I often write on Quora.com, where I am the most viewed writer on financial matters, with over 566.6 million views in recent years.

In the answers below I focused on the following topics and issues:

- Will the Federal Reserve raise interest rates in 2023? What would be a good investment if they do?

- What are some good reasons to invest in exchange-traded funds (ETFs)? What are some potential risks associated with investing in ETFs?

- What businesses are best for a recession?

- Can lawyers be good entrepreneurs?

- How long would 10 million dollars last you?

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Some of the links and videos referred to might only be available on the original answers.

Will the Federal Reserve raise interest rates in 2023? What would be a good investment if they do?

The Federal Reserve, and other major central banks, have increased interest rates.

This has bought about opportunities and risks.

Government and corporate bonds got hit hard last year.

In fact, many stock markets, like the Dow Jones and UK FTSE 100, did far better than the traditional “safe heaven” play.

That is because as interest rates increase, it is bad news for existing bond holders.

If interest rates peak and then fall, that will be likely be good for bonds.

Already we can see A-rated corporate bonds, provided by large companies, paying 6%-8% a year.

Stocks have had a good start to the year too, with some European stock markets hitting record highs.

As valuations look depressed compared to before, especially in non-US stock markets where the strong dollar has weighed on valuations, there is, as always, opportunities for the long-term investor.

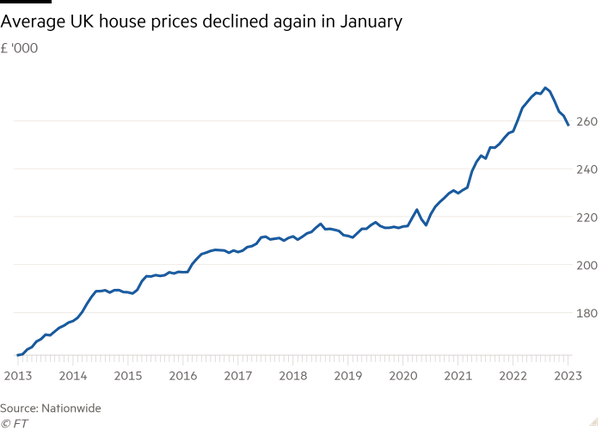

Real estate is the big one. Housing did better than stocks and bonds in 2022 until late last year.

This year, real estate looks riskier than before.

Already, prices are falling in the UK, Hong Kong, South Korea and beyond.

As this graph from the FT shows, prices have been falling consistently for months now:

Commercial real estate might fall more as companies have to sell stock.

That brings about opportunities.

Investments focused on distressed real estate are likely to do well, because good deals can be found.

What never changes is there are always opportunities out there in the world.

Can lawyers be good entrepreneurs?

It does happen.

I have one or two friends and clients who have started their own business.

It isn’t common, though, as some people below have mentioned.

The main reasons are:

- Lawyers tend to be risk-adverse, which is the opposite of what most entrepreneurs are.

- There is an “easy” route to starting your own company. That is setting up a legal practice. There is also the self-employed consultant route where they can advise people on market entry and many other things

- A good entrepreneur needs to pivot and adapt quickly in some situations.

It is often a difference of mentality.

Take the issue of getting fined and breaking rules.

Travis Cordell Kalanick started Uber. Were they legally compliant in many countries? No.

But Travis, as Mark Cuban and others who were offered it as an early invested have stated, wanted to “seek permission rather than ask for permission”.

He wanted to make Uber so big that even if they received fines, the horse has bolted, which would force regulators to “allow” Uber to be completely compliant.

The same is true for digital currencies, whatever one may think about them.

They reached a certain size where it became impossible to ignore them, and therefore regulating them was easier for most governments.

We also see it with the big banks. They get fined every year.

It is cheaper for them to pay fines rather than change their processes, even though they don’t admit that in public.

The legal or compliance mentality is “better safe than sorry”, which wouldn’t have allowed for an Uber.

Let’s put this another way. Most entrepreneurs wouldn’t make good lawyers, even if they retained.

It isn’t just lawyers though. Most public servants and other people who are encouraged to be cautious, need to adapt quickly when running a business.

This is especially the case if it gets bigger than just a lifestyle business.

What businesses are best for a recession?

Any business that can maintain good profit margins.

Some are obvious like consumer goods.

We still need toilet paper, food and tooth paste in a recession.

Another example is healthcare. Some people still get sick in a recession.

Some are less obvious. Believe it or not, luxury goods companies can stay strong in a recession.

People still like to do those one-off luxury things, even in a recession.

It depends how deep the recession is though, and if it is global or regional.

A recession is merely measured as two successive quarters of negative GDP growth in many countries.

So, the difference between an economy contracting by 0.1% and growing by 0.1%, isn’t huge.

Unless a recession is very bad, luxury companies tend to do OK.

Oil & gas can also maintain margins sometimes, but the price of oil often falls when the global economy is falling.

In terms of global trends and recessions, remember that most of the firms in the UK FTSE 100 are global. The same with the S&P500.

Therefore, it shouldn’t be a surprise that the UK stock market can hit a record high (as it did a few days ago), even if the UK economy isn’t doing great.

There is a wider point here. Seldom is the whole world struggling.

This year, it is likely there will be real global GDP growth of 1%-2.5%.

So, even if 30%-35% of countries go into recession, some parts of the world are doing well.

That is another reason why luxury goods tends to do surprisingly well in a recession.

There are always some people doing well in a recession-hit country.

A good case in point is when Greece and others countries hit a severe recession after 2008, and sales of luxury houses went through the roof, as overseas buyers saw an opportunity.

What are some good reasons to invest in exchange-traded funds (ETFs)? What are some potential risks associated with investing in ETFs?

The positives are

- ETFs are a low-cost way of gaining access to thousands of firms, which is safer than buying individual bonds and stocks.

- They are liquid which means they can be sold quickly.

- You should do well if you buy the right ones and hold them long-term.

- There is little to no risk of large ETF companies going bust. The chance of Vanguard or BlackRock going bust is less likely than a highly leveraged bank. BlackRock has 10 trillion assets under management. To give you some indication of how much that is, HSBC has about 2.9 trillion and, the largest bank in the world has 5.5 trillion.

The negatives are

- That very liquidity is also a negative. Funds take 3–4 days to sell. People are locked into retirement funds for decades in some cases. Many studies show that people are more likely to panic sell with ETFs compared to investment funds.

- Following on from the last point, the ‘grandfather of passive investing’, John Bogle, who founded Vanguard, warned against them for that reason. In other words, he didn’t think they are bad if people buy and hold. He just cautioned against trading them.

Here is the article where Bogle reports why he is sceptical about how ETFs are used rather than the ETFs themselves.

- Many niche ETFs are now linked to specific industries, like AI ETFs, or country-specific ones in small markets. The point in passive investing is that it gives the ‘no nothing’ investor, who doesn’t have an advisor, a chance to do well if they buy and hold. If you start trading them and picking particular narrow areas to invest in, you likely won’t do well long term.

- From a moral point of view, a small percentage of people might have a problem supporting firms like BlackRock, which already own so much of investable assets.

The biggest negative by far is investor behaviour.

We saw evidence for this between 2020 and now. During the market crash in 2020, many people panic sell.

Then the recovery came, and plenty was bought in areas like the ARK ETF.

2022 came, and suddenly people became fearful again after the Ukraine-Russia war.

The point with ETF and index funds is to buy and forget, not buy and trade.

So, the most significant risk is yourself.

How long would 10 million dollars last you?

Like most sensible people, it would last me a lifetime.

This is because I wouldn’t spend it on day one.

I would invest it and live from the dividends, or just accumulate it for further gains – in order to have more for a rainy day.

A cautious strategy could yield $300,000 per year, adjusted for inflation, or slightly more.

It won’t last most people if:

- You take too much investment risk and it doesn’t pay off

- The money is left in cash and gradualy gets eroded by currency devaluations and inflation.

- There are unexpected events such as multiple divorces

- You spend it all, and think ‘how much can my money buy me’, as opposed to ‘how much could my money earn me’, and buy items with the dividends or interest.

- You donate money to friends, family or charity, rather than investing it and giving some of the dividends.

Think about it.

Imagine you are 30 or 40.

You have 50 years to live.

The money is left behind your sofa.

That is 18,000 days.

That is only $500 even if we don’t count inflation.

With money in the bank losing to inflation, that might be $100-$250 a day adjusted for inflation.

Anybody can spend that.

If you spend or give half of it away in the first year, you can halve those figures ($5m to last you a lifetime).

That is $50-$125 a day, assuming inflation keeps running at higher levels than the bank gives in interest.

Therefore, it shouldn’t be a surprise to know how common it is to see former millionaires in the world.

Too many focus on how much millions can buy now, and not decades in the future.