Portugal generally has lower taxes and living costs for retirees and expats, while Spain can be more expensive for high earners.

Property taxes, retirement income taxation, and daily expenses also differ significantly between the two countries.

This article covers:

- Is Portugal or Spain better for retirement?

- Is income tax higher in Spain or Portugal?

- What is the consumption tax in Portugal?

- What is the consumption tax in Spain?

Key Takeaways:

- Portugal often offers lower overall taxes for retirees and expats.

- Spain’s cost of living is higher in major cities but competitive in smaller towns.

- Property taxes are generally cheaper in Portugal.

- Portugal is safer and more expat-friendly, while Spain has a larger, more diverse economy.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions.

The information in this article is not tax advice and may have changed since the time of writing. I can connect you with expert tax support for your specific situation.

Does Spain or Portugal Have Higher Taxes?

Spain generally imposes higher overall taxes than Portugal, including income tax and social security contributions, though exact rates vary by region.

- Portugal: The top personal income tax rate is around 48%. Social security contributions are lower than in Spain, generally around 11% for employees and 23.75% for employers.

- Spain: The top personal income tax can reach 47% depending on the region. Social security contributions are higher, typically around 6.35% for employees and up to 30% for employers, depending on salary level. Certain regions, like Madrid, offer slightly lower income tax rates, but social security is largely consistent nationwide.

Overall, for high earners, Spain’s combined tax and social security burden is usually higher, while Portugal provides a relatively lighter total tax load for most residents.

Is it Cheaper to Live in Spain or Portugal?

On average, living in Portugal is slightly cheaper than in Spain, including daily expenses, utilities, and overall consumption patterns, though costs vary by city and lifestyle.

- Portugal: Daily expenses, groceries, and utilities are generally lower than in Spain. Household consumption rates are moderate, and VAT (IVA) is 23% standard, 13% intermediate, and 6% reduced on essential goods and services. Lisbon and Porto are more expensive than smaller towns, but healthcare, transportation, and dining out remain relatively affordable.

- Spain: Larger cities like Madrid and Barcelona are costly, while smaller cities and southern regions such as Andalusia are cheaper. VAT (IVA) is slightly lower than Portugal at 21% standard, 10% reduced, and 4% super-reduced for essentials. Household consumption rates for utilities, services, and everyday goods are slightly higher than in Portugal, especially in urban areas.

Is it Better to Retire in Spain or Portugal?

Portugal is generally the more affordable country to retire in compared to Spain, due to lower overall living costs and a lighter combined tax burden for most retirees.

- Portugal: Pension and social security income is taxed at moderate rates based on residency status, and healthcare contributions are generally lower than in Spain. Public healthcare is high-quality and mostly free or low-cost for residents, while private health insurance is affordable. Daily living costs including groceries, utilities, and transportation are also lower than in Spain.

- Spain: Pension income from abroad is taxed under Spain’s progressive personal income tax (IRPF), with rates ranging from 19% up to 47% depending on total income. Social security contributions are slightly higher than in Portugal. Public healthcare is excellent but may involve co-pays for certain services, and private insurance is generally more expensive than in Portugal. Urban areas like Madrid and Barcelona have higher living costs, including utilities and everyday expenses.

For retirees prioritizing low pension and social security taxes combined with affordable healthcare and living costs, Portugal often provides the better option, while Spain may appeal for those seeking larger cities and more extensive infrastructure.

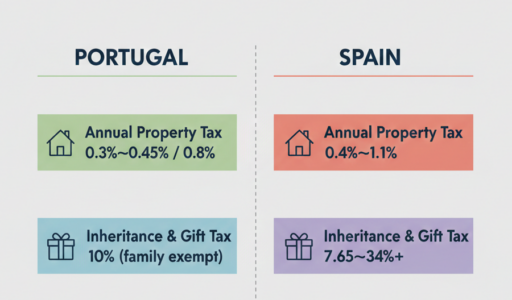

Are Property Taxes High in Portugal vs Spain?

Portugal typically imposes lower property and related taxes than Spain, making it more affordable for homeowners and retirees.

- Portugal: Portugal’s annual property tax IMI generally ranges from 0.3%–0.45% for urban properties and 0.8% for rural land (set by municipalities), property purchases are subject to IMT transfer tax up to 7.5% depending on value and use, and while Portugal has no traditional inheritance tax, stamp duty of 10% applies to inheritances and gifts outside close family (with a 0.8% rate on real estate transfers).

- Spain: Annual property tax (IBI) ranges from 0.4% to 1.1%, depending on the municipality. Wealth tax may apply for high-value properties. Inheritance and gift taxes in Spain vary by region and relationship to the beneficiary, with rates ranging from 7.65% to over 34% in some autonomous communities.

Tax Efficiency vs Lifestyle: Choosing Between Portugal and Spain

Taxes are an important factor, but they should be considered alongside lifestyle and long-term living preferences.

Portugal offers generally lower taxes, simpler inheritance rules, and predictable property costs, making it appealing for retirees and expats seeking financial clarity.

Spain, however, provides larger cities, more extensive infrastructure, and greater cultural and regional diversity, which can enhance quality of life despite higher tax exposure.

Ultimately, the choice between the two countries is a matter of financial optimization versus lifestyle priorities.

The best decision aligns tax efficiency with safety, healthcare, climate, and daily living preferences.

Conclusion

The key distinction between Portugal and Spain for expats and retirees lies in taxation structure and predictability.

Portugal offers lower overall tax exposure, straightforward property rules, and simpler inheritance treatment, making financial planning clearer and more stable.

Spain’s progressive income tax, regional wealth taxes, and varied property-related rules can increase complexity, requiring careful attention to optimize your total tax burden.

For anyone relocating or retiring, understanding these differences is essential to make informed decisions that protect both income and assets.

FAQs

Who has a better economy, Spain or Portugal?

Spain has a larger economy, higher GDP, and more diverse industries.

Portugal’s economy is smaller but growing steadily, particularly in tech and tourism.

Is Portugal warmer than Spain?

Spain is generally warmer, especially in the south (Andalusia) and islands (Canary, Balearic).

Portugal’s southern region, the Algarve, enjoys mild winters and warm summers.

What is safer, Portugal or Spain?

Portugal consistently ranks safer than Spain, appearing near the top of the Global Peace Index with lower overall crime rates.

Spain is generally safe, though petty crime is higher in major cities like Madrid and Barcelona.

Is property cheaper in Spain or Portugal?

Property prices vary widely, but Portugal’s smaller towns and inland areas are usually cheaper, while Spain’s southern regions and smaller cities can be comparable.

Lisbon and Porto are among the most expensive areas in Portugal.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.