I often write on Quora.com, where I am the most viewed writer on financial matters, with over 466.9 million views in recent years.

In the answers below I focused on the following topics and issues:

- What are the risks of investing in the stock market?

- Why is gold not rising dramatically in value with inflation averaging 10%?

- Would you rather be Jeff Bezos or Bill Gates?

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Some of the links and videos referred to might only be available on the original answers.

Source for all answers – Adam Fayed’s Quora page.

What are the risks of investing in the stock market? How was it going?

The biggest risks are:

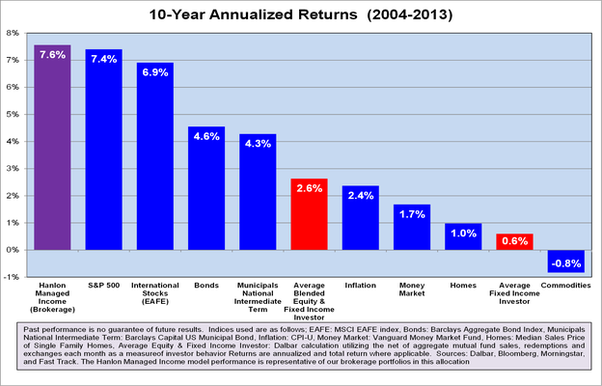

- Yourself. Emotions cause people to sell and buy at irrational times, which gives rise to results like this:

2. Individual company risk. Buying individual stocks is much riskier than the whole market via ETFs. Individual stocks can fall due to a multitude of reasons including:

- The founder dies and the company isn’t as good without them

- There is a regulatory crackdown like what happened with the banks after 2008, or firms dealing with Russia this year

- Over-performance isn’t maintained, and a reversion to the mean is experienced

- The competition gets better, or new technologies render your product or service useless.

There are many others I could list as well. All of these risks can be eliminated if you invest in a diversified group of stocks, such as via index funds or ETFs.

3. With investing in say index funds or ETFs, you don’t have the risks mentioned in the second point, but you still have market risk.

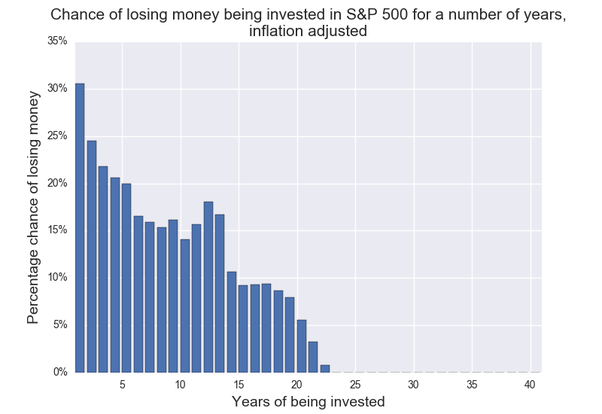

In other words, the market is down, like it is this year. That risk can be managed by being long-tern orientated:

You can further decrease your risks by investing monthly into the market to buy at average prices, reinvest dividends and have some assets in non-stock market instruments such as bonds or REITs.

Risks for the average long-term investor is no higher now than they were last year, or five years ago.

The only new long-term risk which exists is depopulation. For the first time in human history, and certainly in our lifetimes, the human population will likely fall within a generation or two, and not due to starvation.

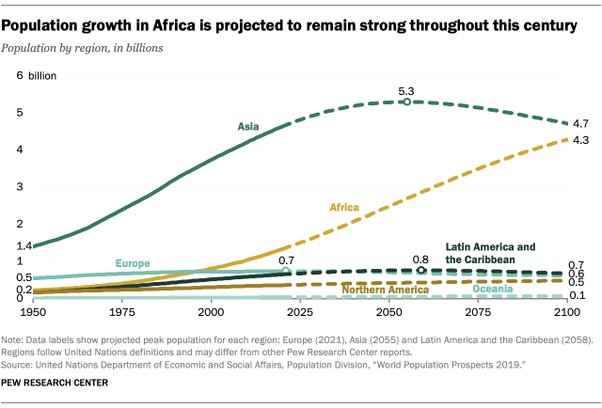

Only Africa and one or two other regions will have increasing populations:

Many countries, such as Japan, South Korea, China, Italy and beyond will see populations fall by over 40%, unless immigration does the heavy lifting.

That is a huge risk, but also an opportunity, as there will be a need for countries to invest in new technologies the further on we get into this century.

Why is gold not rising dramatically in value with inflation averaging 10% monthly?

- Inflation is averaging 10% yearly, not monthly.

- It is a misconception that gold is an inflation hedge.

For the second point, it is true that gold has held its value against inflation the ultra long term.

That is more of a negative, rather than a positive, as it means it has underperformed some other assets:

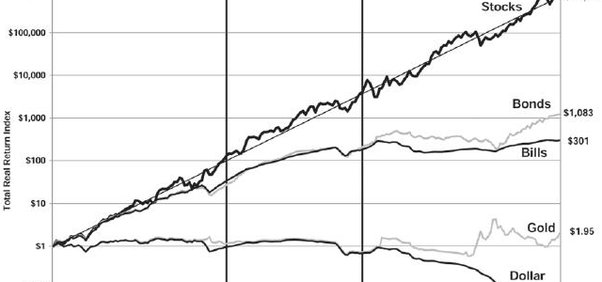

$1 invested in gold for hundreds of years has barely moved adjusted for inflation. As the graph below shows, which looks at the ultra long-term performance of asset classes, gold’s keeping pace and slightly beating inflation isn’t as good as many other asset classes.

The fact that gold has kept pace with inflation over long periods of time, doesn’t mean it will every year or decade.

There have been numerous times periods when inflation has skyrocketed, and gold has gone down or stayed stable.

There have been other time periods, such as 2000–2008, when gold has done well despite low inflation in much of the world.

When people speak about this, it reminds me when it is said that gold is a recession hedge, or a hedge against loads of other things. Usually it isn’t.

Gold is, however, a partly non-correlated asset. In human terms that means it doesn’t always go down when stocks are down, even though sometimes both go down at the same time, like during the 2008 and 2020 market crashes.

That is one reason why gold is in some professional portfolios, as a small competent of the total amount, as a wider asset allocation strategy.

The strong USD is also constraining gold’s price. In Euros or Pounds it has done OK in the last year, even if not great.

Would you rather be Jeff Bezos or Bill Gates?

Neither.

It is better to want to be yourself, rather than somebody else.

If you pointed a gun to my head, and forced me to pick one, I would say Gates. He is older than Bezos, but only marginally so.

He is also a higher “class” of billionaire, for lack a better term.

What do I mean by that?

There are broadly four kinds of billionaires

- Those who have private companies. These are on the lower end of the ladder. A private company owner who is a billionaire, such as Trump, can’t easily raise as much money as somebody who has a public company listed on the stock market

- Those who have put their company onto the stock market, and did an IPO. So, Microsoft did this in 1986, and Amazon in 1997. At this stage, the founder’s wealth is often tied completely to the company.

- Then there are those who gradually diversify away form their initial business. It is difficult to do this too quickly, otherwise the market might panic. Gates had close to 100% of his net worth in Microsoft in the 1990s. The same with Bezos and Amazon. The difference is, Gates has a much lower percentage of his net worth in his original company, and has a family office managing most of his money:

Only about 15% of his net worth is now in Microsoft, unlike Bezos, who has a much larger chunk of his net worth in Amazon.

He is gradually selling off parts of his Amazon stock every year, to diversify, but his wealth is much more concentrated.

- At the top of this so-called “hierarchy” is royalty. They might not always have as much wealth as individual billionaires on paper, but some have the wealth of an entire country behind them.

So, basically, Gates’ wealth is more secure than Bezos.

Gates wouldn’t be affected that much if Microsoft’s shares tanked.