Q2 2026 investment outlook is defined by a fragile balance between rising energy-driven risks and markets that remain unusually calm.

Navigating this environment means understanding how oil shocks, expensive equities, and structural imbalances are shaping where opportunities and dangers lie.

This global outlook for Q2 draws in part from insights shared during a recent Saxo Bank webinar, where Chief Economist Eric Norland outlined the scale and implications of the current energy shock.

Questo articolo tratta di:

- What energy challenge is the world facing now?

- Who benefits from higher oil prices?

- How does supply shock affect inflation?

- How do commodities behave differently from equities or bonds?

- What to watch out for when investing?

Punti di forza:

- Markets are underpricing the duration and impact of the energy shock.

- Equities remain expensive and vulnerable to negative surprises.

- Bonds are losing their traditional role as a safe haven.

- Commodities and real assets stand out in an inflationary environment.

I miei recapiti sono hello@adamfayed.com e WhatsApp +44-7393-450-837 se avete domande.

Le informazioni contenute in questo articolo hanno un valore puramente indicativo. Non costituiscono consulenza finanziaria, legale o fiscale e non rappresentano una raccomandazione o una sollecitazione a investire. Alcuni fatti potrebbero essere cambiati dal momento della stesura.

Why do markets remain calm despite rising global risks?

At first glance, global markets in Q2 2026 appear remarkably stable. Equity indices are holding near highs, volatility remains subdued, and investor sentiment hasn’t fully reflected the growing list of macro risks.

But beneath the surface, the picture is far more fragile.

Oil prices have surged from earlier lows, inflation is re-accelerating, and geopolitical tensions continue to disrupt global trade routes.

Yet markets seem to be pricing in a smooth resolution—an assumption that may prove overly optimistic.

This disconnect between market calm and macro risk is the defining feature of today’s investment environment.

The Dominant Macro Driver: What caused the global energy crisis?

The global energy crisis in 2026 is primarily caused by a geopolitically driven oil supply shock, amplified by years of underinvestment and fragile global supply chains.

At the center of it is war-related disruption, which has removed an estimated 10–12% of global oil supply.

According to Eric Norland, Chief Economist and Executive Director of CME Group, this represents a historically large shock that rivals or even exceeds events like the 1973 Oil Crisis.

Beyond actual supply losses, uncertainty around the duration and escalation of conflict has added a significant risk premium to prices.

At the same time, global trade routes have become less reliable. Security risks in key chokepoints such as the Red Sea and the Strait of Hormuz have reduced shipping volumes, increased transit times, and driven up costs.

These disruptions ripple across the entire energy supply chain.

Compounding the issue is years of underinvestment in oil and gas production. Capital constraints and the shift toward energy transition policies left the market with limited spare capacity.

As a result, the system is now far more sensitive to disruptions than in previous cycles.

Meanwhile, demand has remained relatively resilient. Global consumption has not fallen enough to offset supply losses, particularly with steady demand from emerging markets.

This combination has driven sharp price movements with oil rising from around $68 per barrel before the conflict, peaking near $120, and now stabilizing around $90.

But the key issue isn’t just where prices are today; it’s what the market expects next.

Current pricing suggests investors believe disruptions will ease within months.

However, history shows that energy shocks often last longer than expected, especially when driven by geopolitical and structural factors.

For now, the impact has been partially cushioned by:

- High global inventories

- Strategic petroleum reserve releases

These buffers, however, are temporary. If the crisis persists, supply tightness could intensify quickly, raising the risk of sharper price spikes and broader consequences for inflazione and financial markets.

Why is crude oil important to the global economy?

Crude oil is important to the global economy because it powers the movement, production, and energy systems that keep modern economies running.

It directly influences:

- Transportation and logistics

- Manufacturing and industrial production

- Energy generation in many regions

Because of this, oil prices act as a multiplier across the economy.

When oil rises, costs increase across supply chains, feeding into higher prices for goods and services worldwide.

In short, oil is not just another commodity, but a core driver of economic stability and growth.

What are the economic impacts of the oil industry?

The economic impact of the oil industry is a global redistribution of wealth, shifting income from energy consumers to producers while exposing vulnerable economies to severe disruption.

In the same Saxo Bank webinar, Eric Norland categorized these effects into three groups:

Beneficiari

Oil-producing nations and energy companies are seeing a surge in revenues, estimated at around $2.7 billion per day globally.

Major producers like the United States and Russia are among the primary beneficiaries.

This represents a large-scale wealth transfer from consumers to producers, strengthening fiscal positions and boosting energy-sector profits.

Inconvenienced

Oil-importing nations, particularly in Asia and Europe, are facing higher costs.

Countries like China, Japan, and South Korea are paying more for energy, though large reserves and policy measures have softened the immediate impact.

These economies are not in crisis, but they face slower growth and rising inflation pressures.

Devastated

Some economies face a more severe challenge: limited ability to export due to geopolitical constraints or disrupted infrastructure.

Even certain oil-rich nations are affected if they cannot fully bring supply to market, forcing them to rely on sovereign wealth funds or liquidate assets to offset revenue losses.

What are the consequences of the Strait of Hormuz being closed?

The consequence of the Strait of Hormuz being closed is an immediate and severe disruption to global oil supply, leading to sharp price spikes and heightened market volatility.

The Strait of Hormuz is one of the most critical oil chokepoints in the world. A significant portion of global oil supply flows through this narrow passage.

With the Strait now disrupted:

- Global oil supply is materially constrained

- Oil prices are repricing aggressively

- Shipping costs and insurance premiums are surging

- Energy-importing economies are facing immediate cost pressure

Unlike disruptions in the Suez Canal where alternative routes exist, a blockage in Hormuz offers no easy workaround in the short term.

This turns the situation into a systemic supply shock. In market terms, the impact unfolds in layers:

- Energy markets react first, typically with sharp upward price movements

- Inflation expectations adjust quickly, feeding into bond yields and monetary policy expectations

- Equities reprice, particularly in energy-sensitive and import-dependent sectors

- Currencies shift, with commodity exporters strengthening and importers weakening

Volatility does not just spike but tend to remain elevated, as markets continuously reprice based on geopolitical developments and the uncertain timeline for resolution.

For investors, this is not merely a tail risk scenario but a live macro driver, forcing rapid reassessment of portfolio exposure across asset classes.

How does oil affect inflation?

Oil affects inflation by directly increasing energy costs, which then feed through transportation, production, and ultimately consumer prices across the economy.

As energy costs rise:

- Transportation becomes more expensive

- Production costs increase

- Consumer prices follow

Recent data already shows inflation moving higher, driven in part by rising gasoline and diesel prices.

This sets the tone for a broader inflation trajectory across 2026, where energy-driven price pressures remain a key variable shaping the global macro outlook for the remainder of the year.

In more extreme scenarios such as a major supply shock or a disruption in key routes like the Strait of Hormuz, this inflationary pressure intensifies sharply.

How energy shocks are feeding inflation and policy uncertainty

Oil price spikes in these cases don’t just affect headline inflation; they can quickly shift inflation expectations, leading to broader repricing across markets.

This creates a difficult environment for central banks:

- Tightening policy risks slowing growth

- Easing policy risks fueling further inflation

The result is a policy dilemma that adds uncertainty to financial markets, particularly in interest rate expectations, bond yields, and currency stability.

Asset Class Outlook: Where Things Stand in Q2 2026

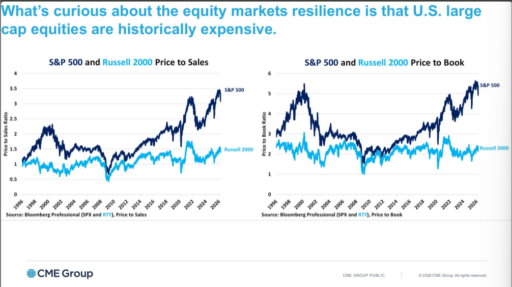

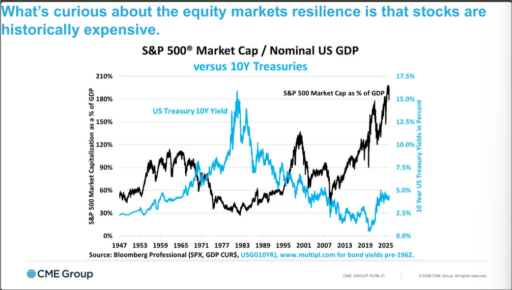

Azioni – Expensive and Complacent

The S&P 500 and other major indices remain near historically elevated valuations, with market capitalization relative to GDP reaching extreme levels.

Despite rising risks:

- Volatility remains low

- Investors continue to buy the dip

This suggests a market that is complacent, pricing in continued stability despite growing macro pressures.

Obbligazioni – Losing Their Appeal

Traditionally seen as a safe haven, bonds are becoming less attractive:

- Rising yields are driving price declines

- Inflation is eroding real returns

- Fiscal deficits are increasing supply

In some regions, bond markets are already showing signs of stress, raising concerns about their role in diversified portfolios.

Materie prime – A Clear Beneficiary

Commodities, particularly energy and precious metals, are among the strongest performers in the current environment.

Drivers include:

- Inflation hedging

- Geopolitical uncertainty

- Portfolio diversification

Metalli preziosi, in particular, have benefited from investor demand during periods of macro instability, although they remain sensitive to changes in interest rate expectations.

Currencies – A New Layer of Volatility

Currency markets are increasingly influenced by:

- Diverging fiscal policies

- Commodity price exposure

- Interest rate expectations

Commodity-linked currencies tend to outperform during energy rallies, while import-dependent economies may see their currencies weaken.

This adds another layer of complexity for global investors.

What is a good investment strategy in 2026?

A strong investment approach in 2026 is positioning for resilience through real assets and selective equity exposure across key sectors such as energy, commodities, defense, financials, and high-quality technology.

This reflects a reduced reliance on traditional bonds, as energy shocks and inflation risks keep markets structurally unstable in Q2 2026.

In an environment defined by uncertainty, no single asset class stands out as universally safe.

Instead, investors should focus on positioning for multiple scenarios.

Key themes to consider:

- Real assets exposure: Energy and commodities may continue to benefit from supply constraints and inflationary pressures, making them key hedges in an energy-driven inflation environment

- Selective equity investing: Focus on sectors with pricing power, strong balance sheets, and structural tailwinds rather than cyclical exposure; this includes energy, materials, defense, and selective technology leaders benefiting from AI-driven productivity gains

- Financials (selective exposure): Certain banks and insurers may benefit from higher interest rates, but performance will depend heavily on sovereign exposure and credit quality in a fragmented global debt environment

- Reduced reliance on bonds: Reassess their role as a defensive asset amid fiscal stress, persistent deficits, and rising global yields that limit upside and increase volatility in sovereign debt markets

- Risk management: Prepare for potential volatility spikes driven by geopolitics, inflation surprises, and policy uncertainty, particularly as energy shocks transmit quickly across asset classes

Rather than chasing returns, the priority in Q2 2026 is resilience; building a portfolio that can withstand both inflationary pressure and geopolitical shocks.

Structural Shifts Investors Should Watch in 2026

The key structural shifts investors should watch are rising fiscal imbalances, constrained monetary policy, and accelerating geopolitical realignment, all of which are reshaping global markets beyond short-term cycles.

Fiscal Imbalances Everywhere

Governments around the world are running large budget deficits, even in periods of economic stability.

This raises concerns about:

- Debt sustainability

- Increased bond issuance

- Long-term currency stability

These imbalances increase reliance on debt markets at a time when investor appetite for sovereign debt is becoming more selective, especially as yields rise globally.

Policy Constraints

Central banks face limited flexibility:

- Inflation remains above target

- Growth risks are rising

Recent rate cuts despite elevated inflation suggest that policymakers are increasingly constrained in their ability to respond to shocks.

This creates a more fragile policy environment where central banks are often reacting to conditions rather than actively shaping them, increasing volatility in interest rate expectations.

Geopolitical Realignment

Global economic relationships are shifting:

- Rising tensions between major powers

- Supply chain restructuring

- Increased state involvement in strategic industries

These changes are gradually redrawing the map of global trade and capital flows, with implications for everything from commodity pricing to equity market leadership and currency performance.

Over time, this may lead to a more fragmented and less globally synchronized investment environment.

Conclusione

Q2 2026 is less about isolated market moves and more about a growing disconnect between visible market stability and underlying macro fragility.

Energy shocks, fiscal pressure, and geopolitical fragmentation are not new individually, but their overlap is creating a more complex and less predictable investment environment.

What stands out is not just volatility in prices, but volatility in assumptions.

Markets are still largely positioned for a return to normalization, while structural forces such as energy security concerns, persistent deficits, and shifting global alliances, point toward a more uneven path ahead.

For investors, the key challenge is not forecasting a single outcome, but recognizing that traditional relationships between growth, inflation, and asset performance are becoming less reliable.

In this kind of environment, positioning matters more than prediction, and resilience matters more than precision.

Domande frequenti

What is the oil industry outlook for 2026?

The oil industry outlook for 2026 remains highly sensitive to geopolitical risks and supply constraints, with prices likely to stay volatile as disruptions and underinvestment continue to shape global supply dynamics.

Is the oil shock worse than the 1970s?

In terms of percentage of global supply impacted, the current shock is comparable to or in some cases larger than parts of the 1970s crises, but its economic impact is partially cushioned by higher inventories and diversified energy systems.

Are bonds still a good investment in 2026?

Obbligazioni can still play a role in portfolios in 2026, especially for income and diversification, but they are no longer a universally safe asset due to higher yields, inflation risk, and increased government debt issuance.

Their effectiveness now depends more on duration, credit quality, and the inflation environment rather than broad market exposure.

What sectors benefit from high oil prices?

Energy producers, select commodities, and commodity-linked currencies tend to benefit most from higher oil prices, along with certain defense and infrastructure-related industries during geopolitical stress periods.

Is it a good time to invest in equity now?

Equities are still investable, but returns are increasingly concentrated in specific sectors, meaning a selective approach is more appropriate than broad index exposure in the current environment.

Siete afflitti dall'indecisione finanziaria?

Adam è un autore riconosciuto a livello internazionale in materia finanziaria con oltre 830 milioni di visualizzazioni di risposte su Quora, un libro molto venduto su Amazon e un contributo su Forbes.