In this volatile economic environment, one thing is certain: inflation continues to threaten your hard-earned wealth.

With increasing prices and shrinking purchasing power, astute investors are using time-tested inflation-hedging methods to preserve their financial well-being.

If you are looking to invest as an expat or high-net-worth individual, which is what I specialize in, you can email me (advice@adamfayed.com) or WhatsApp (+44-7393-450-837).

This includes if you are looking for a second opinion or alternative investments.

Some facts might change from the time of writing. Nothing written here is financial, legal, tax, or any kind of individual advice or a solicitation to invest.

What precisely are good inflation hedging strategies in 2025? Do the assets you consider for inflation hedges actually give you protection when you need it most?

Let us discover how best to protect your wealth from the havoc of inflation.

Inflation Hedging Meaning

Consider hedging as insuring your investment against inflation. You would never drive a car without auto insurance or purchase a home without homeowner’s insurance.

Just like that, why invest without inflation protection? Without hedging, your portfolio can be exposed to catastrophic risks.

In layman’s terms, hedging against inflation is investing in such a way that your money is safer in periods of higher inflation. It’s definitely not about removing the risk entirely, which surely cannot be done.

Instead, it is about protecting your wealth as much as possible from the harmful impact of inflation.

Hedging is similar to putting on a seatbelt when you drive.

It won’t stop market fluctuations, but it will cushion the blow when turbulence comes.

This method enables you to continue pursuing your investment goals with more assurance during times of economic uncertainty.

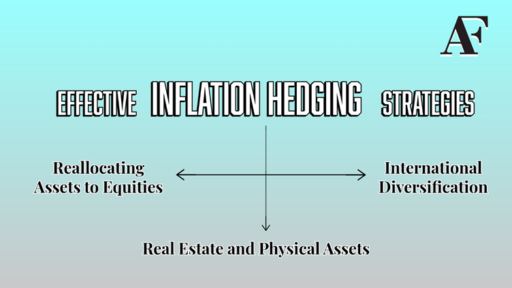

Effective Inflation Hedging Strategies

Ready to safeguard your portfolio? Let’s discuss the ultimate hedging strategies against inflation in today’s market.

Reallocating Assets to Equities

During periods of inflation, bonds usually lag behind as climbing interest rates and bring down the values of outstanding fixed-rate obligations.

Equities usually perform well, however, as companies can raise prices with respect to inflation and still register decent profit margins and real returns.

Consider these equity-based strategies:

- Traditional 60/40 portfolio:

This traditional portfolio allocation offers conservative inflation protection but will lag behind an all-equity portfolio in the long run.

- Preferred stocks:

These hybrid investment vehicles pay higher interest than most bonds but may realize less price deterioration during inflation periods.

- Utility stocks:

They have comparatively stable price trends over economic cycles and pay constant dividend income to neutralize the effect of inflation.

International Diversification

Did you know that different economies experience varying inflation rates that need not be based on local conditions? This offers a perfect chance for smart diversification.

Adding foreign stocks and bonds to your portfolio provides inflation protection within one country without sacrificing the potential for growth.

Italy, Australia, South Korea, etc., tend to be independent of U.S. markets and are good economic cycle hedges at home.

The silver lining?

Exchange-traded funds (ETFs) and mutual funds now provide affordable and hassle-free ways of securing international diversification, without the hassle of buying individual foreign stocks.

Real Estate and Physical Assets

When inflation hits, physical assets usually do well.

Why? Because physical property has intrinsic value that tends to rise with increasing prices.

Real estate is an especially good inflation hedge for several reasons:

- Property prices often match or surpass inflation rates

- Rental income usually rises during inflationary times

- Real assets offer both capital appreciation and income growth

For a majority of investors, real estate investment trusts (REITs) happen to be the most convenient method.

It is because they provide access to this inflation-resistant asset class without the hassle of owning property directly.

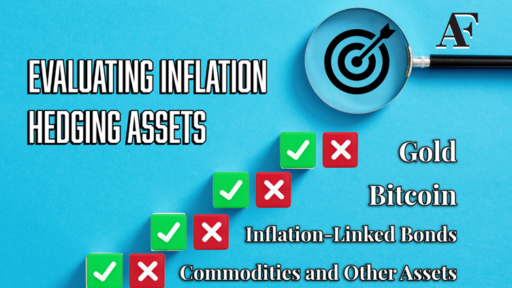

Evaluating Inflation Hedging Assets

Not all inflation hedges are created equal. Here’s an evaluation of some of the commonly known assets known to hedge against inflation:

Gold: An Inconsistent Inflation Hedge

Gold has always been considered a better hedge against inflation because it is rare and precious by the mere fact of existence. Gold can neither be printed nor devalued by powers like central banks, making it theoretically an excellent store of value in economic calamity.

But evidence has a more complex tale to tell.

Studies by the CFA Institute indicate a minimal correlation between inflation fluctuations and gold prices. As per them, gold – inflation correlation coefficient ranges from -0.004 to 0.162. This implies that gold does not necessarily have to move in tandem with inflation as it is commonly believed.

Goldman Sachs’ wealth management division has categorized gold among the “least effective” long-term hedges against inflation.

Although gold saw considerable returns of 27% in one recent year, its year-end 2024 price of $2,625 an ounce had only increased 3.6% per year on average from its price in 1980.

Simultaneously, the S&P 500 increased 11.7% compounded annually, which is significantly greater than gold.

Inflation-Linked Bonds

Inflation-linked bonds, like Treasury Inflation-Protected Securities (TIPS), are specifically created to hedge against inflation. They have been around since the 1980s and are appropriate if bought at issuance and held to maturity.

Even so, they can vary sharply in price over their term based on shifts in market interest rates and inflation expectations.

This accounts for their somewhat dismal recent performance, catching up with the adverse effect of rising interest rates relative to the favorable effect of inflation accrual.

In the long term, inflation-indexed bonds have outperformed inflation, producing an inflation-adjusted 2.3% annual return in the US market.

On these grounds, they deserve consideration as part of a long-term strategy to hedge inflation.

Bitcoin: An Unproven Hedge

Bitcoin has more and more been marketed as an inflation hedge because of its fixed supply and lack of dependency on central banking policy.

Empirical support for this comes, in part, from new studies, which identify that “bitcoin returns increase quite a bit in response to a positive inflationary shock.”

Regardless, studies point out the following:

- Bitcoin’s inflation-hedging characteristic seems price index selection-dependent. It works in the case of CPI shocks but not core PCE shocks

- Its hedging quality is largely drawn from previous periods in the history of Bitcoin

- Its effectiveness may be waning as institutional demand grows

Financial organizations such as Goldman Sachs continue to doubt the efficiency of Bitcoin, grouping it with commodities as inferior inflation hedges compared to other asset classes.

Commodities and Other Assets

Other commodities, such as oil, metals, and vegetables & fruits, are also most frequently mentioned as inflation hedges. But they have had an uneven performance.

Goldman Sachs states that, since 2010 the total return of oil has been negative, and the commodity market has high variability across subsectors.

This variability renders commodities (as a whole asset class) less effective at hedging against inflation than most believe.

Goldman Sachs indicates that “Commodities and gold are the two least effective inflation hedges.”

Inflation Hedging for Long-Term Investors

For long-term investors looking for protection against inflation, a diversified approach is likely to outperform dependence on any single asset class.

The evidence suggests that over very long time horizons, good inflation protection arises from diversified exposure to equities, credit securities, and to a lesser extent, gold.

Equity Considerations

While equities are reasonably good in the long-run protection against inflation, valuation is paramount.

During 2000-2010, the S&P 500 produced a negative inflation-adjusted total return with the primary cause being the colossal valuation bubble in the early 1990s. Surprisingly, the equally weighted S&P 500 index performed much better during this period.

Hence, this points to the necessity of diversification in equity exposures.

The market now has the same problems of excessive concentration of tech stocks in market-cap-weighted indices. Investors constructing inflation-hedged portfolios might have to favor more diversified equity exposure with average valuations below the market-cap S&P 500.

Portfolio Construction

A successful inflation-hedging portfolio might consist of:

- Diversified equity exposure, possibly with an increased emphasis on value stocks and historically evident inflation-sheltering industries

- Selective inclusion of inflation-indexed bonds suitable to your time horizon

- International diversification regarding bonds and stocks

- Provisional allocations to real assets, like maybe REITs or other real property investments

- Provisional allocations to gold or other precious metals as a worst-case economic condition hedge

The best combination will be based on your own time horizon, risk tolerance, and overall financial objectives.

Nonetheless, diversification among a variety of inflation-hedged asset classes tends to have the strongest protection.

FAQs

Q. What is hedging in finance?

Hedging, in terms of finance, is a risk-reduction strategy utilized to cancel potential loss in investments by going for an inverse investment in a similar asset.

The method acts to reduce the effect of adverse price movement in the main investment, just like an insurance cover against financial loss.

Q. How do you hedge inflation?

To safeguard against inflation, portfolios may be invested in assets that naturally appreciate in value when prices rise, which generally include equities, property, and commodities.

Inflation-indexed bonds, such as Treasury Inflation-Protected Securities (TIPS), also work well since they modify their principal value according to inflation rates.

Q. Why is gold an inflation hedge?

Gold is considered an inflation hedge as it normally keeps its value even during times of inflation.

Investors consider gold as a hedge vehicle that keeps up purchasing power in case fiat currency loses purchasing power with inflation.

At least, its potential is relative and depends on conditions and temperament in the market.

Q. Is Bitcoin actually an inflation hedge?

Bitcoin has frequently been promoted as an inflation hedge due to its limited supply and independent nature from central bank policies.

It has been argued in some research that it can act as an inflation hedge, especially during some time periods.

However, its efficiency is questionable and seems to be context-dependent, with a lot of skepticism especially from the side of financial institutions which are cynical about its dependability in contrast to traditional assets.

Crypto is quite high risk and investors can lose all their money.

Q. What is the best hedge for inflation?

The best hedge against inflation is a portfolio that’s diversified and made up of equities, property, and inflation-indexed bonds.

By having a diversified portfolio of such assets, investors are able to have complete protection against the eroding effect of inflation in the long run.

Conclusion

As we find ourselves in the middle of the 2025 economic uncertainties, successful inflation hedging is still essential to maintaining long-term wealth.

While traditional holdings such as gold have been the blue chips of inflation protection for decades, the facts are different.

Diversified equity holdings seem to offer more inflation protection over the long term than gold or commodities. Inflation-indexed bonds provide explicit protection if they are held until maturity but may exhibit volatility in the meantime.

For the majority of investors, the best strategy is the combination of:

- Diversified equity exposure

- Tactical asset allocation to inflation-indexed bonds

- International diversification

- Judicious use of real assets

This multi-strategy solution offers inflation resilience with room for real growth over long horizons.

As inflation dynamics change, periodically re-examine your hedging strategy, rebalancing asset positions in order to adapt to evolving economic conditions and yet continue to commit to maintaining long-term purchasing power.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.