I often write on Quora.com, where I am the most viewed writer on financial matters, with over 438.2 million views in recent years.

In the answers below I focused on the following topics and issues:

- Do British expats pay any taxes on their overseas earnings?

- How can you invest as a digital nomad?

- How can you invest $500-$1,000 to earn more money?

- Do most expats retire?

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Some of the links and videos referred to might only be available on the original answers.

Source for all answers – Adam Fayed’s Quora page.

How can I invest as a digital nomad?

It is the same as every other expat but with caveats.

From a very practical point of view, what you need to do is:

- Fill out an online application form with a brokerage. That document will include questions on source of wealth, like where the money originates from.

- Give proof of address (usually a bank or utility statement) and ID (ID card or passport) for anti-money laundering requirements

- Fund the account

The issue is, many digital nomads don’t have things like a tax number overseas, which is asked for as part of the source of wealth requirements.

If you say you are living in Thailand or Malaysia, as an example they will ask for a tax identification number (TIN).

Most nomads don’t have this, and therefore make the mistake of focusing on investing back in their home country.

The issue is, this could be a mistake. Many tax authorities, including in Canada, Australia and beyond, are now cracking down on expats and nomads. They are demanding that expats “show intent” in some cases.

In practice this means giving up ties to your home country, such as cancelling the gym membership and other ties to your country of origin. We don’t know about the future, but this is likely to get worse.

After Covid-19, and with an aging population, governments need revenue. Those living overseas could become easy targets.

Therefore, it is better to ensure you deal with a brokerage company who understands nomads, and makes sure everything is legally correct, and makes sense from a long-term investing point of view.

Beyond that, just like for regular expats, it is important to have portability. You will most likely move around, so any investments need to move with you.

So, just as you should avoid investing in your home country, it isn’t a good idea to focus on investing locally.

Expat-focused portable accounts, typically held in a country which isn’t your current country of residency or citizenship, are usually much more convenient to move around as a nomad.

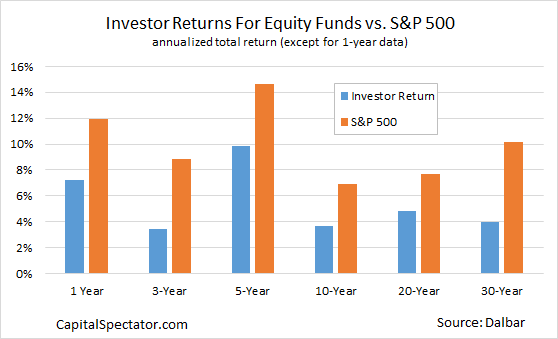

Beyond that I would make sure you get guidance or advice where appropriate, as most people end up with sub-optimal returns like this:

Many younger nomads have told me that they bought crypto high, and panic sold low, and have done the same with other assets.

It is important to have a good risk-adjusted asset strategy, and not just focus completely on getting the highest possible return, otherwise hidden risks increase and you can end up losing.

Take too little risk and you will lose for sure, due to inflation. Take too much and you might lose as well.

There are sensible ways to reduce risks and ensure returns are likely to be good.

Do British expats pay any taxes on their overseas earnings?

Usually not, but the devil is in the detail.

If you are British, and living overseas, whether you pay taxes depends on if you are a tax-resident in the UK, and where the money is coming from.

Assuming you don’t have too many “ties” to the UK, and don’t spend too many days locally, you don’t usually have to pay taxes on overseas earnings.

I would check out documents online from HMRC and the government, such as this one below, and get formal tax advice if needed.

I would avoid putting too much money into UK properties whilst overseas, because this can create tax obligations.

There are more tax-efficient routes for expat investing than sending money home to buy property.

Good morning sir, I have read and watched all videos you posted about investing rather than spending. I am Nigerian and I really do want to escape the harsh economic realities in the country. Stocks are crumbling, foreign investors are leaving and money is worth nothing except one earns in dollar. How can I invest between 500- 1000 dollars in the US to get a long term returns. I really need directive and referrals

Thanks for your question.

However, it is too big a question to answer here.

I would carry on reading my content for free, as we do have investment minimums, so unfortunately can’t accept the majority of people who reach out to us.

The only points I would make is:

- Stocks aren’t crumbling. This is a normal correction of 10%-20%

- I don’t say don’t spend obviously, merely overspending is one of the biggest issues many people face. Most self-made wealthy people are good at delaying gratification

- I would seek to use the rise of the online world to earn more. Location doesn’t matter as much anymore when it comes to earnings, if you know how to do it.

- Keep learning and reading from various sources, and then implement.

There are many answers which show how you can invest in the US stock markets globally.

Do most expats retire?

If expats work for a company they are more likely to be retired.

Let’s say you work for BP, or Shell, UK. You can’t easily be forced to quit due to age discrimination laws.

In many expat locations, you are most likely a contractor working for the same company. This means you are working without those same rights as back home, and also lack a pension for the most part.

So, you trade security, for adventure and often a highly hourly rate on a rig somewhere.

I have used oil&gas as one example, but the same “deal” exists in some other industries.

School teachers back home often get a good pension and are difficult to fire. International school teachers can save and invest much more, on average, than their peers back home, but they don’t have the same security.

The exception is business owners, who can’t be forcibly retired, and those who move (and stay) in just one location, and therefore receive local benefits.

This is why it is important for expats to actually prepare. What people do back home, which is often to leave it late, works more easily than overseas, due to the acquired benefits from social security/national insurance.