I often write on Quora.com, where I am the most viewed writer on financial matters, with over 621.7 million views in recent years.

In the answers below I focused on the following topics and issues:

- What are some income producing assets that I can use to build wealth?

- What is a booming business in the future?

- Are insurance companies safer than banks?

- What are some reasons why people might not invest in commodities?

- Will inflation continue to grow in 2023?

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Some of the links and videos referred to might only be available on the original answer

What are some income producing assets that I can use to build wealth?

Income isn’t a free lunch.

What have been some of the best-performing firms on the stock market?

Amazon and Warren Buffett’s company Berkshire Hathaway. They don’t pay dividends.

That allowed them to grow more quickly than paying out income to shareholders.

The same is true for your own business. If you take out more income, you have less to reinvest, which in turn will allow you to earn more later on.

Here is a good graph from the Motley Fool, which shows how correlated the S&P500 and Vanguard high dividend ETF has been:

Another way of looking at the graph would be to say that it would have been irrelevant if a retiree had invested in the S&P500 and sold some it every year, compared to living off the interest from the dividend fund.

In fact, they would have had slightly more money had they sold off some of the S&P500 units.

With that being said, eventually, you will probably need income.

The best ways of doing that are

- Having an income-producing business and reinvesting into income-producing, tax-efficient assets

- Investing in accumulation assets like non-income (or low-income) paying ETFs, and only optimizing for income later on.

- Even if you don’t need the income, focusing on diversification. So, some assets are held in accumulation and some into income-paying investments

- Using leverage to your advantage. For example, leveraging through buy-to-let when you are young, and then using the income when you are retired. In many countries, however, this no longer works due to tax laws. In the UK, for instance, this worked in the 90s and 2000s, but no is mainly dead due to tax changes and the lack of 100% mortgages.

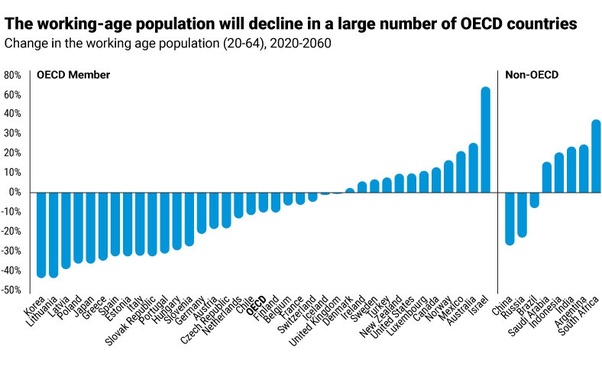

What is a booming business in the future?

We are seeing something right now which has never happened before.

There have been many times of falling populations, historically, due to feminine.

Right now, many countries are seeing falling populations in decent economic times.

People are having fewer kids.

South Korea, Japan, China and many other countries are seeing falling populations.

Much of Europe and the US would have the same problem if it wasn’t for migration

In comparison, some countries are seeing booming populations.

The graph below doesn’t fully show how fast Nigeria’s population could increase.

Given these sets of trends, the following businesses might do well:

- AI and automation

- Healthcare and any services for older people

- Migration and cross border services. Right now, only 3% of people live outside of their home country. In the future, more people surely will, as countries compete for machines and human labour alike. Cross-border lawyer, financial and consultancy services is more complicated than in a single country. Visa-related firms might also benefit.

- Old people’s homes.

- Existing business that adapt to an aging population. For instance, education services for the elderly.

Of course, though, nobody can predict the future.

If somebody would have predicted in the 1970s that several countries would have falling populations in 2023, almost everybody would have assumed that starvation would be the likely cause

Are insurance companies safer than banks?

It depends what kinds of insurance companies.

If an insurance company is insuring buildings, cars and other things against loss or fire, they can easily go out of business.

Ultimately, it can take a few black swan events for them to go bust.

In comparison, some insurance companies are really just investment companies.

They are more like life assurance, in terms that they make money from clients assets, and wrap it in insurance for tax and estate planning benefits.

Many offer pension plans as well.

These kinds of companies are less likely to go bust than banks.

The reason is:

- They don’t use as much debts, whereas the banks leverage with clients money. We saw during the 2008 Financial Crisis, and the recent “mini crisis” in Europe and the US, that the banking system is vulnerable to runs. We have also seen large bank runs in the past

- They often have exit fees. An insurance company that has some products which have exit fees, or it is impossible to get out (such as pensions), have more “sticky” business

- Like investment platforms, they make a lot of residential/recurrent income

- The medium-sized insurance companies are less likely to gamble or speculate, compared to larger banks and “too big to fail” insurance companies like AIA who got into trouble in 2008.

What is more, when it comes to death and estate planning, insurance companies can be some of the quickest to pay out family members.

I was at a convention recently where a speaker, who mainly helps Indian expats overseas, was talking about a recent case.

One of his clients died two years ago. In India, it is still going through probate, whereas the insurance company changed the ownership to the beneficiaries almost instantly.

So, it depends on many things, but insurance companies and investment platforms are more secure than plenty of banks out there.

Ultimately, if any company (insurance company, platform or bank) operates a no or low debt model, they are less risky.

EuroPacific Bank in Puerto operated a zero debt policy. They were closed down, but customers likely won’t lose money for obvious reasons – there is capital and no debt, so the customers can move to another institution.

That also meant that regulators could close them down without worrying about contagion or people losing money.

Few banks operate like that.

In the US, apparently deposits at insurance companies aren’t covered by FDIC, which should tell you something.

Many countries have similar policies.

What are some reasons why people might not invest in commodities?

The biggest single one is that commodities perform worse than stocks, and even bonds, long-term, with higher levels of volatility.

Usually more volatile assets perform better, as per the Nasdaq’s relative over performance against other stock markets long-term.

Industrial metals are also more volatile than Gold as well.

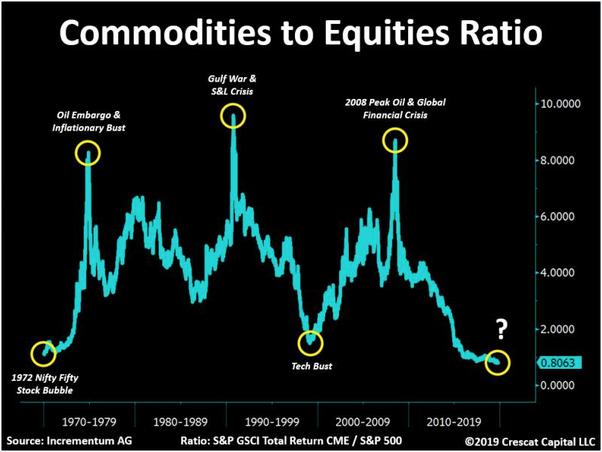

Some see the graph below, produced by IBKR, as proof that commodities are cheap and due a bounce:

Commodities might be cheap and potentially due for a bounce, but another way of looking at it is they don’t tend to do that well long-term.

What is more, during economic downturns such as 2008 and 2020, they tend to fall more than stocks.

Oil was at $144 before 2008, and fell to around $30. Similar things happened to many other industrial commodities.

Commodities ETFs also don’t pay dividends.

Against that commodities have the following advantages:

- They occasionally outperform. They sometimes outperform during moments when stocks are underperforming, such as in 2000–2007.

- Commodities can, therefore, be held as a small hedge and way of diversifying

- If you go beyond ETFs into assets such as hedge funds, you can sometimes overcome the negatives associated with commodities, such as a lack of dividend payments.

- Firms within the commodity space can be innovative and some pay high dividends.

Will inflation continue to grow in 2023?

We are almost mid-way through 2023 now.

It is clear inflation rates are falling.

US inflation is below 5%, with Spain and some others seeing rates closer to 3%.

What is more interesting is according to truflation.com, which looks at real-time inflation data, inflation is now below 3%.

Longer-term, a bigger likelihood is low inflation and even deflation.

Remember we are seeing two big deflationary forces:

- An aging population, and even a falling one in some countries. Remember, Japan struggled with deflation for decades, and the recent pick up in inflation there is likely to be transitory.

- AI and the tech revolution. Some of this is not picked up in official inflation data. Going to the cinema is more expensive than it used to be, as is going to bars and restaurants……yet the option to watch Netflix and have a drink means some people are spending less on entertainment than in the 1990s or 2000s. Ditto commuting costs. Some people have reduced it down to zero.