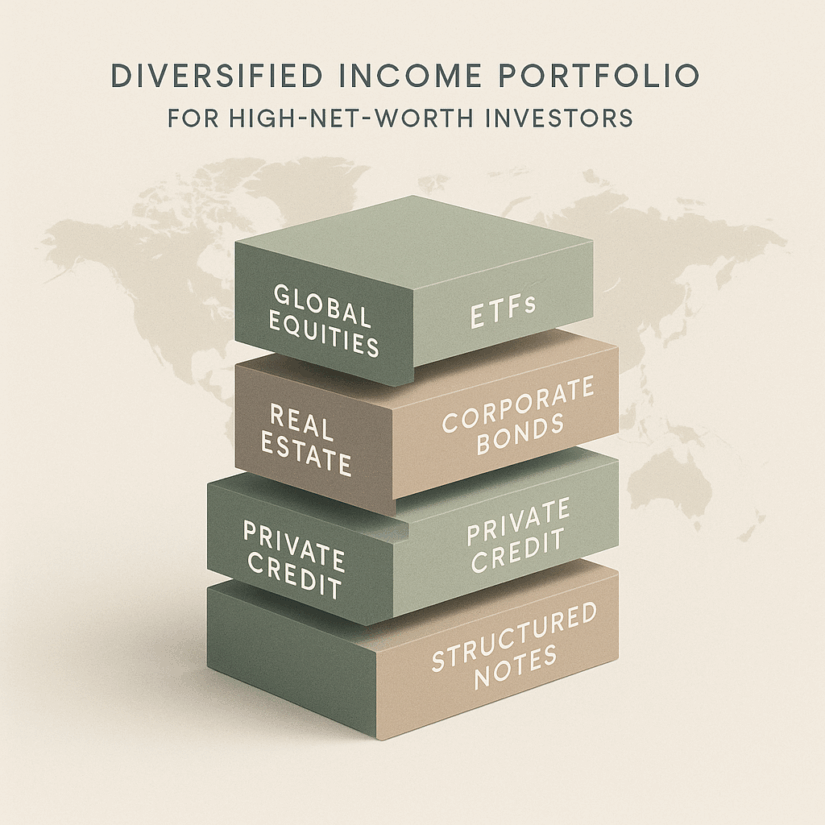

Investment Options

Crypto Updates 2026: Bitcoin Forecasts, New Laws, and IRS Reporting Rules

The biggest changes shaping the market this year include regulatory reforms, institutional inflows, and new tax rules, and these are the core crypto updates in