Switzerland’s annual wealth tax is levied on net assets, but effective rates vary from canton to canton, from less than 0.1% to around 3% for wealthy residents.

Because the system is cantonal and municipal, choosing where to live is an essential part of minimizing exposure to wealth tax in Switzerland.

Questo articolo tratta di:

- How does Switzerland tax the wealthy?

- Which Swiss canton has the lowest wealth tax rate?

- Which Swiss canton has the highest taxes?

- Is there a wealth tax exemption in Switzerland?

Punti di forza:

- Swiss wealth tax is levied at the cantonal and municipal level, not federally.

- Rates range from 0.05% to 3%, based on location and wealth level.

- Cantons like Zug, Nidwalden, and Schwyz offer the lowest tax rates.

- Non-residents are generally taxed only on Swiss-sourced assets, not worldwide wealth.

I miei recapiti sono hello@adamfayed.com e WhatsApp +44-7393-450-837 se avete domande.

Le informazioni contenute in questo articolo non costituiscono una consulenza fiscale e possono essere cambiate rispetto al momento in cui sono state scritte. Posso mettervi in contatto con un'assistenza fiscale esperta per la vostra situazione specifica.

How does wealth tax work in Switzerland?

Svizzera wealth tax is a yearly tax on your total net worth, charged by your canton and municipality rather than the federal government.

Taxable net wealth generally includes:

- Cash and bank deposits

- Securities (stocks, bonds, ETFs)

- Portafogli di investimento

- Immobili (domestic and, in some cases, foreign for rate progression)

- Business ownership stakes

- Certain luxury assets

Liabilities are deductible, including:

- Mutui

- Personal loans

- Business debts

The tax is calculated on net wealth (assets minus liabilities) as of December 31 each year.

How is wealth tax calculated?

Each canton sets:

- Tax-free thresholds

- Progressive wealth tax rates

- Municipal multipliers

Rates range between 0.05% and 3.0%, based on wealth level and location.

Unlike countries that tax worldwide income heavily, Switzerland focuses more on modest recurring wealth taxation combined with moderate income tax at the federal level.

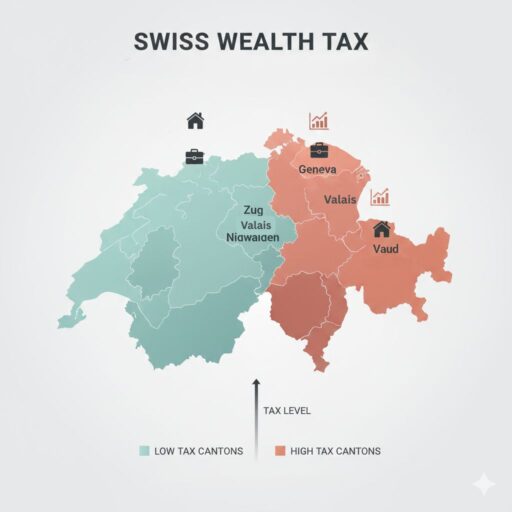

What are Swiss Wealth Tax Rates by Canton?

Since wealth tax in Switzerland is levied at the cantonal and municipal level, rates vary significantly based on where you live. The minimum rate is roughly 0.05%.

Below is an overview of typical effective wealth tax rates across selected cantons:

| Canton | Indicative Wealth Tax Rate (2025) | Typical Tax‑Free Threshold | Notes |

| Zug | ~0.05% – 0.20% | ≈ CHF 100,000 (individual) / CHF 200,000 (couple) | Among the clearest low‑tax cantons; progressive but capped at lower effective rates. |

| Schwyz | 0.06% | ≈ CHF 125,000 (individual) / CHF 250,000 (couple) | Low, often linear rates across brackets; competitive overall. |

| Nidwalden | ~0.10%–0.13% | ~CHF 60,000 (individual) / CHF 120,000 (couple) | Relatively low tax with moderate exemptions; competitive for wealthy residents. |

| Lucerne | ~0.24% | ~CHF 50,000 (individual) / CHF 100,000 (couple) | Mid‑range wealth tax, progressive on net assets; varies by municipality. |

| Vaud | ~0.779 – 3.39 % | ~CHF 58,000 (single) / CHF 116,000 (couple) | Progressive scale with higher marginal rates at larger net worth. |

| Geneva | ~0.1 – 1 % | ~CHF 82,200 (single) / CHF 164,400 (couple) | One of the highest wealth tax burdens; municipal factors also apply. |

| Zurich | ~0.05 – 0.3 % | ~CHF 77,000 (single) / CHF 154,000 (couple) | Progressive and moderate, but higher than Zug at upper brackets. |

| Valais | Up to 3% | CHF 30,000 (single) / CHF 60,000 (couple) | Progressive rates; relatively low thresholds but higher rates for larger net wealth; moderate overall burden compared with Geneva or Vaud. |

| Neuchâtel | ~0.30 % – 0.50 % | ~CHF 50,000 | Progressive base rates with higher effective tax burden; one of the higher wealth tax cantons. |

Rates are indicative and can vary based on municipal multipliers, total net wealth, marital status, and allowances.

Which Swiss canton has the lowest wealth tax?

The cantons with the lowest wealth tax in Switzerland are Zug, Schwyz, and Nidwalden.

Among them, Zug is the most tax-friendly due to its combination of low wealth and income tax rates.

The canton also offers a business-friendly environment and a strong international community, making it attractive for both entrepreneurs and high-net-worth individuals.

For those relocating from higher-tax cantons, moving to Zug can lead to significant annual savings on wealth taxes.

Which canton in Switzerland has the highest taxes?

The cantons with the highest wealth and income taxes in Switzerland are Geneva, Vaud, and Valais.

These regions generally impose higher wealth tax rates and have larger public spending programs compared with other cantons.

Geneva, in particular, carries one of the highest combined burdens for both wealth and income taxes.

For high-net-worth individuals, living in these cantons can result in significantly higher annual tax liabilities than in low-tax cantons like Zug or Schwyz.

How To Avoid Swiss Wealth Tax

Completely avoiding tax on wealth in Switzerland is difficult for residents, but relocating to a low-tax canton such as Zug can significantly reduce liability.

Legal strategies to reduce exposure include:

1. Choosing a low-tax canton: Relocating to cantons like Zug or Schwyz can materially reduce annual wealth tax.

2. Structuring assets efficiently: Increasing deductible liabilities, using pension structures (Pillar 2 and 3a), or holding certain assets through business entities can lower taxable wealth.

We offer bespoke structuring solutions that can be tailored based on your situation.

3. Lump-sum taxation (for eligible foreigners): Some qualifying foreign nationals may opt for forfait taxation, where tax is based on lifestyle expenditure rather than global wealth. This option is not available to Swiss citizens.

4. Ceasing Swiss tax residency: Becoming non-resident may eliminate Swiss wealth tax on foreign assets, though Swiss real estate remains taxable.

Professional tax advice is essential before implementing any of these strategies.

Is there a wealth tax exemption in Switzerland?

There is no blanket federal Swiss wealth tax exemption, but each canton offers tax-free thresholds and allowances that range from around CHF 50,000 for single individuals in low-tax cantons to over CHF 160,000 for married couples with children in higher-threshold cantons.

- Personal allowances vary widely, with higher exemptions for married couples and additional allowances for children.

- Small and moderate levels of wealth may fall below these taxable thresholds in many cantons.

- Pension assets such as occupational pensions (pillar 2) and tied conti pensionistici (pillar 3a) are typically exempt from wealth tax.

- Certain business assets may receive preferential valuation under cantonal rules, though most are included in net wealth calculations.

These exemptions and allowances make the tax system progressive and ensure that only significant net wealth is subject to taxation, while the exact thresholds and rules depend on the canton of residence.

What is the Swiss wealth tax proposal?

Switzerland recently faced a high‑profile proposal to introduce a new federal tax on extremely large fortunes, but it was overwhelmingly rejected by voters in late 2025, as per Deloitte.

The initiative would have reportedly imposed a 50% tax on inheritances and gifts exceeding CHF 50 million (targeting only the ultra‑wealthy) in order to fund public goals like climate initiatives.

Because Switzerland’s political system relies on direct democracy and strong cantonal autonomy, major federal tax reforms face steep hurdles and require national referendums to pass.

Proponents of measures like this have argued for higher taxes on the top 1% and adjustments to valuation rules for very large fortunes, but these ideas have not gained traction at the national level.

How much does the Swiss wealth tax raise?

In 2017, Swiss wealth tax raised 7.329 billion Swiss francs, accounting for about 3.8% of total tax revenue across federal, cantonal, and municipal authorities.

More recent data from the Swiss federal tax authority shows that taxable wealth continues to grow, with analyses suggesting that wealth tax now accounts for approximately 5.6 % of total tax revenue in Switzerland.

In cantons with higher concentrations of wealthy residents, wealth tax contributes a proportionally larger share of local revenues, while its impact is smaller in low-tax cantons.

Despite moderate statutory rates, the tax provides a stable and predictable source of revenue due to the high number of wealthy taxpayers relative to the population.

Do non-residents pay tax in Switzerland?

Non-residents are generally not subject to Swiss wealth tax on assets outside Switzerland.

They are only taxed on Swiss-sourced assets, including real estate, permanent establishments, and business operations located in Switzerland.

Owning property in Switzerland usually triggers local tax obligations, such as cantonal wealth tax on the property and property taxes, and may also involve income tax on rental income.

Some cantons apply limited municipal multipliers or reporting requirements even for non-resident property owners, depending on local regulations.

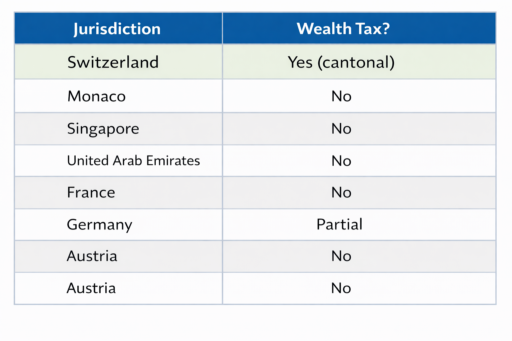

Switzerland vs Other Wealth-Friendly Jurisdictions

Switzerland’s wealth tax system sits between low-tax havens and higher-tax European neighbors.

While cantonal rates range from less than 0.1% to over 3%, countries like Monaco, Singapore, and the UAE impose no wealth tax per year, offering full exemptions on net assets.

These jurisdictions are attractive for high-net-worth residents but often have stricter residency requirements or different business and lifestyle considerations.

Compared with Europe, Switzerland remains competitive.

France maintains real-estate-focused wealth taxation, Germany abolished its national wealth tax but has high income and inheritance taxes, and Austria also has no wealth tax but relatively high income taxes.

Switzerland’s cantonal system allows residents to optimize their tax exposure through location choice while benefiting from political stability, transparent governance, and robust financial infrastructure.

Ultimately, Switzerland strikes a balance: it is not a zero-tax haven, but its predictable, moderate wealth tax combined with favorable income and estate treatment makes it one of the most attractive jurisdictions in Europe for HNWIs.

Conclusione

Switzerland’s wealth tax reflects the country’s balance between fiscal prudence and attractiveness for high-net-worth individuals.

While rates are moderate compared with other European jurisdictions, the wide variation across cantons creates meaningful incentives for residency planning and strategic asset structuring.

The system’s reliance on cantonal autonomy, combined with political mechanisms like direct democracy, makes significant federal reforms unlikely, preserving predictability for taxpayers.

Ultimately, Switzerland demonstrates how a targeted, well-administered wealth tax can generate stable revenue without deterring investment or capital inflows, highlighting the nuanced trade-offs between equity, efficiency, and competitiveness in wealth taxation.

Domande frequenti

How much is $100,000 after tax in Switzerland?

A $100,000 annual income in Switzerland leaves between $65,000 and $80,000 after taxes, reflecting an effective tax rate of roughly 20% to 35%.

The exact outcome varies by canton, marital status, number of children, church tax liability, and overall income structure.

Are Swiss taxes high?

Swiss taxes are generally moderate by international standards, lower than countries like France or Germany but higher than low-tax jurisdictions such as Singapore or the UAE.

While Switzerland does impose a wealth tax, income tax rates in many cantons particularly low-tax ones like Zug, remain competitive rather than aggressively high.

What country has the lowest taxes for the wealthy?

Countries like the United Arab Emirates, Monaco, and Singapore have some of the lowest tax burdens for wealthy individuals due to the absence of annual net wealth taxes and generally favorable income tax regimes.

However, each jurisdiction has specific residency rules, economic substance requirements, and lifestyle considerations that affect overall tax outcomes.

Why is Switzerland considered a tax haven?

Switzerland is considered a tax haven because it combines relatively low and flexible cantonal tax regimes with a historically strong tradition of banking secrecy, political stability, and a sophisticated financial system.

Although it no longer offers the same level of secrecy and now complies with global transparency standards, its competitive tax structure and legal certainty continue to make it attractive for international wealth and corporate structuring.

Siete afflitti dall'indecisione finanziaria?

Adam è un autore riconosciuto a livello internazionale in materia finanziaria con oltre 830 milioni di visualizzazioni di risposte su Quora, un libro molto venduto su Amazon e un contributo su Forbes.