Wealth/Asset Management

Placing Crypto in a Trust: Key Steps, Tax Rules, and Benefits

Putting crypto in a trust allows you to legally transfer, secure, and manage your digital assets through a formal estate planning structure. It also helps

Putting crypto in a trust allows you to legally transfer, secure, and manage your digital assets through a formal estate planning structure. It also helps

Spain has officially ended its Golden Visa program, leaving non-EU nationals seeking residency and citizenship to explore alternative pathways. These Spain Golden Visa alternatives include

The best investments in South Africa in 2026 include top sectors such as real estate, renewable energy, fintech, and agriculture. These sectors offer strong potential

The best investment in Uganda in 2026 capitalizes on its fast-growing agriculture, renewable energy projects, real estate boom, and emerging tech startups. With rising domestic

Private Placement Life Insurance (PPLI) is an advanced life insurance solution tailored for high-net-worth individuals and sophisticated investors. Unlike traditional life insurance products, PPLI in

Offshore bonds give UK residents and returning expats powerful tax benefits by allowing investment growth to roll up tax-deferred and enabling 5% tax-advantaged withdrawals. They

Estate planning in Spain is more complex than in many other European countries because of forced heirship rules, regional tax differences, and separate inheritance laws

The best countries for registering a crypto company are generally considered to be Switzerland, Singapore, Dubai (UAE), and Estonia. These jurisdictions offer the most attractive

Using offshore companies for crypto is one of the most effective ways to protect digital assets, optimize tax exposure, and operate in clearer regulatory environments.

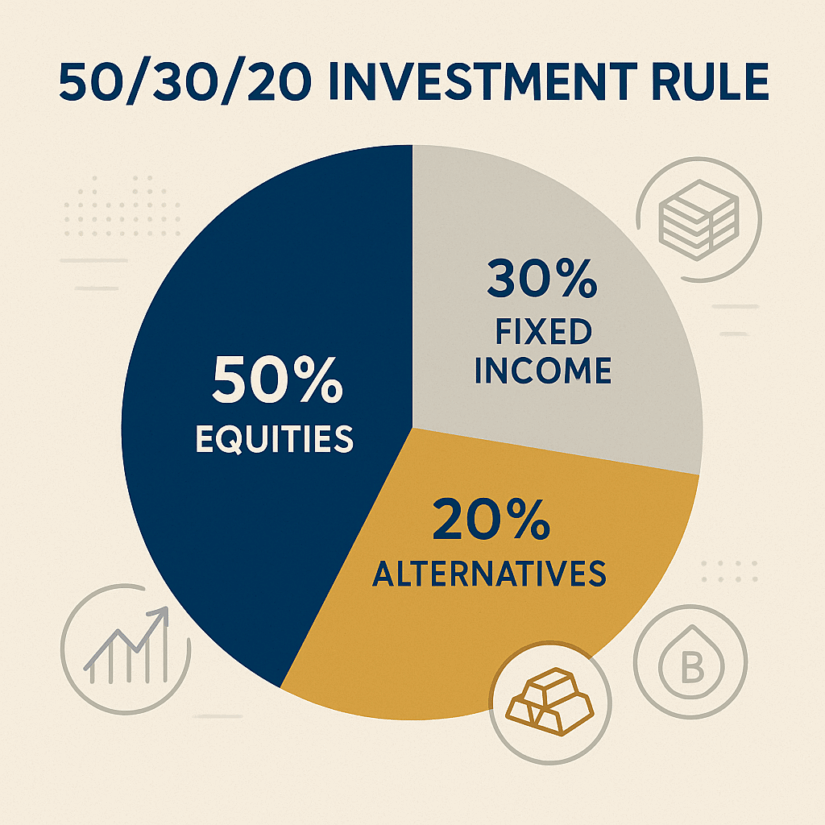

The 50/30/20 rule for allocating assets offers better diversification, downside protection, and risk-adjusted returns than a traditional 60/40 portfolio. By slightly reducing equities, keeping a

The first step to expat tax planning is understanding how your home and host countries tax your income. Without this foundation, you risk overpaying or

The best strategy for retirement planning in 2026 is to combine diversified, inflation-resilient investments with long-term tax-efficient structures that protect your wealth across borders. With

Travelers from visa-exempt countries, such as the United States and Canada, will need ETIAS authorization to enter the Schengen Area and other ETIAS countries starting

Offshore crypto security is critical for high-net-worth investors who want to protect crypto offshore using cold storage, multi-signature wallets, and legal structures. Wealthy investors and

Cold storage remains the best crypto asset protection in 2026 for safeguarding significant digital wealth. High-net-worth investors also rely on multi-signature wallets, institutional custodians, and

The best investment strategies in 2026 focus on globally diversified portfolios that combine high-quality fixed income with growth assets like technology, private credit, and selective

Asset protection strategies in 2026 focus on stronger legal structures, offshore diversification, and lawsuit-resistant entities. Rising litigation risk, global tax shifts, and government scrutiny are

Expat wealth management trends in 2026 are increasingly driven by AI-powered investment tools, ESG-focused portfolios, and cross-border tax optimization strategies. Expats are no longer relying

Best offshore investments in 2026 include global index funds, offshore bonds, private banking portfolios, and regulated international real estate options. These vehicles remain popular for

Shariah compliant investments in Europe are now widely accessible, offering expats and high-net-worth individuals clear options such as sukuk, halal ETFs, Islamic real estate funds,

A trust allows you to manage how and when your assets are distributed, even after death or if you become incapacitated. Choosing a trust instead