I often write on Quora.com, where I am the most viewed writer on financial matters, with over 488.2 million views in recent years.

In the answers below I focused on the following topics and issues:

- What are the money rules for financial success?

- Can you invest in the US stock market from China?

- Is it possible to become a millionaire without debt?

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Some of the links and videos referred to might only be available on the original answers.

Source for all answers – Adam Fayed’s Quora page.

What are the money rules for financial success?

There can be no definitive rules, that are easy to implement, otherwise everybody would do it.

However, there are some commonalities.

Let’s separate being a salaried worker, to running your own business.

If you are salaried, the key things are:

- Invest from a young age to take advantage of compounding. Don’t save only, as that gets eroded due to inflation

- Keep costs down. Now sure, it is natural to spend more as you earn more. We can’t live as students if we have kids and are 35. However, lifestyle inflation can eat away at any pay rises. A good rule of thumb is to invest 50% of any pay rise.

- Invest in educating yourself. Those who put in the time and work to do that, can get rewarded. An example is investing, communication and negotiation skills. Most of all, if you become one of the best at your job, you will more likely always have one. If you are one of the best teachers in your hometown, you are less likely to lose your job compared to being average.

- Having a bit of luck is essential. Most of the everyday millionaires you see kept things simple. They invested for decades, spent wisely etc. Yet they also had their health for decades as well.

Of starting your own business, the keys are:

- Having at least some natural talent in the area. Natural talent is over-rated, but having at least some is important. If you have that, it is easier to get good at a job in an area, and then quitting that job and starting your own business is easier than just starting from fresh.

- Work really hard, especially during the early stages when you are trying to establish yourself

- Work in a smart and focused way. If you work really hard, but try to be too broad, you are less likely to succeed. If, on the other hand, you solve a really specific problem people have, you have more chances of success.

- Take many calculated risks. Most people are afraid to fail, take risks and be seen as being too “abnormal”. Risk-taking in a sensible way is one way to actually work smart.

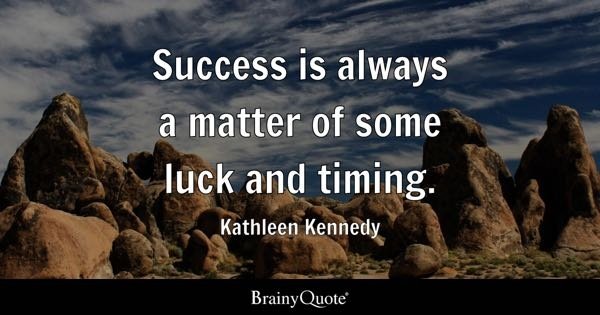

- You need a slice of luck. A bigger slice than if you are a salaried employee. Now sure, you do make your own luck as well, but randomness plays a role in business success. Even people like Gates and Buffett have admitted that they wouldn’t have been rich hundreds of years ago. The quote below from brainy quotes says it all:

There are some commonalities for both, such as avoiding toxic people.

Can you invest in the US stock market from China?

You absolutely can, but it comes with some added difficulties.

As always, you need to:

- Find an advisor or online broker who can accept Chinese residents

- Provide your proof of ID and address. This is due to anti-money laundering (AML requirements)

- Fill out an application form

However, with China, you have an added difficulty – getting money out of China.

For Chinese citizens, it is theoretically possible to move $50,000 a year out of China. In recent years, bank have made it harder for many people to do that.

I have ran out of the number of people who have approached me, after being denied to transfer money (or the money mysteriously comes back to the account) perfectly legally and under the limit.

It seems that the state-owned banks are worried about the depreciation of the RMB against the USD, or have another reason for doing this.

For non-Chinese people living in China (expats), it is theoretically possible to send any amount of money out of China.

In reality it isn’t easy because:

- The account you are sending to should be in your own name, so a bank account. Most investment accounts aren’t in your name. You need to provide a reference number in the transfer, so the money can be assigned to your account. Brokerages don’t create individual bank accounts because you aren’t opening a bank account. Therefore, even if you can make use of this rule, it is first needed to transfer money overseas, and then to the investment account.

- Like many rules in China, it isn’t easy to do it in practice. When I lived in China, I went to the bank, and I could speak conversational Chinese. They insisted that $500 a day was the limit. I showed them some evidence to the contrary, in the form of a Chinese-language article. A few calls were made and they relented after seeing some documents……took about four hours. Some other people I have helped tried the method and it didn’t work.

Therefore, you often need to find solutions such as:

- China-specialized currency companies

- Get a visa or MasterCard in China

- Any other solution a good advisor can suggest

So, it is doable, just tricky sometimes.

Is it possible to become a millionaire without debt?

It is, but most people actually indirectly get wealthy through debt.

What do I mean by that? Many “everyday millionaires” might think they haven’t got into debt. Maybe they haven’t used credit cards and business debts.

Yet most have made more money from getting a mortgage that buying the property in cash.

The majority have also directly or indirectly (through pensions) invested into the stock market. Those companies use debt to grow.

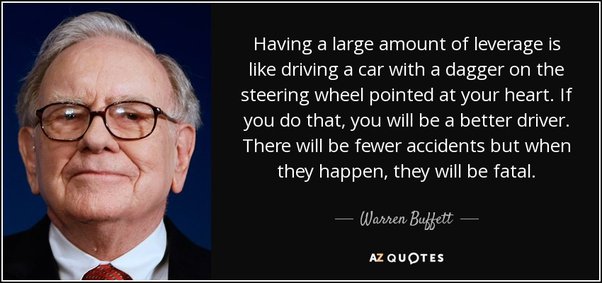

Debt is a double-edged sword. Leverage increases the gains, but also the risk. Charlie Munger once said there are three ways smart people go broke – liquor, ladies and leverage!

The dangerous thing about leverage is that it works most of the time. Therefore, you might start out sensibly. Once it works, why not go for more and more?

You also need to be right more often as per this quote:

I know several people who went broke during the 2008 financial crisis, as they needed to sell properties to pay back the loans that were called in.

Somebody who would have leveraged out on the indexes like the S&P500 would have also made a fortune in the long-term, but plenty took leverage took far.

So, use debt sensibly. It can be your making, or breaking. You can get it right ninety-nine times out of a hundred, and that one time you fail can be your undoing.

What is true is that most people who get wealthy use different types of leverage, which isn’t just financial leverage.

What kinds of leverage am I referring to?

- Financial leverage/debt. We have already discussed that

- Leveraging people. Employing others to do tasks for you

- Leveraging time. Compound investing returns is a great example of this

- Leveraging technology. You can’t be in over a hundred countries at once with the old model. You can be if you are online.

Basically, if you just invest in yourself and gain high skills, it isn’t easy to get wealthy, unless you save really hard.

Even then, inflation might erode the capital. Therefore, investing in time and other kinds of leverage can be very effective.