Adam Fayed In The Media

Reuters announcement on Africa and Singapore push

SINGAPORE, June 9, 2025 (EZ Newswire) — British financial entrepreneur Adam Fayed, opens new tab has announced a push across East and West Africa, with plans to

SINGAPORE, June 9, 2025 (EZ Newswire) — British financial entrepreneur Adam Fayed, opens new tab has announced a push across East and West Africa, with plans to

We are looking for businesses to buy, in the financial services industry.

I am delighted to announce that I have re-released my 2018 Amazon book…..completely for free! The updated 2024 version includes answering questions such as: The

What makes me different, and how does that benefit you?

Gain your free expat financial and investing guides today

What are the 6 biggest reasons for expats and HNWI to have an advisor?

Recent client case studies

I am happy to announce my 34th LinkedIn review

adamfayed.com on Forbes – I am delighted to announce that I will soon be a regular contributor for Forbes.com

A second passport for Moldovan citizens refers to obtaining citizenship outside Moldova, commonly in countries like Romania, Italy, Portugal, or other EU and mobility-focused destinations

A second passport for Bolivians is typically obtained through residency-based naturalization in countries like Portugal, Paraguay, or Uruguay, or faster investment routes in the Caribbean

A second passport for Brazil can open wider global mobility, with many Brazilians exploring options such as Portugal, the United States, Canada, and Caribbean citizenship-by-investment

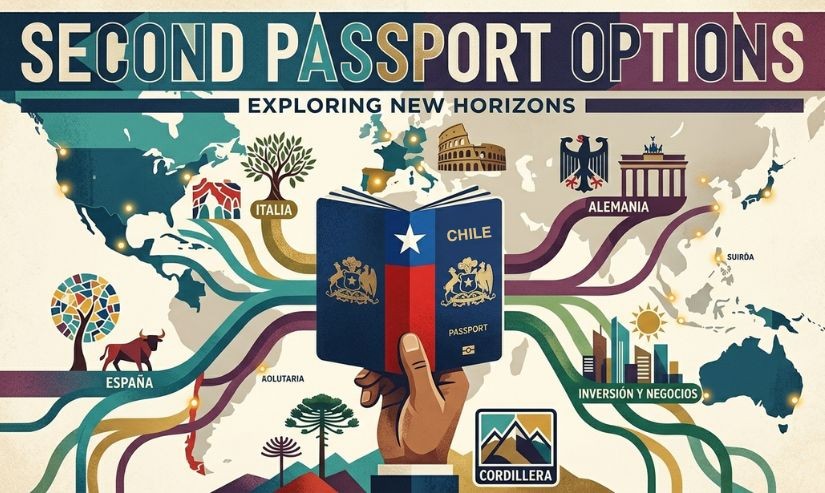

Chilean citizens can obtain a second passport through top options like Portugal, Paraguay, Uruguay, and fast-track Caribbean programs without giving up their Chilean nationality. The

A second passport for Colombians typically involves obtaining citizenship in countries like Portugal, Spain, Uruguay, or Caribbean nations such as Dominica and St. Kitts &

A second passport for Ecuador refers to Ecuadorian citizens legally acquiring another nationality, with the most common options including Spain, the United States, Portugal, and

A second passport for Paraguayans is most commonly pursued through fast-track naturalization in Spain or regional pathways in Uruguay and Argentina, with some also opting

A second passport for Peruvians refers to obtaining an additional nationality alongside Peruvian citizenship, with common top options for Peruvians including Spain, Portugal, Canada, and

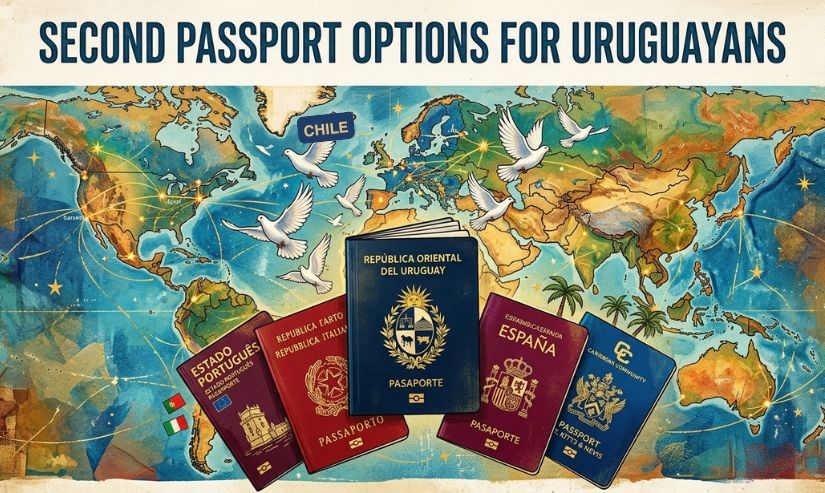

A second passport for Uruguayans is most commonly obtained through Spain, Portugal, or Italy via residency or ancestry, with faster options available in Grenada. The

A second passport for Venezuela typically involves Venezuelans acquiring citizenship in countries such as Spain, Colombia, Peru, Chile, Brazil, or the United States while retaining

A second passport for Costa Rica is most commonly pursued through Spain, Italy, Paraguay, Portugal, or Caribbean programs like Dominica to expand visa-free access and

The most relevant options for a second passport for El Salvador include pathways connected to the United States, Spain, Italy, and select Caribbean citizenship-by-investment programs.

To create a will in Germany, you must draft a legally valid Testament that follows strict formal requirements under the Bürgerliches Gesetzbuch. Any mistake in

Putting property into an offshore life insurance policy allows you to hold assets like cash, investments, or real estate within an international life insurance structure.

Setting up an NRI trust offers tax benefits such as income distribution efficiency, capital gains planning, and streamlined wealth transfer in India. It can reduce

To live comfortably overseas in 2026 on investment income alone, most individuals will need a passive income stream of roughly $2,000–$7,000+ per month. This depends

Writing a will in India means clearly recording how your assets should be distributed after your death in accordance with the Indian Succession Act, 1925.

Retirement planning in Uganda means building your own long-term income security in a country where public pensions cover only a small minority of workers and

Financial advice is professional guidance that helps individuals make informed decisions about saving, investing, tax strategy, retirement, and wealth protection. It is one of the

The seven main types of investment are equities, debt instruments, mutual funds, real estate, cash equivalents, commodities, and pensions. Each category has a different risk,

Trusts in India are legal arrangements where one person transfers assets to trustees, who hold and manage those assets for specified beneficiaries or purposes. Trusts