Updated January 10 2020.

This is to answer frequently asked questions about index account.

Want to gain access to low-cost and diversified funds from some of the world’s leading financial institutions, but still want the personal touch of speaking to your advisor regularly by phone or WhatsApp? Or perhaps you are just fed up with some of the expensive products offered by your bank, or other traditional companies.

In any case, I have helped countless investors gain access to such portfolios, and achieve better returns, all around the world.

Se state cercando di investire come espatriati o individui con un alto patrimonio netto, che è ciò in cui sono specializzato, potete inviarmi un'e-mail (advice@adamfayed.com) o un messaggio WhatsApp (+44-7393-450-837).

Questo vale anche per chi è alla ricerca di un secondo parere o di investimenti alternativi.

Alcuni fatti potrebbero cambiare rispetto al momento della stesura del presente documento e nulla di quanto qui scritto rappresenta una consulenza finanziaria, legale, fiscale o di qualsiasi tipo, né una sollecitazione a investire.

Index Account FAQs

Q. What kind of returns can I expect?

Historically markets like the US S&P give 10% per year, but that is merely an average. Some years, and decades, are much better than others, and nobody can predict or time marekts

As you need some bonds in your portfolio, 7%-8% long-term returns are realistic. Overall returns will also depend on how much you invest, and for how long.

If you invest $50,000 for 5 years and get 8% per year, you will only have $73,466 after the 5 years are up. If, on the other hand, you invest for 30 years, and add a $1,000 per month contribution, you will have $1.5M, even if you only get the 7% per annum returns.

Q. How do the accounts work?

You are set up with investments that are in line with your age. As a simple example, a 25 or 30 year old, should be invested less in bonds and more in markets. A 55 year old, or anybody 5 years away from retirement, should have more bonds in their portfolio, compared to the younger person.

Q. What currency can I invest in?

USD, British Pounds, Euros, Australian Dollars, Norwegian Krone, Swedish Krona and various other options. Money can be taken from almost any bank account in the world, and deposited into a USD account.

Q. What are the account minimums?

Analysis paralysis, and not taking action, are the biggest mistakes I see. Ultimately, if you spend 100% of what you make, you will make $0 in investment returns. If you inv$500 for monthly accounts and $40,000 for lump sums, or currency equivalent. My lump sum minimums will be increasing to $50,000 from next month (May 2019).

Q. What are the biggest mistakes I see investors make?

Analysis paralysis, and not taking action, are the biggest mistakes I see. Ultimately, if you spend 100% of what you make, you will make $0 in investment returns.

If you invest $2,000 a month and get 5%, you will be richer than if you invest $500 a month and make 8%.

Various studies have shown that how much you contribute, is the biggest indicator of how much your wealth will be in retirement, alongside spending habits. Your income and investment returns are secondary factors.

Despite this, most people are overly cautious and want to start small. The opposite end of the spectrum – taking too many risks and speculation – is another key mistake I see. Market timing and speculating are huge risks, that seldom pay off, compared to buying and holding for 40 years.

So a realistic understanding of risk and return is one of the keys to investment success, alongside a disciplned approach.

Q. Can’t I just invest myself?

Yes you can, but how many people, including doctors, do you know who have six packs and are ultra-healthy? The point being, often people need some structured help, for example a personal trainer, to see sustainable goals, and to stop them doing silly things.

Likewise, in finance, somebody who invested $10,000 in the S&P in 1941, would have $52 million today. How many of our parents and grandparents did that? Most people panic when markets are going down, and get too excited when markets are going up – buy high and sell low.

Q. What are the minimum investment terms?

I would highly recommend that anybody who invests should consider a medium-lump term investment. Markets perform well, but in the short-term, nobody can predict what will happen.

Therfore, anybody investing should consider this a 5 year + commitment, and understand that the longer you invest, the more you will gain.

Q. What do I charge?

1% on smaller portfolios, reducing to 0.5% for portfolios above $500,000.

Q. How do you pay?

Bank transfer or credit/debit card. For lump sums, usually bank transfer are used. Card payments are used by most monthly investors.

Q. Do you gain online access?

Yes you gain 24/7 online access.

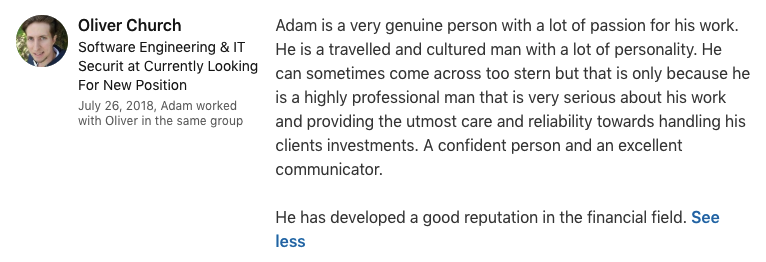

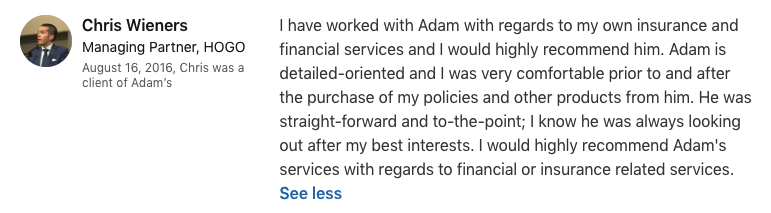

Q. Do I have any client recommendations?

Yes countless. Below are a small selection taken from my LinkedIn :

Many more can be found on my profile. One of my clients, Nikolaos, has also produced a recommendation on Youtube.

Q. How do I stay in touch with clients?

By email, WhatsApp and various apps. I communicate with some clients weekly, others monthly and some quarterly, depending on a range of factors, such as how busy we both are.

However, I do respond to emails and WhatsApp messages within 24 hours.

Q. What kind of fund managers do I use within the platform?

Various fund companies. Again, many people over analyze this question. The difference between an index fund used by Vanguard, and one used by BlackRock or iShares, is tiny. The costs are the same.

Q. How do I keep costs low?

By focusing on technology. The traditional financial services industry has $30,000 a month offices and does everything face-to-face. This increases the cost for clients, and lowers returns.

It is also a very poor use of my time, and yours, and doesn’t help increase returns.

Q. What is you money invested into?

Low-cost ETF and index funds, focusing on markets in the US, Europe and emerging markets, with some in bonds.

Q. How much should you be saving and investing?

That depends on your age. If you are very young, 5%-10% of your salary may be fine. Most people leave it too late, however, and need to be very aggressive with their saving targets.

In general, it is better to save and invest aggressively when you are young, and when you have the chance to invest.

You never know when you will need the money.

Q. What is the process like for opening up accounts?

The first stage is an initial talk to understand your objectives better. If we are on the same page, the next step is documentation; proof of identity (passport) and address for anti-money laundering requirements.

Finally, once that is done, the accounts will be reviewed for 24-72 hours. Assuming they are approved by admin/legal, the premium needs to be paid.

Q. What investment options do you have for American expats?

The regular contributions aren’t available for Americans, but the lump sums are.

Q. Can I accept anybody who meets the account minimums?

Everybody apart from people living in America. American expats are fine. Most locals are fine as well. In fact, I do have a significant number of local ‘returnees’ as clients, who have returned home after living in the UK, US, Canada or Australia.

Q. Where are the assets held?

It depends on the platform, but typically in well-regulated UK, US and offshore territory, with various guarantees if there is a financial crisis.

Q. Will you need to pay tax?

Tax is usually on capital gains tax, and that is paid once you sell and make a gain. That is another reason to be long-term; it is more tax advantageous. Generally speaking, the offshore destinations are best for tax, especially for expats, but all the solutions are tax advantageous.

Q. You may be moving, does that affect things?

This is a question that many expats ask me, as they regularly move every 3-4 years. The simple answer is no, it doesn’t affect things.

Provided you update your payments information like credit or debit card, your investments won’t be affected if you move.

Q. Can expats invest in Vanguard and other index funds?

Often not directly, but the platforms I have access to, allow for such options to be held.

Q. Where do my clients live?

All around the world, from the UK, Shanghai, Brussels, Qatar, Holland, Japan, South Africa, Singapore, Hong Kong, Australia, Canada, to Dubai. More than 100 countries in total.

Q. Is this the right time to buy index funds? You are worried about a recession and/or a financial crisis.

Nobody can predict when a financial crisis will strike. Barely nobody thought 2008-2009 would happen, and those few that did predict it, were surprised at how quickly GDP and sock markets recovered. There is a lot of academic evidence that market timing doesn’t work, so we do know that it is counterproductive to worry about these things.

As for recessions, there is little or no correlation between GDP growth and stock market performance. Just look at the last 10-20 years. Chinese Markets have performed awfully since 2006, despite very strong GDP growth.

US Stock Markets have performed excellently since 2009 lows, with the exception of last year, when markets fell despite strong GDP growth! This year markets have performed strongly again, despite weaker GDP numbers.

Beyond that, there is little or no correlation between GDP growth and geopolitical risks in general. Markets have risen during nuclear stand offs (North Korea, Cuba), trade dispute and hot wars. They have fallen during periods of geopolitical calm.

Even in recent times in the last 12 months, the best months for the markets have been during periods of uncertainty, such as the recent big rises during the US Government Shutdown a few months ago and the North Korea situation last year.

That doesn’t mean that markets always rise during such periods, only that no correlation exists between investment returns and political problems. The only `strongish` correlation is between various price-to-earnings (PE) ratios and market falls.

For example, in 1999, the US Dow Jones looked overvalued, relative to bonds and international markets, on a PE basis. The investor who has a well diversified portfolio doesn’t need to worry abut such considerations. Rebalancing away from the winners to the losers, has always worked historically.

Q. Why is it so hard to beat the market?

The costs of trying to beat the market is one of the biggest reasons. If you are buying and selling frequently, you are increasing costs. This means your net returns need to be huge, even to break even with the market.

For example, if the markets produce 6% for the next 2 years, and your costs for buying and selling and market timing are 3%, you will need to beat the market by 50%, an extremely tall order

Beyond that nobody can know, for sure, when markets will fall and rise. People who beat the market over 5-10 years often get cocky and complacent.

People also allow their emotions to guide their investing decisions. Various studies have shown that doctors may be more likely to buy healthcares stocks, and teachers education companies and ‘everybody’ has a bias towards their home country.

This is called ‘familiarity bias’ in investing. Investors are less likely to be objective, and more likely to be emotional, about things close to their heart.

Besides, all of the information about listed firms is publicly available. I don’t need to be a doctor to check the balance sheets of pharmaceutical stocks!

There are thousands of investors, and indeed robots, in the market these days. If there is such a great undervalued opportunity in the market then why isn’t everybody buying that stock? You don’t have special information…..if you do, that is insider trading and illegal.

They are just some of the reasons why only 20% of people beat the market over 5 years, and 2% over 50 years.

Q. Is it true that even Warren Buffett isn’t beating the S&P500 anymore?

Yes it is true. In the 1960s and 1970s, he beat the market handsomely. In the 1980s, he did it comfortably. The gap closed in the 1990s, and 2000s. The last 10 years, he hasn’t beaten the market.

The biggest reason for this, is the rise of institutional investors like banks and hedge funds. In the 1960s and 1970s, most of the market was dominated by small investors. Regular people.

These days, most of the money is controlled by banks, financial advisors and hedge funds……..PHDs, robots and other people who have done their research.

So it is becoming harder and harder to use research to beat the market, because these institutions are also researching undervalued companies.

Q. Is it easier to beat the market in emerging markets and small caps?

Slightly easier, because there are less institutional investors in such markets, but it is still hard to beat the US S&P. A good example would be the Chinese Stock Market. I have seen more investors beat the index with stock picking, than any other market.

And yet the market has been one of the worst performing in the world, falling from 6,000 in 2008 to 3,000+ now. In comparison, the US Market has doubled. So even if you beat the benchmark (in this case the Chinese Stock Market), that doesn’t mean that you have succeeded as an investor.

If somebody really can’t help themselves, stock picking with just 5%-10% of your portfolio makes sense. After 20 years, you may just realize it was too much hassle, compared to indexing and using an advisor!

Q. Is there no place for active management?

Bonds are one of the few areas where active can beat passive. Bonds don’t pay 6% anymore – often they only pay 1%-2%. Besides, a good bond fund should include some high quality corporate bonds, as they pay more.

However, most of the index bond funds used are purely government bonds, which barely pay anything. So some good quality actively managed bond funds can easily pay 3%-4% per year net, by including some corporate bonds.

Q. Why should you even have bonds in your portfolio, if they pay so little?

Bonds usually rise when markets fall. This buffer allows you to rebalance in the bad times. Let’s take a simple example of somebody who had $200,000 before the financial crisis.

$40,000 is invested in bonds and $160,000 in index equity funds. The bonds rise to $44,000 during the panic and the stock index fall to $100,000.

You now have a $144,000 portfolio, and 30% in bonds, as opposed to 20%. Now you can sell 10% of your bonds, and buy the equities at a cheaper price, to maintain the 80%-20% balance. After markets recovered, the rebalancing would have helped returns.

Having said that, a 10%-20% allocation to bonds is fine for most younger people, and even those who are 40, 45 or 50. Above 50, and in retirement, it makes sense to rise the bond component of your portfolio.

Q. Are FANG stocks overvalued?

Quite possibly. They certainly look so on a P/E basis. Today’s winners are usually today’s losers, and technology is one area of the market that looks overvalued now.

Who could have predicted the rise and falls of previous tech giants, such as Yahoo? I am not saying Amazon and Google will go bankrupt, or even fall by 50%, but it is a fact that it would be unprecedented if they continued to beat the market, year in, year out.

None of the original 30 firms on the Dow Jones, are still on it. This survival of the fittest is one of the reasons why markets beat other investments – they are the cream of the crop.

FANG stocks may be the cream today, but don’t count on it continuing!

Q. How about real estate investment trusts (REITS)?

REITS can be a great additional to a portfolio. Various academic studies have shown that REITS lower volatility, and (slightly) increase returns over the long-term.

The reason is that REITS perform well, during periods when stocks markets perform badly, and vice versa. REITS also have several advantages over direct real estate, including;

- They can be sold more easily. With direct real estate, it isn’t always easy to sell, especially in markets where people don’t like ‘second hand homes’ like in China and many Asian markets.

- Long-term performance is better.

- It can be held in the same portfolio as bonds and stock indexes. This means you can buy and rebalance.

- They are globally diversified so not focused on just one real estate market.

- Geopolitical risk is less when you can buy and sell online, quickly. If you buy a physical plot of land, or property, in an emerging markets, there is significant political risk. Indeed most countries in the last 50-100 years have had extreme governments that have confiscated land and private property.

- They can be bought in seconds whereas direct real estate is time consuming.

Just like stock market indexes, however, some of the lower-cost REITS funds are better.

Q. Do index funds exist which lower the downside?

Yes they do. Many companies offer limited guarantees, linked too structured notes. A typical example would be a 3%-4% per year ‘guarantee’ provided markets don’t fall by 40% or more over the duration of the product – say 15 years as an example.

However, these guarantees add costs and complexity to the products. The chances of you being down over a 15-20 year period are very low, in any case.

It has never happened that somebody invested for 20-25 years or longer, in a diversified stock and bond index portfolio, has been down.

Qual è il risultato finale?

I can’t control markets or always pick winners, but I can control risk through the asset mix and help with the behavioural/emotional aspects of investing – stopping my clients from doing silly things that affect most investment portfolios.

Siete afflitti dall'indecisione finanziaria?

Adam è un autore riconosciuto a livello internazionale in materia finanziaria con oltre 830 milioni di visualizzazioni di risposte su Quora, un libro molto venduto su Amazon e un contributo su Forbes.

Hi Adam, I have been reading your content in the last few months, and I am interested in these kinds of accounts. I presume you can accept clients in Mainland China? How about the RMB issue?

Hi Andrew – thanks for your comment. I have emailed you. Yes I have many clients in China, and I can help with sending RMB out of the country.

Hi Andrew,

Thank you for your publications. They are very informative and promising. Do you accept British expats residing in Kuwait?

Hi Nav – yes I do. Anywhere except USA. I have emailed you.

Ciao Adam,

Thank you for your publications. They are very informative and promising. Do you accept British expats residing in Kuwait?

Hi Adam, any ideas about how this works in China?

Hi David – it is fine for China-based clients. However, you need to know how to get money out of China. I wrote an article about that before.