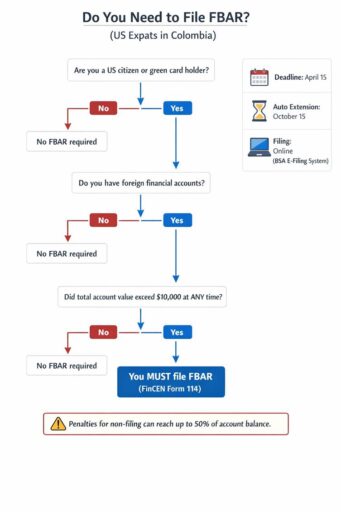

US expats in Colombia must file an FBAR (FinCEN Form 114) if the total value of their non-US bank and financial accounts exceeded 10,000 USD at any time during the year.

This applies even if no US tax is ultimately due.

The FBAR is filed electronically with FinCEN, not the IRS, and penalties for non-compliance can be severe.

As a US expat in Colombia, you often must also consider Colombian tax residency rules and local filing obligations when planning your overall tax and reporting strategy.

Este artículo trata:

- Do expats pay US taxes?

- What is FBAR?

- Is FBAR only for expats?

- How do you know if you qualify for the foreign earned income exclusion?

- Who is eligible for the US foreign tax credit?

- What is the last day to file FBAR?

Principales conclusiones

- US expats in Colombia must file FBAR if their non-US accounts exceed 10,000 USD.

- FBAR is filed electronically with FinCEN and is separate from tax return.

- The FBAR deadline is April 15 with an automatic extension to October 15.

- Efficient strategies combine FEIE, Foreign Tax Credits, and Colombian tax planning.

Mis datos de contacto son hello@adamfayed.com y WhatsApp +44-7393-450-837 si tiene alguna pregunta.

La información contenida en este artículo no constituye asesoramiento fiscal y puede haber cambiado desde el momento de su redacción. Puedo ponerle en contacto con expertos fiscales para su situación específica.

Do You Have To File US Taxes If You Live Abroad?

US citizens and green card holders generally must file a US tax return on worldwide income even when they live full-time in Colombia.

Living abroad may change how your income is taxed through exclusions and credits, but it does not remove your filing obligation.

US expats in Colombia must understand that US tax filing is based on citizenship, while Colombian tax filing is based largely on residency.

When Expats Must File a US Tax Return?

US expats must file a tax return if their gross income exceeds the standard filing threshold for their filing status (single, married filing jointly, etc.) for that year.

Expats receive an automatic filing extension to June 15, but interest on taxes owed still accrues from April 15.

Common Tax Obligations for US Expats

US expats in Colombia often face several recurring US tax obligations:

- File Form 1040 reporting worldwide income

- Report foreign accounts on FBAR (FinCEN Form 114) if thresholds apply

- File Form 8938 (FATCA) if asset thresholds are met

- Use Form 2555 (FEIE) or Form 1116 (Foreign Tax Credit) to reduce double taxation

What Are The US Tax Forms For Expats?

For a typical US expat in Colombia, the most important forms are Form 1040, Form 2555, Form 1116, and FinCEN Form 114 (FBAR).

US expats generally use the same core forms as domestic taxpayers but add specific international forms to claim benefits and meet reporting rules.

Form 1040 and Foreign Income Reporting

Form 1040 is the main US individual income tax return and must include worldwide income, including salaries, self-employment income, pensions, and investment income from foreign and US sources.

Even if you expect to exclude much of your income under FEIE or offset it with foreign tax credits, you must first report it on Form 1040.

Form 2555 for Foreign Earned Income Exclusion

Form 2555 is used to claim the Foreign Earned Income Exclusion.

To use it, you must have foreign earned income, your tax home must be in a foreign country, and you must meet either the bona fide residence test or the physical presence test.

Form 1116 for Foreign Tax Credit

Form 1116 allows you to claim a credit for income taxes paid or accrued to Colombia against your US tax on the same income.

You may sometimes use both FEIE and the Foreign Tax Credit, but you cannot claim a credit for foreign taxes on income you have already excluded under FEIE.

Choosing the right mix is a key part of efficient tax planning for US expats in Colombia.

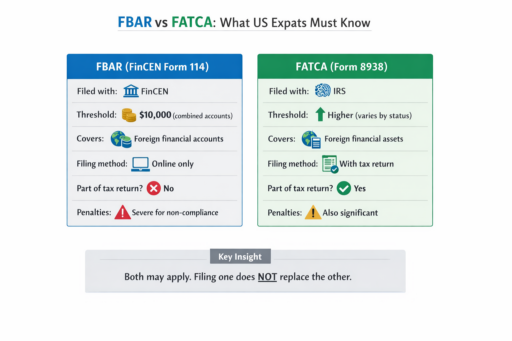

FinCEN Form 114 (FBAR)

FinCEN Form 114 (FBAR) reports foreign financial accounts to the US Treasury.

It is filed electronically through the BSA E-Filing System and does not calculate tax.

What Is FBAR Reporting?

FBAR reporting requires US persons to disclose certain foreign financial accounts if their combined value exceeds 10,000 USD at any point during the year.

It is an information-only filing and does not directly assess tax, but penalties for failing to report can be very high.

The FBAR regime applies broadly to accounts held outside the United States, including bank, securities, and certain other financial accounts.

Do Expats Need To File FBAR In Colombia?

Yes, US expats living in Colombia must file FBAR if they meet the account and threshold criteria, just as if they lived anywhere else outside the US.

The fact that your accounts are in Colombia rather than another country does not change the core FBAR rules.

Failure to file an FBAR can result in significant civil penalties and, in extreme cases, criminal consequences.

The penalty for willful violations may reach up to 50% of the account balance.

What Are FBAR Filing Requirements For US Expats In Colombia?

US expats in Colombia generally must file an FBAR if they meet the US person, account authority, and reporting threshold requirements.

FBAR must be filed when:

- You are a US person

- You have a financial interest in or signature or other authority over at least one foreign financial account

- The aggregate value of all such accounts exceeds 10,000 USD at any time during the year.

The 10,000 USD threshold is measured in aggregate across all accounts, not per account.

Foreign Financial Accounts That Must Be Reported

Reportable accounts generally include bank accounts, brokerage accounts, certain pension accounts, and accounts where you have financial interest or signature authority.

Many US expats in Colombia hold checking accounts, USD savings accounts, CDTs, or brokerage accounts that may fall under these rules.

How To File FBAR As A US Expat Living In Colombia?

You file FBAR electronically using FinCEN’s BSA E-Filing System; there is no paper filing option.

The process involves gathering account details, calculating maximum balances in US dollars, completing FinCEN Form 114 online, and submitting it by the deadline.

Step-by-Step FBAR Filing Process

1. Determine whether your aggregate foreign accounts exceeded 10,000 USD at any time in the year.

2. Gather required account data and compute maximum balances in USD.

3. Access the BSA E‑Filing System FBAR page.

4. Choose the individual filing option and complete filer information.

5. Enter each reportable account, including maximum value and institution details.

6. Review the form for completeness and correct any validation errors.

7. Submit the FBAR electronically and save the confirmation and a copy of the submission for your records.

If you find errors after submission, you can file an amended FBAR through the same system.

What Is The Deadline For FBAR Filing?

For calendar‑year taxpayers, the FBAR deadline is April 15 following the end of the calendar year being reported.

For example, FBARs for the 2025 calendar year are due April 15, 2026.

Filers who miss the April deadline may generally rely on an automatic extension.

Is there an extension for FBAR?

Yes, FBAR benefits from an automatic extension to October 15 for filers who do not submit by April 15.

You do not need to file a separate extension request, unlike with many income tax return extensions.

However, if you anticipate difficulty gathering your Colombian account data, it is wise to prepare well ahead of April 15 so you can file accurately and early when possible.

The automatic extension is a safety net, not a reason to delay without planning.

What happens if you miss the FBAR deadline?

If you miss the FBAR deadline and do not file by October 15, you may be subject to FBAR penalties unless you can demonstrate reasonable cause and correct the failure promptly.

Penalties can be imposed per violation and can quickly become substantial for multiple accounts or multiple years.

If you realize you have missed past FBARs, you should seek advice on current IRS and FinCEN compliance procedures.

These may allow you to file late with reduced or no penalties, depending on your circumstances.

Acting proactively usually yields a better outcome than waiting.

How To File Taxes In Colombia?

To file taxes in Colombia, you first determine whether DIAN considers you a tax resident and whether you exceed Colombian filing and income thresholds.

If so, you typically file an annual income tax return (Declaración de Renta) with DIAN.

The Colombian tax year is the calendar year, and DIAN sets annual filing deadlines that vary by type of taxpayer and ID number ranges.

As a US expat, you may need a Colombian tax ID (NIT).

What Is The Tax Residency In Colombia?

Individuals are generally considered Colombian tax residents if they spend more than 183 days in the country within a 365-day period.

Colombian tax residents are generally taxed on their worldwide income, while non-residents are typically taxed only on their Colombian‑source income.

This means a US expat who becomes a Colombian tax resident can face worldwide taxation in both countries, making intelligent use of FEIE and Foreign Tax Credits essential.

What Are The Tax Benefits For US Expats In Colombia?

US expats in Colombia can use US tax benefits such as the Foreign Earned Income Exclusion, the Foreign Tax Credit, and the Child Tax Credit.

Through effective utilization of these benefits, one can reduce or eliminate US tax on income already taxed in Colombia.

Coordinating these US benefits with Colombian rules around residency, deductions, and credits is crucial for efficient planificación fiscal.

Many expats analyze whether the Foreign Earned Income Exclusion, the Foreign Tax Credit, or a combination of both produces the lowest overall tax burden.

Maintain bank statements, account records, and USD conversion calculations for each foreign account. FBAR records should be kept for at least five years.

Is there a tax treaty between the US and Colombia?

As of early 2026, there is no fully effective comprehensive income tax treaty between the United States and Colombia.

Instead, relief from doble imposición is typically achieved through US domestic mechanisms, primarily the Foreign Tax Credit on Form 1116 and, in some cases, the FEIE on Form 2555.

On the Colombian side, you must follow DIAN’s domestic rules for foreign tax and credit treatment.

Who qualifies for Foreign Earned Income Exclusion (FEIE)?

To qualify for FEIE, you must have foreign earned income, your tax home must be in a foreign country, and you must meet either the bona fide residence test or the physical presence test.

The bona fide residence test generally requires you to be a bona fide resident of a foreign country, such as Colombia, for an entire tax year.

On the other hand, the physical presence test requires at least 330 full days in one or more foreign countries in a 12-month period.

Who qualifies for the Foreign Tax Credit?

You generally qualify for the Foreign Tax Credit if you pay or accrue foreign income taxes to Colombia on income that is also subject to US tax, and the tax is a legal and actual foreign tax liability.

The credit is claimed on Form 1116 and is subject to limitation formulas that cap the credit at the portion of US tax attributable to foreign‑source income.

This credit is particularly important for US expats who are Colombian tax residents paying Colombian income tax at rates equal to or higher than US rates on the same income.

Who qualifies for the Child Tax Credit?

US expats may qualify for the Child Tax Credit if they have a qualifying child who meets age, relationship, residency, and identification tests.

Simultaneously, the expat’s income should fall within applicable thresholds.

What are the differences between FBAR and FATCA?

FBAR reports foreign financial accounts to FinCEN when the 10,000 USD threshold is met, while FATCA Form 8938 reports broader foreign financial assets to the IRS under higher thresholds.

FBAR is filed separately through FinCEN’s BSA system.

Form 8938 is included with your federal tax return (Form 1040) and applies different reporting thresholds and asset scope.

Preguntas frecuentes

How much does it cost to file an FBAR?

FinCEN does not charge a fee to file FBAR; the BSA E‑Filing System is free to use.

Your only cost is any fee you choose to pay to a tax professional or software provider to assist you.

Can I file FBAR by myself?

Yes, individuals can file FBAR themselves online using the BSA E-Filing System’s individual filing option.

Many expats file on their own, though some prefer to use a professional due to the complexity of their accounts.

Is FBAR filed every year?

You must file FBAR for each year in which you meet the reporting threshold; it is an annual requirement tied to the calendar year.

If in a later year your foreign accounts never exceed 10,000 USD in aggregate, you do not file for that year.

Which is better, the foreign earned income exclusion or the foreign tax credit?

Neither is universally better. The optimal choice varies based on your income level, Colombian tax rate, and mix of income types.

Many US expats in Colombia model both FEIE and Foreign Tax Credit scenarios each year and sometimes combine them to minimize overall tax.

¿Le duele la indecisión financiera?

Adam es un autor reconocido internacionalmente en temas financieros, con más de 830 millones de respuestas en Quora, un libro muy vendido en Amazon y colaborador de Forbes.