Bolivia does not tax most foreign-sourced income for residents under its territorial tax system. This means expats earning income abroad may legally pay 0% income tax in Bolivia, but the reality is more nuanced.

Residency rules, domestic income definitions, and compliance obligations all affect who truly benefits.

Misunderstanding these subtleties can lead to unintended tax exposure or compliance challenges.

Prefer listening over reading? This audio dives into the realities and risks of Bolivia’s so-called zero foreign income tax.

Key Takeaways:

- Bolivia taxes only domestic income; most foreign income for residents is legally exempt.

- Residency of 183 days or more is required to qualify for territorial tax benefits.

- Exceptions exist—income connected to Bolivian activities or assets may be taxable.

- Documentation and proper planning are critical to safely benefit from the 0% tax on foreign income.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions.

The information in this article is for general guidance only. It does not constitute financial, legal, or tax advice, and is not a recommendation or solicitation to invest. Some facts may have changed since the time of writing.

Why is the claim of zero foreign income tax in Bolivia misleading?

Many assume moving to Bolivia automatically eliminates all tax obligations. In reality, territorial taxation operates within a legal framework with conditions, reporting requirements, and potential economic risks.

The headline claim is accurate in principle, but the practical implications reveal a more complex story.

For example, some expats might think that simply opening a bank account in Bolivia and moving money from abroad guarantees tax-free status.

In practice, authorities may require proof of residency, days physically spent in the country, and evidence that income truly originates outside Bolivia.

Without such documentation, even overseas income could be questioned.

How does Bolivia’s territorial tax system work for foreign income?

Bolivia only taxes income sourced within its borders; foreign income is generally exempt for residents.

- Residency rules: Expats become tax residents after spending 183 days in a calendar year in Bolivia. Once resident, territorial taxation applies.

- Domestic income taxation: Personal income inside Bolivia is subject to tax of 13%, as per PwC.

- Foreign income: Income earned abroad—such as salaries, consulting, or investment returns—is typically exempt. However, expats must maintain documentation proving foreign-source income.

- Reporting: Bolivia does not have extensive reporting requirements for foreign income, but record-keeping is recommended. Simple steps like maintaining invoices, bank statements, and contracts can protect expats from potential disputes.

- Historical context: Bolivia adopted territorial taxation decades ago to encourage foreign investment and reduce administrative burden. Unlike worldwide taxation systems, territorial rules simplify compliance for expats, but they also rely heavily on self-certification and good documentation practices.

Example scenario:

An expat software developer living in Bolivia works remotely for a US tech company. If they spend more than 183 days in Bolivia, their foreign salary remains untaxed locally.

But if they occasionally work with Bolivian clients or operate a small business from a home office, part of that income may become taxable domestically.

Are there exceptions to Bolivia’s 0% foreign income tax?

Some foreign-sourced income may still be taxable if it is effectively connected to Bolivian activities.

- Work performed in Bolivia: Income earned while physically present in Bolivia for client work—even if the client is abroad—may be considered domestic and subject to taxation.

- Bolivian-source investments: Rental income, dividends, or capital gains from Bolivian assets remain taxable.

- Digital nomad considerations: For remote workers providing services to foreign companies while in Bolivia, income is usually exempt. However, using local infrastructure or resources can create a taxable nexus.

- Policy stability: Bolivia’s territorial system is generally stable, but as with any jurisdiction, tax laws can evolve. High-net-worth expats should monitor potential changes and consult with professional advisors.

What do expats need to know to benefit from Bolivia’s tax system?

Expats must carefully plan residency, compliance, and lifestyle considerations to fully leverage the 0% foreign income tax benefit.

- Financial planning: Setting up international banking arrangements, remittance structures, and detailed records is critical for compliance. Even if taxes are zero, being able to prove foreign-source income can prevent unnecessary scrutiny.

- Exit strategy and mobility: Expats should understand the implications of leaving Bolivia or changing tax residency, including potential reclassification of foreign income and reporting obligations in their home country.

- Lifestyle considerations: Bolivia offers low-cost living but limited expat infrastructure compared to Chile, Uruguay, or Panama. Health care, international schools, and luxury services may require careful planning.

- Strategic migration: For high-net-worth individuals, Bolivia can form part of a diversified residency plan, leveraging tax efficiency while maintaining lifestyle and investment access.

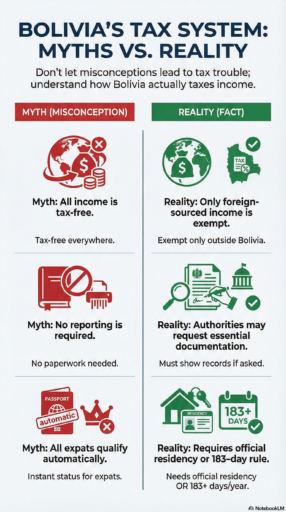

Common misconceptions about Bolivia’s tax system

Not all income earned abroad is automatically tax-free, and residency alone does not eliminate all obligations.

- Myth: Moving to Bolivia guarantees zero taxes on all income. Reality: Only foreign-sourced income is exempt; domestic income is taxable.

- Myth: No reporting is required. Reality: While reporting is limited, authorities can request proof. Documentation is essential.

- Myth: All expats qualify. Reality: Only residents under the 183-day rule or those meeting official residency criteria enjoy territorial taxation benefits.

Why is Bolivia a strategic option for tax-efficient residency?

Bolivia’s territorial system is a rare opportunity in South America, but its 0% foreign income tax, while real, is bounded by residency rules, domestic income definitions, and documentation requirements.

For investors, digital nomads, and expatriates, Bolivia can be part of a broader wealth migration strategy.

Its low cost of living, territorial taxation, and relatively stable policies make it a contrarian yet compelling choice for tax efficiency outside traditional offshore jurisdictions.

Investors or those seeking to diversify residency can use Bolivia as a stepping stone: benefiting from low taxes while monitoring economic and policy developments.

The combination of territorial taxation and cost-effective living creates a rare window for expats willing to navigate the rules carefully.

Why Bolivia Is Ignored in Global Tax Planning

Bolivia is rarely discussed in international tax planning circles because it lacks narrative positioning.

No Marketing Machine

Unlike Panama or Paraguay, Bolivia does not actively promote itself as a relocation or tax-planning hub.

It does not widely market:

- Digital nomad visas

- Investment migration programs

- Residency-by-deposit schemes

Without intermediaries promoting it, Bolivia remains largely off the radar.

Perception Risk

Bolivia is more often associated with political volatility than financial structuring. In wealth management, perception shapes adoption.

Jurisdictions seen as stable and internationally connected attract capital. Those viewed as economically modest are often overlooked, even when structurally efficient.

Limited Financial Ecosystem

Bolivia lacks a deep network of private banks, international advisors, and global law firms positioning it as a core jurisdiction.

It has:

- Limited international banking depth

- A modest treaty network

- Minimal offshore branding

Without ecosystem support, it remains niche.

It Doesn’t Sell Prestige

Bolivia offers tax efficiency, not mobility branding.

It does not provide:

- EU access

- Passport enhancement

- Investment migration visibility

In a market where residency planning often overlaps with lifestyle and status, Bolivia’s purely structural advantages make it easy to ignore.

However, for sophisticated investors, overlooked jurisdictions can offer asymmetric advantages precisely because they are not saturated.

The Real Risks of Using Bolivia as a Tax Base

Territorial taxation does not eliminate risk; it only shifts its nature.

The primary risks are not tax rates but structural exposure.

1. Source-of-Income Reclassification

If authorities determine income is effectively connected to Bolivian activities, it may be treated as domestic. Physical presence, use of local infrastructure, and client location can influence classification.

The risk is interpretational, not statutory.

2. Currency and Economic Risk

Bolivia operates in a region prone to macroeconomic volatility. Currency pressure, capital controls, or policy adjustments could affect:

- Banking access

- Remittance flows

- Financial stability

Tax efficiency does not immunize against macroeconomic instability.

3. Policy Stability Risk

While Bolivia’s territorial system has existed for decades, tax regimes globally are tightening.

Governments under fiscal stress may revise:

- Residency definitions

- Source rules

- Reporting obligations

Investors must monitor policy drift.

4. Infrastructure Limitations

Bolivia lacks:

- Advanced private banking networks

- Extensive double tax treaty networks

- Deep capital markets

For high-net-worth individuals, this creates operational friction.

5. Reputation and Mobility Risk

Unlike Uruguay or Panama, Bolivia does not offer strong international residency branding.

For some investors, jurisdiction perception matters when opening accounts or structuring cross-border holdings.

Bolivia is low-profile — which can be either an advantage or a constraint.

When Does Bolivia Make Sense Compared to Panama, Uruguay, and Paraguay?

Bolivia makes sense for remote earners and entrepreneurs who prioritize low foreign-income tax exposure and low living costs over banking sophistication, global branding, or premium infrastructure.

- Panama suits internationally mobile investors needing strong banking access.

- Uruguay fits high-net-worth individuals seeking stability and lifestyle quality.

- Paraguay appeals to cost-sensitive residency planners seeking simplicity.

| Factor | Bolivia | Panama | Uruguay | Paraguay |

| Foreign Income Tax | Generally exempt under territorial system | Generally exempt (territorial) | Partial exemptions with structured incentives | Territorial, but certain foreign income may be taxed |

| Residency Threshold | 183 days | Friendly Nations / visa pathways | Tax residency with structured incentives | Permanent residency relatively accessible |

| Cost of Living | Low | Moderate to high | High (regional standards) | Low |

| Banking Infrastructure | Limited international banking | Strong international banking | Stable, developed banking | Limited to moderate |

| Global Reputation | Low-profile | Established offshore hub | Stable, reputable | Growing but niche |

| Best For | Remote workers, cost-focused expats | Global investors, structured planners | HNW families seeking stability | Budget-focused residency seekers |

FAQs

Does Bolivia tax foreign income for residents?

No. Under Bolivia’s territorial tax system, residents are generally exempt from paying tax on income earned abroad. Only domestic income sourced within Bolivia is taxed.

Who qualifies for Bolivia’s territorial tax exemption?

Expats who meet residency requirements—spending at least 183 days in a calendar year in Bolivia—can qualify for the 0% foreign income tax benefit.

Proper documentation proving foreign income is recommended.

Do expats need to report foreign income in Bolivia?

Bolivia does not require comprehensive foreign income reporting, but expats should keep records such as invoices, contracts, and bank statements to prove the income is sourced abroad.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.