Expats can buy annuities, but the options differ from those available to residents. This is primarily due to residency and tax regulations.

In most cases, providers are required to handle international tax, currency, and regulatory compliance.

Questo articolo tratta di:

- Are annuities a good investment for expats?

- How to buy an annuity as an expat?

- How are annuities taxed for expats?

- What is a better alternative to an annuity?

Punti di forza:

- Annuities can provide guaranteed lifetime income, but tax and residency rules determine how they are treated.

- In many tax treaties, the country of residence has the primary taxing right, with credits preventing double taxation.

- Most annuities continue after you move abroad, though payment routing and withholding tax may change.

- Annuities often work best alongside drawdown or lump sums as part of a broader retirement strategy.

I miei recapiti sono hello@adamfayed.com e WhatsApp +44-7393-450-837 se avete domande. Offriamo anche soluzioni di strutturazione su misura per la vostra situazione.

Le informazioni contenute in questo articolo hanno carattere puramente indicativo, non costituiscono una consulenza finanziaria, legale o fiscale e possono essere cambiate rispetto al momento in cui sono state scritte.

What is an annuity and how does it work for expats?

An annuity converts a lump sum into a regular income, often for life. The core mechanics do not change for expats.

What changes for expats are:

- Where you are allowed to buy it

- How the income is taxed

- Which currency you receive payments in

So, the product is familiar, but the cross-border rules around it are not.

What is an annuity in retirement planning?

In pianificazione della pensione, an annuity converts a lump sum of savings into a stream of regular income, usually paid monthly for a fixed period or for the rest of your life.

Retirees often use annuities to create a predictable income alongside pensions, investimenti, or government benefits.

Annuity payouts are mainly determined by:

- Interest rates: Higher long-term interest rates typically allow insurers to offer higher payouts.

- Life expectancy: Age and actuarial life tables affect how long payments are expected to last.

- Premium size: Larger contributions generate higher income.

- Product features: Options such as inflation protection, survivor benefits, or guaranteed periods usually reduce the starting payout.

After global interest rates rose between 2022 and 2024, annuity payouts became more attractive again.

In major markets such as the US and UK, lifetime annuity income for a healthy 65-year-old has often ranged roughly between 6% and 7.5% of the invested capital annually, depending on product structure and market conditions.

The key trade-off is certainty versus flexibility.

Once purchased, most annuities cannot be reversed, but they provide stable income that continues even if you live longer than expected.

For this reason, many retirement plans use annuities to cover essential living costs while leaving other assets invested for growth.

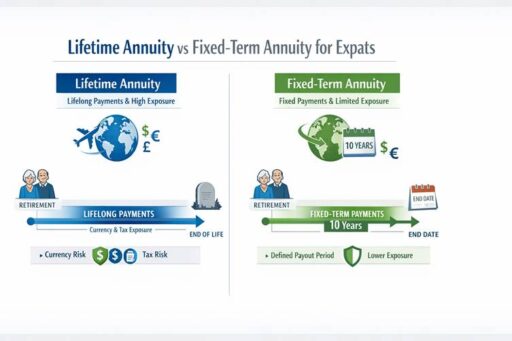

Lifetime annuity vs fixed-term annuity for overseas retirees

A lifetime annuity pays you for as long as you live, however long that is. A fixed-term annuity pays for a set period (for example, 10 or 20 years); after that, payments stop.

Lifetime annuities are better when you fear outliving your money, while fixed-term annuities can bridge a gap (for example, between retiring early and a state pension age) while keeping some flexibility later.

For expats:

- Lifetime annuities lock in long-term currency and tax exposure

- Fixed-term annuities limit that exposure to a known number of years

How to buy annuities as an expat?

To buy an annuity as an expat, you typically need to purchase it through a provider in the country where your pension is held or where you are tax-resident.

The process usually involves confirming residency status, complying with tax reporting rules, and meeting local pension access requirements.

Insurers must comply with local regulations, anti-money-laundering rules, and tax reporting requirements.

Key constraints include:

- Many providers sell only to local residents

- Pension access age rules still apply

- Some products are closed to overseas clients

Can you buy an annuity after moving abroad?

Yes, expats can sometimes buy an annuity after moving abroad, but eligibility varies based on the regulations of the issuing country and your residency status.

Some jurisdictions allow non-resident citizens (or people with local pension rights) to buy an annuity from abroad, usually with stricter documentation and limited advice options.

Others require you to be tax‑resident and physically resident to buy a retail annuity product, especially if it is linked to tax-favoured pension savings.

Offshore markets may allow expats of many nationalities to buy annuities, but fees, product complexity, and regulatory protection vary widely.

How long can you keep an annuity when you leave your home country?

Most annuity contracts continue for life or for the agreed term even after you move abroad. What changes are:

- Where the payments can be sent

- Whether tax is withheld at source

- How you report the income locally

Transferring an existing annuity to a new provider is usually not possible.

Buying an annuity before vs after becoming an expat

The timing of your annuity purchase can significantly affect product availability, regulation, and tax treatment.

Buying before you move usually gives you:

- More provider choice in your home market,

- Access to domestic retirement annuities that might not be sold to non-residents,

- Clearer consumer protection under your familiar regulator.

Buying after you move can make sense if:

- You plan to match income to your new country’s currency,

- You want your annuity taxed and regulated where you will actually live,

- Your new country offers specific expat-friendly products or international pension structures.

However, once you are an expat, it may be harder to find competitive products and qualified advice, so planning the timing before you move is often wise.

What is the tax treatment of annuities for expats?

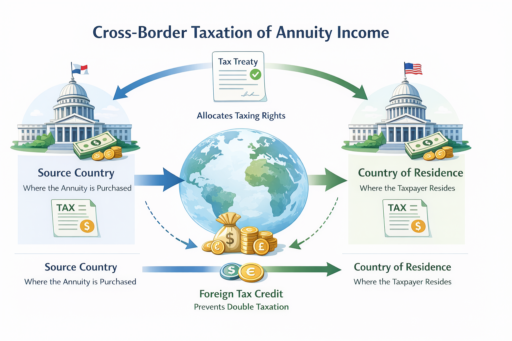

Annuity taxation becomes more complex when you live abroad because two countries may claim taxing rights over the same income.

In simple terms:

- Your country of residence often has the main right to tax your annuity income under many double taxation agreements.

- Your source country (where the annuity is issued) may also tax it, especially if there is no treaty or if the treaty explicitly allows source taxation.

- You generally do not get tax-free annuity income just because you moved abroad, although some countries exempt certain pension income or allow a tax-free capital element.

How is annuity income taxed when you live abroad?

In many bilateral tax treaties, the general rule is that private pensions and annuities are taxable only in the country where the recipient is resident, not in the source state.

However, some treaties allow both countries to tax, with the residence country giving a foreign‑tax credit.

If there is no treaty, you could face full tax in both countries, relying only on domestic foreign‑tax‑credit rules, if available.

Within a country, the tax code may treat annuity income like:

- Ordinary income (taxed at your marginal rate),

- Part capital recovery and part interest (only the interest element is taxed), or

- Exempt in special cases (e.g., some survivor or state-backed pensions, or annuities paid after a member’s death under specific rules).

Tax treatment of annuity income in your country of residence

Each country has its own way to classify and tax annuities:

- Some tax the full gross payment as pension income.

- Some separate the tax-free unrecovered capital element from the taxable profit element.

- Some give special relief if the annuity comes from a qualifying pension scheme or recognised overseas pension, or if you are a long-term resident.

Because rules vary widely, the honest answer is: this is determined by your country of residence. You need to check:

- Does your country have a tax treaty with the annuity’s source country?

- How does your country tax foreign pensions and foreign annuities?

- Can you claim foreign‑tax credits or exemptions?

How double taxation treaty works for annuity income?

Double taxation treaties determine which country has the right to tax annuity income when the payer and the recipient live in different countries.

The typical pattern is:

- Privato pensions/annuities are taxable only in the recipient’s state of residence

- Some treaties allow a limited source‑country tax, for example, a small withholding

- Public‑sector or government pensions may follow a different article and be taxed in the paying country unless an exception applies

In practice, if both countries have the right to tax, your residence country usually grants a foreign‑tax credit for tax already paid in the source country, up to its own tax on that income.

Can annuity payments be tax-free?

Completely tax-free annuity income is rare. You might see:

- A tax-free capital portion, where the law says part of each payment is just a return of your own contributions and therefore not taxed.

- Exempt treatment for certain pensions or annuities from recognised overseas pension schemes or after death, when specific conditions are met.

- Zero tax in practice if your personal allowance or low-income band in your residence country covers all your annuity income.

But moving abroad does not itself erase tax obligations.

Both the IRS and other tax authorities make clear that foreign pensions and annuities remain taxable according to domestic law and treaties.

How to Get Paid Annuities Abroad: Currency and International Transfers

When receiving annuity payments abroad, some providers will pay directly into a foreign bank account once you are classified as a non-resident.

Others require a domestic account.

Which currency should you choose?

Receiving income in the currency you spend reduces exchange-rate risk.

Receiving income in your home currency and converting it yourself:

- Gives control over timing

- Allows use of FX specialists

- Adds complexity and risk

Many expats use a split approach by holding assets and cash in more than one currency.

How to choose an annuity as an expat?

Choosing an annuity as an expat requires considering several cross-border factors, including tax residency, currency exposure, and family circumstances.

- Your long-term country of residence

- Your spending currency

- Whether a spouse depends on the income

- Your health

Fixed vs inflation-linked income for overseas living

Fixed annuities pay the same amount every year. With today’s higher fixed rates (often around 5–7% for certain terms in major markets), they can look appealing.

However, inflation in your new country can erode purchasing power over time.

Inflation-linked annuities start lower but rise each year with an index.

They better match long retirements in countries with higher or uncertain inflation, though they are less common and sometimes not available to non-residents.

Joint-life annuities for expat couples

Joint‑life annuities pay until both partners have died, often at a reduced rate after the first death (for example, 50% or 66% to the survivor).

They can be vital if one spouse is financially dependent or doesn’t qualify for much pension income in the new country.

Enhanced annuities for expats with health conditions

People with qualifying medical conditions may receive significantly higher income, but access for non-residents varies by provider.

Offshore vs domestic annuity options

Domestic annuities:

- Stronger consumer protection

- Simpler tax treatment

- Multi-currency flexibility

- More complex charging structures

- Variable regulatory strength

They are not automatically tax-free.

Do annuities make sense for expats?

They are most suitable if you:

- Need a guaranteed income to cover essential expenses

- Expect a long retirement

- Want protection from market volatility

They are less suitable if you:

- Plan to move countries frequently

- Want full access to your capital

- Have complex multi-country tax exposure

- Prioritise leaving a large inheritance

What are the pros and cons of annuities for expats?

For expats, annuities provide guaranteed income, protection against outliving your money, and, in some cases, tax benefits. However, they reduce flexibility and entail regulatory, jurisdictional, and currency risks.

It is important to weigh their advantages and limitations before committing capital.

Benefits of guaranteed income while living overseas

- Predictable monthly income to cover essential bills, no matter what markets or currencies do.

- Protection against longevity risk: if you live a very long time, the insurer, not you, carries the risk of your money running out.

- Psychological comfort, especially in volatile times, is one reason annuity demand has risen with higher rates.

- For some, favourable treatment inside pension systems (for example, allowed to satisfy minimum income rules or simplify tax reporting).

Risks of annuities for expat retirees

- Irreversibility: once you buy, you usually cannot get your somma forfettaria back or move the contract offshore.

- Currency and inflation risk if you lock into a currency that doesn’t match your long-term spending, or into a fixed income in a high-inflation country.

- Tax and regulatory risk: changes to tax treaties, residency rules, or pension law can affect net income.

- Provider and jurisdiction risk: weaker regulation or investor protection in some offshore centres could be a concern, especially for very long lifetimes.

What are alternatives to annuities for expats?

Expats have alternative options to generate retirement income like drawdowns, taking a lumpsum and investing globally, and using international retirement strategies.

Drawdown while living abroad

In a drawdown, your money stays invested (usually in funds or ETFs), and you choose how much to withdraw each year.

This gives flexibility, better potential growth, and more control over currency and tax timing, but you carry investment risk and the danger of running out of money if markets perform badly or you overspend.

As an expat, you must also track how your residence country taxes investment gains, dividends, and withdrawals.

Taking a lump sum and investing internationally

Some systems allow you to take part of your pension or annuity value as a lump sum, sometimes tax-free or tax-favoured.

You can then invest via international brokers, local tax-efficient wrappers, real estate, or business ventures.

This offers maximum flexibility and global diversification, but zero guarantees; all the risk and decision-making falls on you, and tax reporting across borders can become complex.

Using international retirement structures

International pension structures (for example, international SIPPs, QROPS-type arrangements, or similar offshore retirement plans) are wrappers designed to hold retirement assets for mobile individuals. These can:

- Consolidate multiple pensions

- Offer multi-currency investing

- Support either drawdown or later annuitisation

They are still taxed under local rules.

Expat Retirement: Sample Scenario

Let’s build a simple, realistic scenario to see how all of this plays out.

Alex, age 65, retires with a pension worth 500,000 and moves to a country that taxes foreign pension income at 10%.

Option 1: Lifetime annuity

- Income at 6.5%: 32,500

- Tax at 10%: 3,250

- Net income: 29,250

This provides a higher starting income but is tied to one currency.

Option 2: Drawdown

- 4% withdrawal: 20,000

- Tax at 10%: 2,000

- Net income: 18,000

Income is lower initially but the capital remains invested and flexible.

A blended strategy can provide both security and growth.

Conclusione

For expats, annuities are neither magic nor irrelevant; they are one tool in a larger cross-border retirement plan.

The key ideas are simple: track where your annuity is based, where you are tax‑resident, how treaties share taxing rights, which currency your income and expenses use, and how much flexibility you are willing to give up for guaranteed income.

Used carefully, often alongside drawdown and international pension structures, annuities can provide a strong, predictable floor of income that helps you enjoy life abroad without constantly worrying about markets and longevity.

Domande frequenti

How long does an annuity last?

Annuities can last either for a fixed term or for your entire life, based on the contract you choose.

How much does a 1,00,000 dollar annuity pay?

Recent lifetime rates for a healthy 65-year-old in major markets have often been roughly 6–7.5% before tax, based on terms and health.

Is 5% a good annuity rate?

It is competitive if similar products offer less, but less attractive if the market range is closer to 6–7%.

What is the best age to buy an annuity?

There is no universally best age, but annuity payouts generally improve as you get older because your life expectancy shortens, so the insurer expects to pay for fewer years.

Many people consider annuities in their 60s or early 70s, often when they stop work or draw their main pensions.

Are annuities a good idea for expats?

Annuities can be a good idea for expats who value guaranteed income for life, especially to cover essential expenses, and who understand the tax and currency implications across borders.

Siete afflitti dall'indecisione finanziaria?

Adam è un autore riconosciuto a livello internazionale in materia finanziaria con oltre 830 milioni di visualizzazioni di risposte su Quora, un libro molto venduto su Amazon e un contributo su Forbes.