¿Cuáles son las mejores opciones de inversión para los expatriados británicos?

Los expatriados británicos suelen elegir entre invertir en su país de residencia, invertir en el Reino Unido o utilizar plataformas extraterritoriales. La elección correcta depende de su estatus de residencia, situación fiscal y objetivos a largo plazo.

Aunque es imposible hablar de todos los países del mundo, dados los más de 180 lugares donde residen expatriados británicos, intentaré generalizar, basándome en la evidencia y en mi experiencia como británico vivir en el extranjero.

Este artículo se centrará en las mejores opciones de inversión para los expatriados británicos que residen en el extranjero, más que para los expatriados no británicos que viven en el Reino Unido, aunque habrá algunos puntos en común en el análisis.

Mis datos de contacto son hello@adamfayed.com y WhatsApp +44-7393-450-837 si tiene alguna pregunta.

La información contenida en este artículo es meramente orientativa. No constituye asesoramiento financiero, jurídico o fiscal, ni una recomendación o solicitud de inversión. Algunos hechos pueden haber cambiado desde el momento de su redacción.

Cómo invertir como expatriado en el Reino Unido

Empiece por determinar dónde reside fiscalmente y si tiene previsto regresar al Reino Unido. Esto determinará sus opciones de inversión y cómo tributan.

Algunos expatriados priorizan el acceso y la flexibilidad utilizando plataformas reguladas en su país de residencia.

Otros mantienen vínculos con el Reino Unido a través de pensiones o propiedades, especialmente si esperan jubilarse allí.

Un tercer grupo utiliza plataformas extraterritoriales o internacionales para una mayor portabilidad entre jurisdicciones.

La mejor opción suele combinar dos o más estrategias, en función de sus objetivos, apetito de riesgo y obligaciones transfronterizas.

1. Inversiones de expatriados británicos en su país de residencia

Como expatriado británico, puede invertir directamente en su país de residencia, ya sea España, Dubai, Hong Kong, Singapur o cualquier otro.

Las opciones incluyen inversiones bursátiles locales, bienes inmuebles y depósitos bancarios. Esta sección repasará cada una de las opciones:

Bolsa local

Si vive en un lugar con un mercado de valores de calidad, que ha tenido entre 100 y 200 años de gran rendimiento como los mercados de valores de EE.UU., tiene sentido invertir con una empresa de corretaje local.

Del mismo modo, algunos países dificultan mucho, desde el punto de vista fiscal, la inversión en el extranjero. También es el caso de EE.UU., donde las inversiones en el extranjero resultan fiscalmente ineficaces para los residentes fiscales estadounidenses.

Así pues, si usted es residente fiscal británico en Estados Unidos, casi siempre tiene sentido invertir localmente, desde el punto de vista fiscal.

En comparación, si vives en un lugar como China, Colombia o cualquier otro lugar con un mercado de valores bastante inestable, estás asumiendo muchos más riesgos al invertir localmente.

Conocí a muchos expatriados británicos mientras vivía en China, que se dejaron llevar por todo el “El crecimiento de China“, olvidando que el PIB y el crecimiento bursátil no están relacionados.

Por supuesto, es posible tener una cuenta de corretaje en el país A, y se centra en la inversión en acciones en el país B.

Por ejemplo, puede abrir una cuenta de inversión en la mayoría de los países, lo que le permite operar en los mercados de valores de Estados Unidos, Reino Unido y Europa continental.

El problema es que si la plataforma de inversión o el corredor de bolsa están demasiado localizados, es posible que no le permitan seguir invirtiendo si abandona ese país.

Como expatriado, especialmente si se desplaza mucho, tiene sentido disponer de una opción portátil que garantice que sus cuentas sigan funcionando si se marcha.

No sólo eso, sino que, a menos que viva en un entorno de ganancias de capital 0%, puede verse afectado por impuestos muy elevados si invierte automáticamente en su país de residencia.

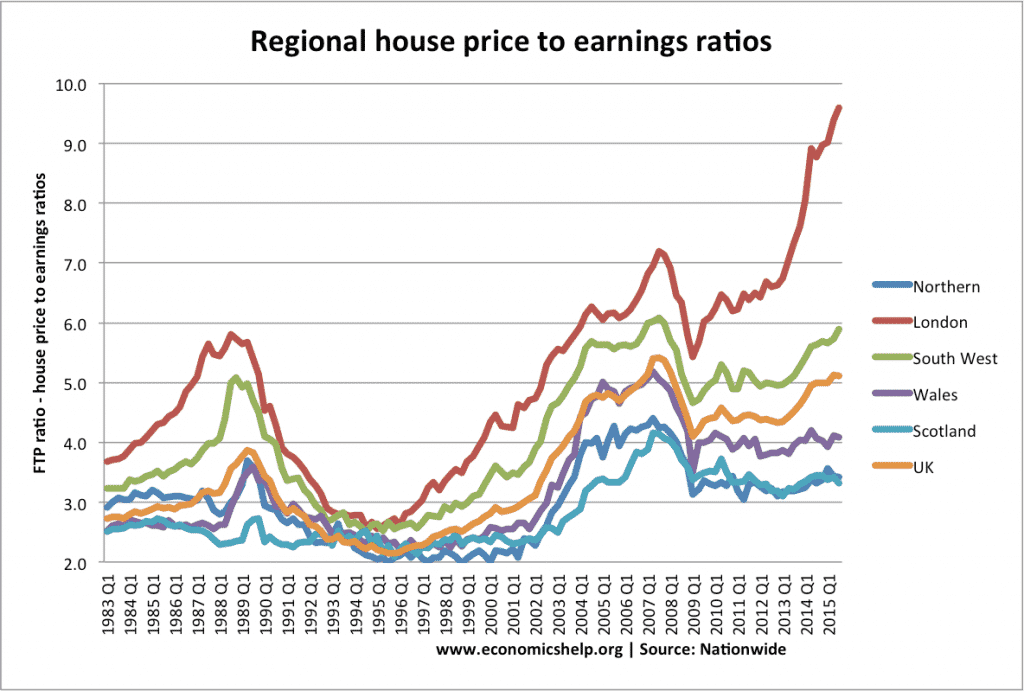

Inmobiliaria local

Otra opción es comprar propiedades inmobiliarias locales en el país donde reside actualmente. En general, esta opción tiene más sentido si piensa quedarse en ese lugar a largo plazo y utilizar la propiedad como vivienda en lugar de como mera inversión.

Para quienes estén pensando en alquilar propiedades, es importante sopesar los riesgos.

El sector inmobiliario es un activo ilíquido y su venta puede resultar complicada, sobre todo en mercados en los que el ordenamiento jurídico, el idioma o los derechos de propiedad difieren de los que conocen los inversores del Reino Unido.

Esto es especialmente relevante para los expatriados británicos que viven fuera de entornos anglófonos nativos.

Además, las valoraciones inmobiliarias en muchos mercados emergentes han aumentado considerablemente en los últimos 10-15 años, acortando distancias con los precios de la vivienda en el Reino Unido.

Antes de 2007-2010, los inversores solían recibir un descuento para compensar los riesgos adicionales.

Hoy en día, algunos mercados inmobiliarios extranjeros son tan caros o más que el Reino Unido.

Incluso algunos mercados desarrollados se han revalorizado significativamente en relación con los valores inmobiliarios del Reino Unido.

Banca local

Todos los expatriados necesitan un banco para cubrir sus necesidades diarias, y los empleadores suelen abrir cuentas locales cuando se trasladan al extranjero.

Sin embargo, muchos expatriados también se benefician de las soluciones bancarias de terceros países, sobre todo en jurisdicciones con controles de divisas más flexibles.

Por ejemplo, los expatriados en países como China o Vietnam, donde mover dinero a través de las fronteras puede ser difícil, a menudo optan por ingresar parte de su salario en cuentas en lugares como Hong Kong o Singapur.

Lo hacen para garantizar unas transferencias internacionales más fluidas y una mayor flexibilidad monetaria.

Dicho esto, los depósitos bancarios no deben considerarse una inversión real. En la mayoría de los países, los tipos de interés de los depósitos son inferiores a la inflación, lo que significa que su poder adquisitivo disminuye con el tiempo.

En algunos mercados emergentes, puede encontrar tipos de depósito de dos dígitos. sin embargo, suelen ir acompañados de elevados riesgos de divisa e inflación.

2. Opciones de inversión en el Reino Unido para expatriados británicos

¿Pueden los expatriados británicos seguir invirtiendo en el Reino Unido? Sí, pero tiene sus contrapartidas.

Aunque se puede enviar dinero de vuelta para invertir en acciones británicas o en cuentas existentes, los expatriados suelen perder el acceso a ventajas fiscales como las ISA, y se enfrentan a un escrutinio adicional.

Inversiones en bolsa británica e ISA

Algunos expatriados británicos optan por enviar dinero a casa e invertir a través de plataformas radicadas en el Reino Unido.

Esto es especialmente cierto en el caso de quienes realizan misiones de corta duración o mantienen estrechos vínculos con el Reino Unido.

Puede tratarse de inversiones en bolsa, pensiones o cuentas existentes en el Reino Unido.

Aunque esto pueda parecer familiar o cómodo, no siempre es fiscalmente eficiente o práctico.

De hecho, para la mayoría de los expatriados de larga duración, invertir en su país de origen conlleva importantes limitaciones:

- Las ISA no están disponibles para los no residentes en el Reino Unido, por lo que sus ganancias pueden estar sujetas a impuestos tanto en el Reino Unido como en su país actual.

- Los corredores y bancos británicos pueden restringir el acceso o cerrar las cuentas si ya no eres residente en el Reino Unido.

- La prueba de residencia legal del HMRC implica que las transferencias y conexiones regulares con el Reino Unido pueden desdibujar su estatus de residencia fiscal, desencadenando potencialmente obligaciones fiscales.

- Los controles contra el blanqueo de dinero pueden retrasar o complicar las transacciones, ya que los bancos piden cada vez más pruebas de ingresos o del origen de los fondos a los clientes expatriados.

Aunque las inversiones basadas en el Reino Unido pueden tener sentido en casos concretos, como mantener activa una pensión existente o invertir antes de la reubicación, no suelen ser la opción más eficiente para los expatriados permanentes.

Inmobiliario en el Reino Unido

Muchos expatriados británicos están interesados en alquilar propiedades en el Reino Unido, pero la rentabilidad se ha vuelto más difícil con el tiempo.

Los recientes cambios fiscales han reducido el atractivo de los arrendadores no residentes, como el aumento de los derechos de timbre, la reducción de la desgravación de los intereses hipotecarios y la ampliación de los impuestos. normas del impuesto sobre plusvalías.

Los dos principales partidos apoyaron aumentar los impuestos a los compradores extranjeros en sus manifiestos de 2019, endureciendo aún más el panorama.

El acceso a las hipotecas también se ha vuelto más limitado, ya que muchos prestamistas británicos imponen requisitos más estrictos a los expatriados. Dicho esto, sigue habiendo hipotecas para expatriados, aunque con umbrales más elevados.

A pesar de estos obstáculos, las valoraciones inmobiliarias en el Reino Unido, especialmente fuera de las grandes ciudades, pueden ser más razonables en comparación con algunos mercados mundiales sobrecalentados.

Así que si puede encontrar una compra excelente, adquirir una propiedad en el Reino Unido no es la peor opción.

Simplemente es mucho más difícil que antes hacerlo de forma rentable.

Depósitos bancarios en el Reino Unido

Como ya se ha mencionado, no suele tener sentido que los expatriados británicos envíen grandes cantidades de dinero a una cuenta bancaria del Reino Unido con fines de inversión.

Otra cosa son las pequeñas cantidades de dinero para pagar facturas. También tiene sentido, al menos, mantener abiertas cuentas bancarias en el Reino Unido, con pequeños saldos, por si alguna vez regresas a ese país.

Esto también le permite mantener una “dirección de corresponsalía” en el Reino Unido mientras sigue viviendo en el extranjero.

3. Invertir en un tercer país (Inversiones offshore para expatriados británicos)

Los expatriados británicos pueden invertir a través de plataformas con sede en terceros países, que son jurisdicciones situadas fuera del Reino Unido y de su país de residencia.

Algunos ejemplos de terceros países podrían ser Luxemburgo, la Isla de Man (técnicamente parte del Reino Unido pero con entornos normativos diferentes), las Bermudas y cualquier otro país con ganancias de capital 0%.

Inversión bursátil internacional a través de plataformas extraterritoriales

Hay muchas ventajas para los expatriados que invierten con una solución de un tercer país.

La principal ventaja es que una cuenta para expatriados en la Isla de Man, Bermudas, Luxemburgo u otra jurisdicción popular es eficiente desde el punto de vista fiscal y tiene más probabilidades de ser transferible.

Con portátil me refiero a que, como muchos proveedores internacionales están especializados en el mercado de expatriados, permiten a los clientes actualizar simplemente sus datos en línea, si se trasladan del país A al país B.

Las únicas excepciones suelen ser si te trasladas a Estados Unidos o a un país sometido a sanciones estadounidenses, como Irán o Venezuela, lo que ocurre con muy pocos expatriados británicos.

Desde el punto de vista fiscal, es bastante esencial invertir también en un entorno de plusvalías 0%.

Los impuestos sobre las plusvalías pueden ascender a cientos de miles o más, sobre todo si es un inversor a largo plazo.

Muchas personas no tienen en cuenta la importancia de los impuestos en la ecuación de costes, sobre todo si empiezan con una inversión pequeña. Sin embargo, las pequeñas inversiones mensuales se acumulan con los años.

La principal razón que impide a la gente invertir en bolsa es el miedo.

Normalmente, tras una noticia negativa sobre unas elecciones, un virus o la economía, la gente se preocupa e intenta tomar el tiempo del mercado, es decir, decidir cuál es el mejor momento para invertir.

Esto es casi imposible de hacer. En un evento anterior con clientes, Kevin O'Leary, estrella de Shark Tank (antes Dragons Den), admitió que había intentado cronometrar los mercados y había fracasado:

Si alguien que vale unos $400 millones no puede hacerlo, entonces muy poca gente (si es que hay alguna) puede.

Inmobiliario internacional

Invertir en propiedades en un tercer país conlleva algunos de los mismos riesgos que comprar en su país de residencia.

Los bienes inmuebles siguen siendo un activo ilíquido, y usted puede enfrentarse a problemas legales o lingüísticos en jurisdicciones desconocidas.

Las valoraciones cada vez más altas en innumerables lugares también hacen que esta opción sea cada vez más arriesgada, a menos que se elija muy sabiamente.

Dicho esto, el mercado inmobiliario internacional ofrece claras ventajas. Puede buscar las mejores ofertas en todo el mundo, comparando la rentabilidad de los alquileres, los regímenes fiscales y las perspectivas de crecimiento a largo plazo.

No hace falta que elijas Estados Unidos, Australia, Canadá, Bulgaria o Rumanía.

Basta con hablar con un expatriado del sector inmobiliario, analizar objetivamente las valoraciones y los rendimientos de los alquileres y tomar decisiones basadas en datos, no en exageraciones.

En muchos países, la propiedad de bienes inmuebles también abre la puerta a planes de ciudadanía por inversión. En otras palabras, puede obtener un segunda residencia, a cambio de la propiedad.

Esto es especialmente popular entre los expatriados que han terminado su asignación laboral pero aún quieren vivir en el extranjero.

Cuenta bancaria offshore para expatriados

Aunque hay que volver a mencionar que las cuentas bancarias no deben utilizarse como inversiones, tener un cuenta bancaria para expatriados en un tercer país tiene mucho sentido.

La principal ventaja es la portabilidad. Si su banco sabe que usted es un expatriado, es mucho menos probable que le cierren la cuenta, le congelen los fondos o le pidan demasiada documentación cuando se traslade.

Las cuentas bancarias aptas para expatriados suelen admitir varias divisas, ofrecer transferencias internacionales en línea y cumplir las normas bancarias internacionales.

Aunque cuentas extraterritoriales no están diseñadas para el crecimiento de las inversiones, suelen ser una parte fundamental de un plan financiero internacional bien estructurado.

Ofrecen flexibilidad, control de divisas y, a veces, acceso a servicios financieros globales que los bancos locales podrían no ofrecer.

¿Los expatriados británicos pagan impuestos sobre las inversiones?

Si no es residente a efectos fiscales en el Reino Unido:

- No paga impuestos en el Reino Unido por las rentas o plusvalías obtenidas en el extranjero (excepto por los bienes inmuebles en el Reino Unido).

- Sin embargo, las rentas de inversión procedentes del Reino Unido, como los dividendos o las rentas de alquiler de bienes inmuebles en el Reino Unido, pueden seguir gravándose.

- Las ISA dejan de estar exentas de impuestos una vez que se convierte en no residente. No se permiten nuevas aportaciones y las ganancias pueden tributar en tu país de residencia.

La mayoría de los países gravan la renta mundial, por lo que su legislación fiscal local puede exigirle que declare y pague impuestos sobre sus inversiones aunque éstas se encuentren en paraísos fiscales o en el Reino Unido.

Muchas jurisdicciones tienen acuerdos de doble imposición con el Reino Unido para evitar ser gravado dos veces, pero debe presentar la declaración correctamente para beneficiarse de ellos.

Las inversiones en jurisdicciones como la Isla de Man pueden ofrecer aplazamiento o eficiencia fiscal, pero no están exentas de impuestos a menos que se estructuren correctamente.

Consejos de inversión para expatriados británicos

- Aclare pronto su situación fiscal. Sepa si sigue siendo residente fiscal en el Reino Unido o no, ya que ello afecta a si las cuentas individuales o las inversiones basadas en el Reino Unido son ventajosas.

- Evite el exceso de concentración. Diversificar las jurisdicciones para reducir el riesgo geopolítico, cambiario y normativo.

- Utilice plataformas adaptadas a expatriados. Elija proveedores internacionales familiarizados con el cumplimiento transfronterizo y la portabilidad.

- Mantenga accesibles los fondos de emergencia. No bloquee todo su capital en propiedades ilíquidas o vehículos a largo plazo.

- Consulte su plan a la hora de trasladarse. Cada movimiento puede cambiar su estrategia óptima debido a nuevas normas fiscales o al acceso a la inversión.

- Considere la exposición a la moneda local. Sopese si le conviene cubrirse o aceptar el riesgo de cambio en función de sus objetivos a largo plazo.

Invertir en el Reino Unido: Reflexiones finales

En general, tiene sentido centrarse en las opciones de “terceros países” o extraterritoriales cuando se trata de realizar operaciones bancarias e inversiones como expatriado en el Reino Unido. Este es especialmente el caso de quienes se trasladan de un país a otro cada pocos años.

Las razones son bastante sencillas. Suele ser más eficiente desde el punto de vista fiscal y está especializada en el nicho de los expatriados.

Las principales excepciones a esta norma se dan si vive en Estados Unidos o si su destino es de corta duración. Si se trata de una misión de corta duración, se le suele considerar residente fiscal en el Reino Unido en cualquier caso.

La caída de los mercados que se ha producido durante el mes de marzo de 2020, tras los inesperados cierres gubernamentales a nivel mundial, demuestra una vez más que nadie puede predecir los mercados bursátiles. Por lo tanto, lo mejor es tener un plan a largo plazo que se pueda seguir en las buenas y en las malas.

A largo plazo, invertir tiene mucho más sentido que mantener el dinero en efectivo.

¿Le duele la indecisión financiera?

Adam es un autor reconocido internacionalmente en temas financieros, con más de 830 millones de respuestas en Quora, un libro muy vendido en Amazon y colaborador de Forbes.

Lecturas complementarias

Soy el escritor más consultado en la plataforma de redes sociales Quora sobre inversión y finanzas personales, con más de 218 millones de visitas en los últimos años.

Comparto regularmente respuestas de esa plataforma en adamfayed.com. En las respuestas a continuación, respondo a las preguntas incluyendo:

- ¿Qué necesita saber un principiante para invertir en bolsa? Y lo que es más importante, ¿qué aspectos suelen descuidar los principiantes?.

- ¿Es posible mantenerse económicamente con una cartera de inversiones en bolsa? En otras palabras, ¿puede dejar de trabajar gracias a sus inversiones en bolsa? ¿En qué se equivoca la gente cuando piensa en “ingresos pasivos”?

- Si quiere hacerse millonario invirtiendo en bolsa, ¿cuánto necesita invertir cada mes o cada año? ¿Es menos o más de lo que cabría esperar?

Como anticipo de las respuestas he copiado una sección a continuación:

Lo básico en cualquier ámbito es clave. Si quieres ponerte en forma, lo básico es una buena alimentación, ejercicio y postura.

Lo mismo ocurre con la inversión. Es un mito que haya que ser muy inteligente para ser un buen inversor, como dice la cita siguiente:

Lo que la gente necesita es

1. Empezar de verdad - 80% del éxito es simplemente aparecer. Lo mismo ocurre con la inversión. Abrir una cuenta de inversión parece una obviedad, pero es la clave. Más allá de eso, trucos sencillos como invertir un día después de que te paguen pueden aumentar drásticamente la cantidad que inviertes. Algunos estudios han demostrado incluso que la gente es capaz de invertir 3 veces más invirtiendo a principios de mes, en lugar de a finales. Con el tiempo, cuánto invierta y durante cuánto tiempo será incluso más importante que los rendimientos compuestos.

2. Tiempo y paciencia - La forma más fácil de ganar dinero, con menos riesgo, es aprovechar el tiempo. Las acciones son arriesgadas si sólo las mantienes un año. Incluso algunas de las apuestas ETF e índices lo son. Si los mantienes durante décadas, no lo son. No confundas volatilidad y riesgo.

3. Diversificar. Si mantiene acciones y bonos juntos, es aún más seguro:

4.Conocimientos básicos como mínimo. O subcontrate el proceso a alguien que sí tenga esos conocimientos. Mucha gente comete el error de invertir sin saber mucho sobre el tema.

5. Nadie puede predecir el futuro - Por supuesto, muchas personas pueden acertar una predicción. Algunos incluso pueden acertar muchas. Muchos tienen una excelente racha prediciendo cosas. Sin embargo, a lo largo de un periodo de 40-50 años, es muy improbable batir al mercado haciendo movimientos basados en escuchar a los tertulianos de los medios de comunicación. Innumerables estudios académicos han demostrado que no se puede batir al mercado escuchando a CNBC, Bloomberg y muchos otros medios de comunicación. Al menos a largo plazo.

6. Control emocional - Este es el punto más infravalorado. La mayoría de la gente piensa que los inversores que apuestan son los que más saben. Sin embargo, a una persona muy emocional y superconocida no le va bien en la inversión. Cada vez que hay un desplome, entran en pánico y venden. Incluso se ha descubierto que algunos doctores en teoría de carteras se han saltado sus propias reglas a la hora de invertir.

Con respecto al último punto, lo más importante es que nadie sabe cómo reaccionará ante un desplome bursátil hasta que experimenta uno.

A principios de 2020, el mercado de valores no se había desplomado en gran medida desde 2008.

Conozco personalmente a muchas personas que me “prometieron” que nunca venderían por pánico como esos “idiotas” (por usar sus palabras) en 2008.

Entonces llegó 2020, los medios gritaron esta vez es diferente como hacen siempre, y mucha de esa gente entró en pánico.

Otra parte del control emocional consiste en no excitarse demasiado en los buenos momentos ni deprimirse demasiado en los malos.

La mayoría de la gente ve un mercado de valores estancado y piensa que no merece la pena invertir en él.

Pocos querían invertir en el S&P500 en 1982, tras 17 años de estancamiento.

Del mismo modo, pocos querían invertir en ella en 2010 tras una “década perdida” . Sin embargo, tras ambos periodos, las acciones experimentaron largas rachas alcistas entre 1982 y 2000 y entre 2009 y 2020.

Del mismo modo, no hay que desanimarse por el hecho de que algunos mercados, como el FTSE All Stars, hayan tenido un rendimiento inferior al de los mercados estadounidenses en los últimos tiempos.

Para más información, haga clic a continuación:

¡¡¡¡Este es uno de los consejos más claros que hay - un regalo del cielo para los expatriados confundidos como yo, así que muchas gracias!!!! ¿Puede recomendar algún proveedor específico de las cuentas de inversión en plusvalías “portátiles” de terceros países, 0%, para expatriados de las que habla más arriba en este artículo? Como es difícil de descubrir en línea si utiliza las palabras equivocadas para buscar para ellos, que creo que estoy haciendo.

Hola Kristen, gracias por tu mensaje. Le enviaré un correo electrónico.

Una de las cosas clave es si quieres invertir por tu cuenta o recurrir a un asesor. Swissquote y Saxo Bank están bien para invertir por cuenta propia.

Excelente post. Acabo de enviarle un correo electrónico acerca de la inversión

Gracias David, te enviaré un correo electrónico.

British National estado trabajando en el extranjero desde 2005, todavía tienen cuenta bancaria en el Reino Unido para transferir dinero a pagar las facturas como usted ha mencionado. Necesito algún consejo sobre cómo aumentar la pensión y dónde y ¿vale la pena volver a pagar sellos NI?

Hola Louise, gracias. Te enviaré un correo electrónico.

los comentarios negativos sobre Saxo bank en Trust pilot son realmente desalentadores.