You can live abroad on annuity income, as it can provide a predictable retirement cash flow.

Nevertheless, your net monthly income should cover housing, food, healthcare, transport, and daily living costs in your destination country.

Ideally, it is better to have a 20–30% financial buffer.

Questo articolo tratta di:

- Can you live off annuities while living abroad?

- What happens to your annuity if you move abroad?

- How to plan an estate while living abroad on annuities?

- What are the problems with annuities while living abroad?

Punti di forza:

- A guaranteed annuity can support retirement abroad if net income comfortably exceeds costs.

- Taxes, withholding rules, and currency conversion determine your real monthly income.

- Inflation and currency swings can erode purchasing power over long retirements.

- Mid-cost countries can stretch fixed retirement income significantly.

I miei recapiti sono hello@adamfayed.com e WhatsApp +44-7393-450-837 se avete domande. Offriamo anche soluzioni di strutturazione su misura per la vostra situazione.

Le informazioni contenute in questo articolo hanno carattere puramente indicativo, non costituiscono una consulenza finanziaria, legale o fiscale e possono essere cambiate rispetto al momento in cui sono state scritte.

How to live off an annuity abroad?

Living on annuity income overseas typically requires matching predictable income with realistic local expenses, rather than relying on investment withdrawals or variable income.

Key steps to manage annuity income abroad:

1. Calculate net income after taxes – Account for withholding taxes, local income tax, and transfer costs to know what you actually receive.

2. Assess cost of living – Compare housing, healthcare, groceries, and daily expenses in your destination. Mid-cost cities stretch a fixed annuity further.

3. Plan for currency exchange risk – If your annuity is paid in a different currency, fluctuations can affect your purchasing power.

4. Budget for healthcare expenses– Factor in international insurance or private healthcare, especially where public coverage is limited.

5. Maintain an emergency and inflation buffer – Keep 3–6 months of living expenses in savings to protect against unexpected costs or payment delays.

With careful budgeting, choosing an affordable location, and maintaining a cash reserve, many retirees successfully use annuity income as a stable financial foundation for living abroad.

Typical comfortable single-retiree budgets:

- Spain: €1,500 to €2,500

- Portugal: €1,400 to €2,200

- Thailand: $1,500 to $2,500 equivalent

Mid-sized towns are far more affordable than capital cities.

Your odds improve if you:

- Keep housing modest

- Avoid debt

- Maintain a cash buffer

How to receive an annuity abroad?

You can receive an annuity abroad by arranging direct international bank deposits or by transferring payments from a home-country bank account to your foreign account after the annuity is paid.

Once your residency and payment instructions are updated with the provider, annuity payments generally continue on the same schedule as before.

To receive payments smoothly while living overseas, you typically need to address three practical issues: payment routing, tax documentation, and international transfer costs.

Can annuity payments be sent to an international bank account?

- Some systems allow annuity income to be paid directly into a foreign bank account in your own name, especially if you are officially non-resident, but rules differ widely and can depend on central‑bank exchange‑control manuals.

- Where direct foreign payment is not allowed, you normally receive the annuity into a home‑country account and then transfer it abroad within your annual foreign‑exchange limits.

What happens if you change country after retirement?

- If you move from one foreign country to another, you usually keep the same annuity but must update your address, tax residency declarations, and sometimes proof of life or residency documents with the provider.

- Your tax position may change again, because each new country has its own rules for taxing foreign pension and annuity income and its own treaty network.

Payment frequency and international transfer fees

- Most annuities pay monthly, but some allow quarterly or annual payments; less frequent payments can reduce transfer costs but make budgeting harder.

- International transfers may involve fixed bank fees per payment plus a percentage FX spread, which can be trimmed by using specialist money‑transfer services or multi-currency accounts.

Monthly income stability in real life

- Once set up correctly, annuity payments are usually very reliable, but you may see small month‑to‑month changes in local‑currency amounts because of exchange rates and tax withholding adjustments.

- You should keep a cash buffer (for example, three to six months of expenses) in local currency so a slow or delayed transfer never leaves you short for rent or healthcare.

How to plan income considering the cost of living?

You plan around the costo della vita by matching your net annuity income to realistic local budgets, then adding buffers for inflation, currency risk, and emergencies.

You can also blend your annuity with part-time work, rental income, or drawdown from savings to improve flexibility.

Matching annuity income to your retirement destination

Plan by:

- Listing core expenses

- Comparing them with realistic local budgets

- Ensuring a 20 to 30% surplus

You can improve flexibility by combining an annuity with:

- Part-time remote work

- Rental income

- Drawdown savings

The inflation impact when living abroad

Even if your annuity rises with inflation in its home country:

- Your new country may have different inflation

- Currency moves may offset increases

Review your position every year.

What is your net monthly income after local tax?

Your net monthly income after local tax is the amount you receive after withholding taxes, local income taxes, currency conversion, and transfer fees are deducted from your annuity.

When you move abroad, you may face withholding tax in the paying country, local income tax in your new home, and exchange rate fluctuations when you convert your annuity currency into local money.

Gross vs net income

You live on net income, not the contractual payment.

Your real monthly amount can be reduced by:

- Withholding tax in the source country

- Local income tax in your new country

- Transfer and FX costs

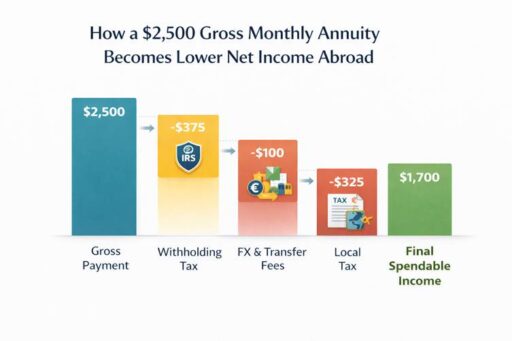

Esempio:

- Gross annuity: $2,500

- 10% withholding: –$250

- 2% FX/transfer: –$45

Net received: $2,205

Local tax may reduce this further.

Tax treaties often prevent double taxation, but only if the correct residency and treaty forms are filed.

Local tax impact

- Some countries tax worldwide income once you become a tax resident, including foreign pensions and annuities, while others focus only on local‑source income or provide special exemptions for foreign retirees.

- Tax treaties between countries sometimes reduce double taxation by allowing pension or annuity income to be taxed mainly in one country, but you may need forms and proof of residency to benefit.

Ritenuta d'acconto

- The paying country may automatically withhold tax from your annuity, especially if you are treated as a non-resident or non-resident alien for tax purposes.

- In some systems (for example, the US and Australia), you can sometimes claim treaty‑reduced withholding or an exemption by submitting the right forms (such as a W‑8BEN in the US or local treaty forms elsewhere) and proof of foreign residency.

Currency conversion effect

If income and spending are in different currencies:

- A strong local currency reduces your buying power

- A weak local currency increases it

FX fees typically cost 1 to 3% per transfer unless you use specialist providers.

Keep 3 to 6 months of expenses in local currency to avoid timing risk.

Simple net income calculation example

Imagine:

- Your gross annuity: 2,500 USD per month.

- Withholding tax in paying country: 10% (250 USD).

- Transfer and FX fees: 2% of the remaining 2,250 USD (about 45 USD).

Net into your foreign bank: 2,205 USD per month (around 88% of gross). Local income tax may then further reduce this, depending on your residency and treaty rules.

How are annuities handled in an estate?

Estate planning for annuities overseas is about understanding what happens to payments when you die, where your beneficiaries live, and how different countries tax those benefits.

Some annuities stop at your death; others continue for a spouse or for a guaranteed period.

What happens to your annuity when you die overseas?

- A single‑life annuity with no guarantees usually stops when you die, no matter where you live; there is often no money for heirs because you traded the capital for lifetime income.

- If you die overseas with a joint‑life or guaranteed‑period annuity, the provider still follows the contract, but your heirs may have to prove your death and their identity across borders.

Cross-border beneficiary considerations

- If your beneficiaries live in a different country than you or the annuity provider, they may face different tax rules, reporting requirements, and delays when receiving any continuing income or death benefits.

- You should keep beneficiary details updated, store policy documents where heirs can access them, and consider a local will in your country of residence, plus a will in your home country, drafted by lawyers who understand cross-border estates.

Joint life

- A joint‑life annuity continues paying after your death to a second person (often a spouse or partner), usually at 50–100% of the original income, until that person also dies.

- Joint‑life options cost more at purchase (you get a lower starting income) but can protect a non-earning spouse who depends on your annuity, especially if they will also live abroad.

Guarantee periods

- Many annuities offer a guaranteed payment period, for example, 10 or 20 years; if you die early within that period, payments continue to your estate or named beneficiaries until the guarantee ends.

- Longer guarantees reduce the risk that you lose your capital with an early death, but they also reduce your initial income compared with a no-guarantee annuity.

Tax for heirs

- Some countries treat remaining annuity payments or death benefits as taxable income for beneficiaries, while others treat them as part of the deceased’s estate and apply inheritance or estate tax instead.

- If heirs are in yet another country, they might have to declare income or inheritances there too, so cross-border advice is important for larger estates.

Is an annuity a good idea for retirement?

Un rendita is useful if you value simplicity and guaranteed income more than flexibility; it helps you avoid overspending because the monthly amount is fixed by contract.

The trade-off is that many annuities, especially level ones, do not automatically rise with inflation.

Therefore, your real buying power can decline over a 20- or 30-year retirement, especially if you live abroad and face currency swings.

Best countries to live on a guaranteed retirement income

The best countries to live on a guaranteed retirement income are those with lower living costs and accessible healthcare, allowing fixed payments to stretch further.

Popular examples include Spain, Portugal, and Thailand, where rent, groceries, and everyday expenses are generally lower than in major financial hubs.

These destinations are especially attractive for retirees living on annuities or pensions because predictable monthly income can cover a larger share of living costs.

In addition, many retirement visas require proof of stable income, making guaranteed payments from pensions or annuities an advantage when applying for long-term residency.

What are the issues with annuities overseas?

Living abroad with annuities works, but it comes with practical headaches: frozen payments, compliance checks, proof‑of‑life forms, and cross-border banking friction.

You must stay organised with documents and keep your provider updated.

Frozen payments and compliance checks

- Providers sometimes freeze payments if mail bounces, your bank rejects transfers, they suspect fraud, or regulations change for payments to your country.

- You may need to provide updated ID, proof of address, tax forms, or bank letters to unfreeze payments, so keep digital copies handy and respond quickly to any notices.

Proof-of-life requirements

- Some pension and annuity systems periodically ask for proof of life certificates, often signed by a local authority, lawyer, or notary; if you do not return these, payments can stop.

- As an expat, you may have to visit a consulate, local government office, or doctor to get the form stamped, so build this into your annual admin routine.

Banking and documentation issues

- Foreign addresses, new passports, and changing residency statuses can trigger additional KYC checks at banks and annuity providers, especially when sending money to certain countries.

- To reduce hassle, keep your passport valid, hold a stable main bank account, and avoid frequent unexplained changes in where payments go.

Retiring Abroad on An Annuity: Sample Budget

Let’s build simple example budgets for a single retiree with a net annuity of 2,500 USD per month, converted to local currency.

These are illustrative only, but they show how the same annuity can feel very different in Spain, Thailand, and Portugal.

Spain: mid-size city

Assume:

- Net annuity: 2,500 USD = about 2,300 euros (after FX and fees).

- Typical comfortable budget in a mid-size city: 1,800–2,200 euros per month.

Sample monthly budget (euros):

- Rent (one‑bedroom, mid-size city): 800

- Utilities and internet: 150

- Food and groceries: 350

- Local transport: 80

- Health insurance/top-ups: 120

- Leisure, eating out, misc.: 300

Total: 1,800 euros. Surplus: about 500 euros. This looks sustainable, with some buffer for travel or savings and for inflation over time.

Thailand: Chiang Mai or a similar city

Assume:

- Net annuity: 2,500 USD = about 90,000 THB.

- Comfortable budget range: 50,000–100,000 THB per month.

Sample monthly budget (THB):

- Rent (nice one-bedroom condo): 20,000

- Utilities and internet: 3,000

- Food and groceries (mix local/imported): 15,000

- Local transport and scooter/taxis: 5,000

- Health insurance: 10,000

- Leisure, massages, short trips: 15,000

Total: 68,000 THB. Surplus: about 22,000 THB. This leaves a solid margin for emergencies or extra travel, but you must watch currency swings if your annuity is not in THB.

Portugal: a smaller town

Assume:

- Net annuity: 2,500 USD = about 2,300 euros.

- Comfortable smaller‑town budgets: 1,400–1,800 euros per month.

Sample monthly budget (euros):

- Rent (modest one‑bedroom): 700

- Utilities and internet: 120

- Food and groceries: 300

- Local transport: 60

- Health insurance: 120

- Leisure, eating out, misc.: 250

Total: 1,550 euros. Surplus: about 750 euros, which is a strong buffer for inflation, trips home, or building a cash reserve.

Across all three, the same annuity feels tight in high-cost capitals but comfortable in mid-cost towns and cities. That is the core decision lever you control.

Conclusione

Living abroad on annuity income is feasible if your net income comfortably exceeds local living costs and you understand tax, currency, and healthcare expenses.

Retirees should focus on three fundamentals: calculating true net income, choosing an affordable destination, and reviewing exchange-rate and inflation effects regularly.

When those factors are managed well, annuities can provide a stable retirement income stream for expats.

Domande frequenti

What happens to my living annuity if I move abroad?

Your living annuity usually stays in the original system, but your tax and payment route change.

You must tell the provider your new address, update residency and tax forms, and set up either direct foreign payments (if allowed) or transfers from a home‑country bank account.

Local tax in your new country may then apply to the income.

What happens to my living annuity if I die early?

Unlike a life annuity, a living annuity is typically an investment wrapper; if you die early, the remaining capital normally passes to your nominated beneficiaries.

They may be able to take a lump sum, continue as annuity owners, or transfer the balance into other retirement products, subject to tax rules in the paying and receiving countries.

Can I live abroad on annuity income alone?

Yes, if your net annuity is comfortably above realistic local budgets, especially for rent and healthcare, in your chosen country.

Many retirees do this in places like mid-cost Spanish or Portuguese towns or in Thai cities where 1,500–2,500 USD a month can still buy a good standard of living.

Can I change the bank account for my annuity payments?

Normally, yes; you can switch to another account in your name, sometimes including foreign accounts if local rules and your provider allow it.

You will usually need to complete forms and provide proof of the new account to satisfy anti-money‑laundering checks.

Is a level annuity risky if I retire overseas?

A level annuity is safe in the sense that it keeps paying, but risky in terms of buying power, especially if you face local inflation and currency swings.

If prices in your new country rise faster than any income increases you receive, you may feel poorer over time, so you must plan for future belt-tightening or add other income sources.

Siete afflitti dall'indecisione finanziaria?

Adam è un autore riconosciuto a livello internazionale in materia finanziaria con oltre 830 milioni di visualizzazioni di risposte su Quora, un libro molto venduto su Amazon e un contributo su Forbes.