I often write on Quora.com, where I am the most viewed writer on financial matters, with over 657.2 million views in recent years.

In the answers below I focused on the following topics and issues:

- Are you losing money if you put it into a bank?

- What are some lies we are told about money?

- What is the secret of the top 1% of people?

- Why do people keep money in a bank instead of using it smart and investing?

- Why has stock market of country like Japan given bad performance to investors over the years?

- What is the importance of rebalancing a portfolio? How do you do that?

- Which countries’ economies will grow the most by 2066? Where will economies be “booming” in the future?

- What are the bitter truths about smart people?

- Why do people think it’s ridiculous to leave money in the bank when investing comes with risk and the stock market is prone to downturns? I debunk the idea behind the question.

- Why don’t so many people save money for their future? What if something bad or imminent happens? How could they go through without money?

- Is 200 thousand dollars enough for retirement?

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Some of the links and videos referred to might only be available on the original answer

Are you losing money if you put it into a bank?

This picture should answer your question:

You don’t need to directly lose money.

Consistently losing money to inflation will do the trick.

What are some lies we are told about money?

Ask most people what is the best investment.

In most countries, the majority of people will say real estate.

In some countries, people might even think that “renting is for losers”.

The reason is simple.

They think Grandma Alma bought a house for $75,000. It is now worth $1.2m. What a steal!

What is more, renting is dead money right?

But have they:

- Considered whether Alma has adjusted for inflation which compounded over time?

- Factored in the taxes and ongoing costs of the property?

- Accounted for indirect costs? For example, did the house stop them from moving to get a better-paid job?

- Looked at the performance of that house versus the S&P500 and other investments, and thereby accounted for the indirect costs of getting a bigger house, when buying a smaller house and investing more is also an option?

- Compared how much somebody would have by renting and investing more into something like the S&P500

- Time-adjusted return on investment (ROI). Time is money. If you own a house, more things are up to you. When you rent, your landlord or the management company saves you time.

People don’t factor in these things. If a house “increases” in value from 500,000 to 515,000, and inflation is 3.1%, you are losing money because:

- The price has gone up less than inflation

- The costs will also be higher than renting

- You could have put more money into other investments .

- All the other indirect costs

I don’t agree with everything Robert Kiyosaki says, but his comment that a primary residency (unlike rental property) is more of a liability than an asset is so true:

Don’t get me wrong, there are good reasons to buy, which go beyond financial reasons.

It allows you to settle down, give kids stability and much else.

It is just a mistake to think it is always the best financial decision.

It is only a sound financial decision in limited situations, for example, if rents are costly relative to buying.

One of my best financial decisions in my 20s was not pining myself down. I moved around a lot and learned a lot.

As soon as I earned serious money, I invested in liquid investments and back into my business, which was fast growing.

I didn’t consider buying a home until my net worth was in the multiple millions. Even now, whilst I am open to it for the first time, I struggle to get beyond the direct and indirect costs.

Unless I can get a 100% mortgage, that deposit money is money I can’t reinvest into myself, my business and/or more liquid and productive stock market investments, which have historically outperformed property.

So, if I do buy, it will be a purely non-financial decision.

If the rest of the world had similar attitudes to some countries like Germany and Japan, where buying is merely considered a home rather than an investment, it would be better.

What is the secret of the top 1% of people?

Why do you assume there is a secret?

The information is publicly available if you are speaking about the top 1% in terms of performance or financial wealth.

Most people know basic things these days, such as the power of compound interest.

In the pre-internet era, knowledge was vital. Knowledge alone was worth more. Academic books sometimes sold for more in the 1980s than today, despite all the inflation since then.

You now have world-class courses on places like Coursera, which only charge $25 or $5-$10 monthly.

These days, knowing alone isn’t good enough. You can’t just have loads of knowledge and charge loads of money for something. At least not in most cases.

The money is in:

- Implementation. Not ideas or knowledge. Implementing your knowledge.

- Leveraging. Implementing your knowledge is one thing. If you can build a team with that knowledge, you can then leverage the knowledge. Or perhaps you can use technology to leverage.

- Asking the right questions. For example, what am I willing to do, that others won’t? You might be willing to work very hard, but so are 20% of other people. Therefore, getting used to taking more risks than other people is one example of increasing the likelihood of getting inside the top 1%.

- Thinking differently also increases the likelihood of getting inside the top 1%. My “big break” was when I went completely online, remote and global years before it became fashionable. Many people thought it was crazy. Then they thought I was a visionary. Yet I have also had so many other failed ideas. So, experimenting with different ideas seen as eccentric will increase your chances. Remember this quote from AZ quotes:

Finally, there is something else that very few people speak about.

Once you start succeeding, many people take their foot off the peddle. They get complacent.

Sticking to your guns after achieving success is more different than people think.

So, staying inside the top 1% of any industry is more complicated than getting there for a few years.

Look at your favourite sport. You will find only a small fraction stay at the top long-term.

Why do people keep money in a bank instead of using it smart and investing?

One of the biggest reasons is a misconception.

That misconception is that investing is risky, and keeping cash in the bank is safe.

The fact is, every year, people lose money from keeping money in the bank. This year it is people living in Lebanon, Pakistan, Argentina and a few other places.

People living in the UK and some other countries are merely losing money to inflation.

Yet nobody has ever lost money investing in a broad-based index, holding for decades and reinvesting dividends.

This graph, taken from Twitter, shows that. If the graph was extended to 20 or 30 years, the numbers would be even more revealing.

There are some excellent reasons to keep some money in cash, though.

Investing is best done long-term. So, investing for a short-term objective, like paying for a wedding usually doesn’t make sense.

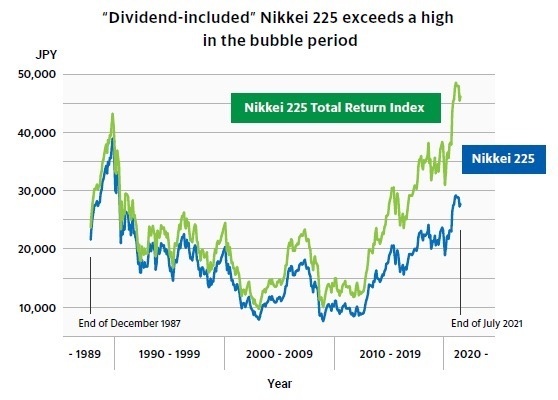

Why has stock market of country like Japan given bad performance to investors over the years?

Firstly, it is a misconception that the Japanese stock market hasn’t ever recovered from its height.

If you owned a rental property down 10%-20%, you wouldn’t lose money unless the rental income was low.

The same is true for the Nikkei. The capital appreciation has never recovered, but with dividends reinvested, it has done OK, as per the graph below from Nikkei’s website.

Since the graph was made, the Nikkei has increased to 33,000, so the chart will be even more telling once it has been updated.

Moreover, hardly anybody would have been so unlucky to have bought it as a one-off at the peak.

More realistically, people would invest monthly or yearly.

If somebody had invested $1,000 a month into the Nikkei for thirty of forty years, and reinvested income, the returns would have been pretty good.

The reason is that valuations were only crazy high for a very short time.

The Nikkei has done almost as well as the US stock market from 1945-today, 1970-today or 2008-today. Or even 1995-today.

It just hasn’t done well since the late 1980s-today. That means anybody unlucky enough to have bought only during that high period would have done poorly compared to alternative investments.

Saying that US and even European firms are more international than many Japanese firms, and the Japanese population will likely continue to fall.

So, there is no reason for people outside of Japan to want to put large amounts of money into the Japanese stock market compared to the US and some other international ones.

What is the importance of rebalancing a portfolio? How do you do that?

It isn’t essential if you are very young.

Nothing is wrong with being 100% in stocks in your 20s, 30s or 40s.

That is provided:

- You don’t panic when markets are down

- You have fresh money coming in to even into the markets

- 90%+ of your portfolio is in the indexes. Being 100% in the S&P500 or MSCI World when you are young isn’t risky, provided you are ulta long-term.

But let’s say you are older or prefer to see less volatility in your accounts.

In this case, owning other assets, such as bonds and money market funds, makes sense.

This is where rebalancing comes in. Let’s say you want 70% in the markets and 30% in other assets. In other words, a moderate-risk portfolio.

At the start of the year, you have 350,000 in stock market indexes and 150,000 in other assets.

The markets fall to 300,000, and the other assets go up to 155,000.

Now the portfolio is worth 455,000. The stocks have fallen to 65% of the portfolio.

You can now rebalance by selling some of the bonds or money market funds and buying stocks, to maintain the 70%-30% allocation.

The same thing applies if stocks soar. If you have a $1m account (700,000 in stocks and 300,000 in non-stock assets), and the stocks rise to $900,000 quickly, you can sell off some of the stocks to revert to the 70%-30% allocation.

It is, therefore, a good way to manage risk without trying to keep money in cash, thereby losing out on returns, and being afraid of market falls

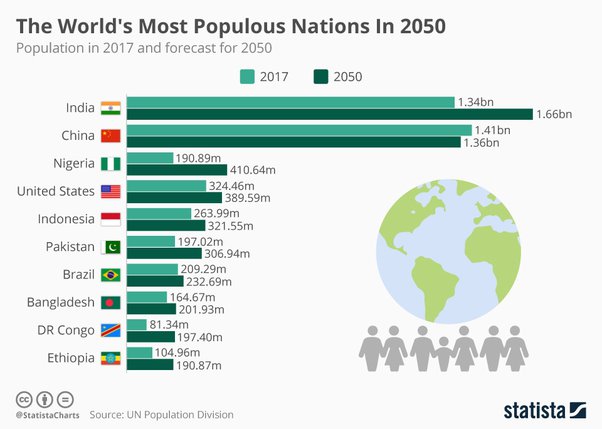

Which countries’ economies will grow the most by 2066? Where will economies be “booming” in the future?

This man’s predictions should be a warning to anybody who thinks that predicting the economy’s future is easy.

Jim O’Neill coined BRIC, and then BRICS for Brazil, Russia, India, China and South Africa.

If you hear about BRICS today, it is likely some silly idea that they are about to displace the USD with a gold-based system.

Over a decade ago, the idea was that growth would go to these economies. It hasn’t happened as expected.

South Africa, Brazil and Russia have struggled badly. China did well in the early years of the BRICS acronym being used.

But most economists think China will only grow by 2%-4%, on average, in the next ten to fifteen years.

Even in the last five or six years, they have struggled to grow as expected. Hardly anybody in 2007 or 2010, or even 2015 thought China’s growth prospects would be this weak for the 2020s and 2030s.

India is perhaps the only one of the five he has gotten completely right, assuming they don’t struggle.

Anyway, to answer your question, my money would be on certain African countries, South East Asia and some specific countries in the Middle East, such as Saudi Arabia, now they are opening up.

The latter “bet” depends on whether they deal with the transition from oil well.

I also wouldn’t bet against the USD being the world’s biggest economy by 2066 due to China’s slowdown.

Nobody really knows. What is easier to predict is population movements.

The predictions from Statista show potential populations in 2050:

And 2100 from the same website:

What do we see? African countries will have more people.

That means GDP will skyrocket even if they don’t develop as much as expected.

It is basic maths. If Nigeria has more than 400% more people by the end of the century, it will have over 400% more GDP, even in the unlikely case that they have zero per capita growth.

If they have 400%-500% more people + solid growth, their GDP will be over 1000% bigger.

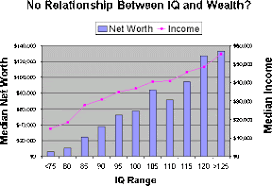

What are the bitter truths about smart people?

One of the bitter truths is that being smart doesn’t always mean you will be happier, earn more or be wealthier.

There is indeed a correlation between IQ test results and higher wealth and income.

This graph from IQs Corner shows that.

Yet an average is just that—an average. People who don’t have a job drag down the average, as do those with addictions or other issues.

Some of the wealthiest businesspeople and investors don’t have a high IQ. Many aren’t especially smart.

Many just:

- Took as many risks as possible, or took the risks early when they were younger

- Invested early and compounded over time

- Have slightly higher than average intelligence and coupled that with a great work ethic

- Use leveraged. That doesn’t just mean debt. It can mean leveraging other people, technology and other things

- Know how to market and sell themselves

- Don’t overthink like some very smart people

Being smart in isolation isn’t enough.

Having knowledge and cognitive intelligence becomes useful when it is combined with other skills and mentalities.

Simple example. If a very smart person learns eight languages perfectly but can’t use them commercially, that isn’t as useful as learning two and knowing how to do business in those two languages well.

Why do people think it’s ridiculous to leave money in the bank when investing comes with risk and the stock market is prone to downturns?

It depends on who you mean by people.

Most people don’t think like this.

Most people, in most countries at least, think that “investing” beyond property or cash is only for the rich, or at least the wealthy.

What is true is that most wealthy and financial literature people do often think this way.

The reasons are simple.

- Keeping money isn’t risk-free. In fact, it can be the riskiest decision of all, due to:

- Banking collapses like in Lebanon now

- Inflation eroding savings

- Relatively losing money to other assets

- You are putting all your eggs in one basket. A sensible investor wouldn’t put 100% in just one home or just one stock, even a blue-chip company like Apple. So, you are taking a massive risk unless you put your cash into ten different major currencies, earning interest on each.

- Depreciation risk. There doesn’t need to be a collapse like in some developing countries, or Germany in the 1920s. Ask anybody who left money in the UK when the Pound was 2:1 against the dollar, what deprecation means.

Ray Dalio’s “cash is trash” video explains it:

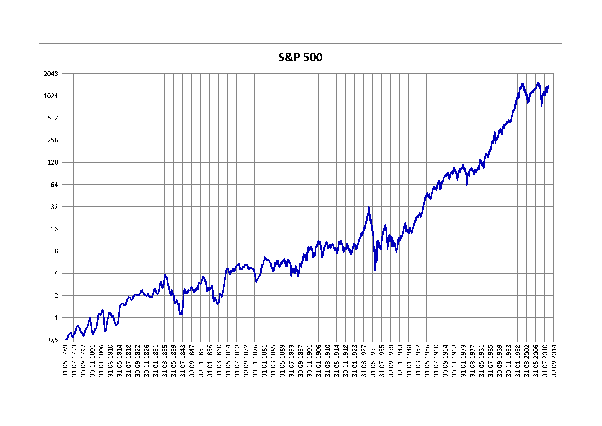

2. Investing doesn’t have to be risky

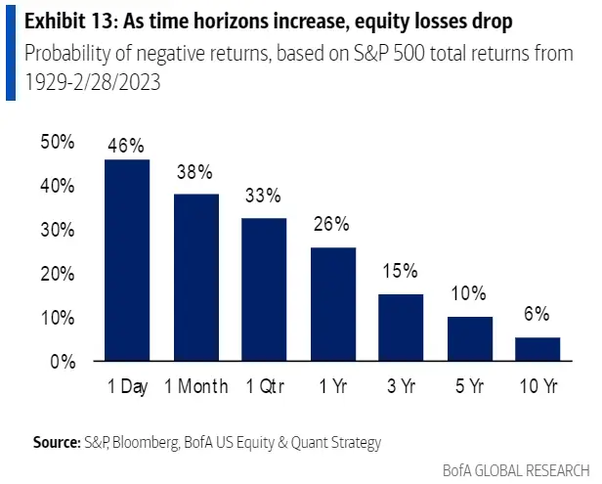

- Investing for one day or even a year is risky. Investing in one or even ten stocks is risky. Investing in the entire market for decades isn’t. The S&P500 is an index which is invested in five hundred stocks. It has never been down over a 20–30 year period.

- Downturns are irrelevant if you buy and hold and add more. Look at a long-term graph. They look irrelevant:

If we look at a much longer-term graph, you would need a magnified glass to see some of the falls

Why don’t so many people save money for their future? What if something bad or imminent happens? How could they go through without money?

There are commonalities here between health and wealth.

I watched this great episode of The Diary of a CEO today:

The interviewer is 30. He admitted that he doesn’t take his health as seriously as he should and plans to take it more seriously after 45.

The expert says this is understandable. The issue is, it is harder to move away from an iceberg if it is closer to you than if it is far away.

Therefore, it makes sense to take action now, rather than later.

Most people don’t think about these things until their 40s or when they have kids.

At 18:00, he compares people in their 20s and 30s not saving and investing for retirement.

It seems so long away; taking no action won’t affect your quality of life today, and most people think they won’t have a good quality of life later on.

Many people feel better at 50 than at 20, and time flies faster than people think.

Many Quora answers about the biggest regrets people have listed not investing sooner because “I would be retired by now”.

Is 200 thousand dollars enough for retirement?

It isn’t in most advanced countries.

At least not in isolation.

If somebody has 200k + a house which is paid off + a pension then of course it is.

In the UK, some people don’t have a penny of savings, but have good indirect savings from private pensions.

Final salary pensions used to be popular in many countries, and in this case, people don’t need many savings.

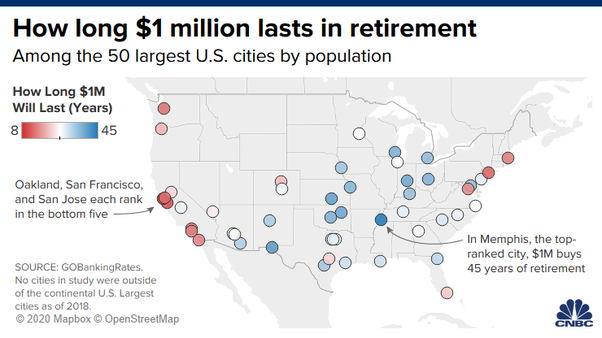

Even $1million isn’t enough in many developed countries if you are only relying on the savings.

This graph from CNBC tells its own story about how long $1million lasts in different US states: