Swiss Life Alpha Plus is a investment-linked life insurance plan that combines life coverage with investment opportunities.

It allows policyholders to grow their wealth through a selection of funds while benefiting from life protection.

However, fees, market risks, and suitability should be considered before investing.

This article covers:

- What is Swiss Life Alpha Plus VUL?

- Swiss Life Alpha Plus Benefits

- Swiss Life Alpha Plus Disadvantages

Key Takeaways:

- Swiss Life Alpha Plus is a VUL policy combining insurance and investments.

- Policy value is based on premiums, fund performance, and fees.

- Partial withdrawals are possible but may reduce the death benefit.

- Early surrender can incur fees, affecting overall policy value.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions.

The information in this article is for general guidance only. It does not constitute financial, legal, or tax advice, and is not a recommendation or solicitation to invest. Some facts may have changed since the time of writing.

Who is Swiss Life?

Zurich, Switzerland-based Swiss Life is an insurance and financial services group founded in 1857.

It provides life insurance, pensions, and investment products to individuals and corporate clients, with operations across Europe and select global markets.

Swiss Life’s Trustpilot profile shows mixed experiences, with a significant number of negative reviews citing service and transparency problems.

What is Swiss Life Alpha Plus?

Swiss Life Alpha Plus is a variable universal life (VUL) insurance policy offered by Swiss Life.

It provides both:

- Life insurance coverage – a death benefit for beneficiaries.

- Investment component – the policyholder can allocate a portion of the premium into various funds, including equities, bonds, or mixed portfolios.

Swiss Life Alpha Plus VUL is being marketed and sold in markets like Singapore, Hong Kong, and other Asian regions, targeted at high‑net‑worth investors through intermediaries.

What is a VUL?

A variable universal life (VUL) policy is a type of permanent life insurance that combines flexible premiums, life coverage, and market-linked investments.

Unlike traditional life insurance, a VUL allows part of your premium to be invested in funds that can grow or decline depending on market performance.

As a variable universal life policy, Alpha Plus is structured as a single-premium VUL, meaning it is funded with a one-time upfront payment.

It offers tax deferral on investment growth within the policy until distribution or withdrawal, allowing for more efficient portfolio accumulation.

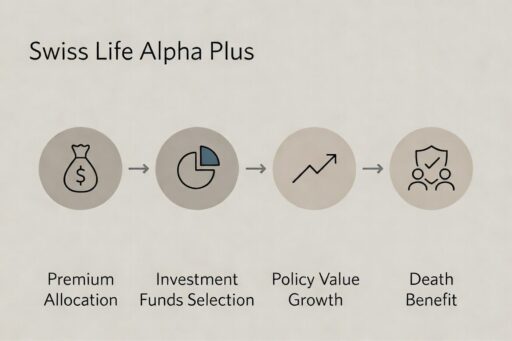

How Swiss Life Alpha Plus Works

Swiss Life Alpha Plus works by investing your premium into selected funds within a life insurance policy, allowing the policy value to grow over time while providing a built-in death benefit.

1. Premium Allocation

A single premium is paid into the policy. After deducting insurance and administrative charges, the remaining amount is invested.

2. Investment Funds Selection

The invested portion is allocated into chosen funds such as equity, bond, or balanced portfolios. The policy value rises or falls based on fund performance.

3. Policy Value Growth

The investment value accumulates inside the policy over time. This value can potentially grow but is subject to market risk.

4. Death Benefit

When the insured person dies, beneficiaries receive either the policy value or a guaranteed minimum benefit, depending on the policy structure.

What are Swiss Life Alpha Plus features?

Swiss Life Alpha Plus includes a single-premium contribution, access to multiple investment funds, partial withdrawal options, and potential tax efficiency depending on residence.

- One-time Contribution. Clients pay the entire premium amount at once, rather than monthly or annually. This is ideal for investors who have a lump sum to deploy.

- Investment Choice. Policyholders can allocate premiums across a range of internal and external funds, including equity, bond, and diversified portfolios. The available options allow investors to align the policy with their risk tolerance and long-term investment goals.

- Partial Withdrawals. Swiss Life Alpha Plus may allow partial withdrawals from the policy value after a certain period. However, withdrawals can reduce the death benefit, sum assured, or overall policy value proportionally. Withdrawals could also trigger taxes or penalties depending on the amount and jurisdiction-specific rules.

- Tax Advantages. In some jurisdictions, investment growth within a life insurance policy may benefit from tax deferral or favorable treatment. The actual tax treatment depends on the policyholder’s country of residence and local tax rules.

What is Swiss Life Alpha Plus VUL Worth?

The value of a Swiss Life Alpha Plus VUL varies based on the premiums paid, investment performance of the selected funds, policy charges, and how long the policy is held.

The total premiums paid into a Swiss Life Alpha Plus policy determine its investment base.

After charges, the remaining funds are allocated to chosen investment options, and higher or consistent contributions generally lead to greater policy value over time.

The policy’s investment value hinges on the performance of the selected funds, which may include equities, bonds, or diversified portfolios.

Strong market performance grows the policy, while downturns can reduce its value.

Policy charges, including insurance costs, administration, and fund management fees, are deducted from the investment value and affect long-term returns.

VUL policies like Swiss Life Alpha Plus are intended for long-term holding, giving the investment component time to compound. Early surrender can reduce growth and overall policy value.

Swiss Life Alpha Plus Pros and Cons

Swiss Life Alpha Plus offers flexible investing within a life insurance policy, but potential investors should weigh the benefits of diversification and insurance coverage against fees, market risk, and long-term commitment.

Pros of Swiss Life Alpha Plus

- Single-premium simplicity – A one-time payment funds the policy, making it straightforward to manage while still providing both life coverage and investment growth.

- Investment diversification – Policyholders can allocate funds across different asset classes such as equities, bonds, and diversified portfolios.

- Combined insurance and investment – The policy provides life protection while allowing capital to grow through market investments.

- Potential tax efficiency – In some jurisdictions, investment growth within life insurance policies may benefit from favorable tax treatment.

- Simplified reporting – Additional benefits may include simplified reporting under Common Reporting Standard (CRS).

Cons of Swiss Life Alpha Plus

- Market risk – The policy value is linked to the performance of selected investment funds and may fluctuate with market conditions.

- Ongoing policy charges – Insurance costs, administration fees, and fund management charges can reduce net investment returns.

- Product complexity – Understanding the structure of a VUL policy, including investment allocation and insurance charges, may require professional advice.

- Early surrender costs – Cancelling the policy in the early years may result in surrender charges and a reduced payout.

Is Swiss Life Alpha Plus Worth It?

Swiss Life Alpha Plus can be worth it for investors who want long-term life insurance combined with market-linked investment growth.

The policy combines life coverage with an investment component, offering potential higher returns through fund selection compared with traditional insurance.

With a long-term horizon and comfort with market fluctuations, the investment portion can grow significantly over time.

However, charges such as insurance costs and fund management fees reduce net growth, especially in the early years.

Because it’s investment-linked, returns aren’t guaranteed as market downturns can lower the policy value.

It may not suit those looking for low-risk or short-term solutions.

Some customers acknowledge that Swiss Life itself, the company behind this VUL product offering, isn’t a scam and can be suitable depending on individual needs and better planning.

Others praise individual advisors for being professional, responsive, and helpful.

Major complaints center on customer service, fee transparency, and claims handling.

Worth it if you:

- Have a long-term horizon and can handle market volatility.

- Want life insurance protection that also builds investment value.

- Can manage fund choices and understand fees.

Less worth it if you:

- Prefer guaranteed returns or low volatility.

- Have short-term financial targets.

- Don’t want to monitor investments and policy costs.

Is a VUL or IUL better?

A VUL offers market-linked investment potential through funds, while an indexed universal life (IUL) ties returns to a market index with caps and floors, making VULs generally higher risk and potentially higher return.

Investment Structure

A VUL allows policyholders to invest premiums in equity, bond, or balanced funds. Returns depend directly on market performance, meaning gains can be higher but losses are also possible.

An IUL, by contrast, credits interest based on the performance of a market index such as the S&P 500. However, returns are usually subject to caps and participation rates.

Risk and Return

VUL policies carry higher market risk but greater upside potential because investments are directly exposed to market movements.

IUL policies typically offer downside protection through floors, meaning returns may not fall below zero in a negative market year, though upside is limited.

Flexibility

Both VUL and IUL policies allow flexible premiums and adjustable death benefits, but VUL policies provide more control over investment allocation.

Which One Is Better?

Neither structure is universally better. VUL policies suit investors comfortable with market risk and long-term investing, while IUL policies appeal to those seeking more predictable growth with downside protection.

FAQs

Who is the owner of Swiss Life?

Publicly traded insurance group Swiss Life shares are held by UBS Fund Management (Switzerland) AG, which holds over 5% of shares, and BlackRock Inc. also holding more than 5%.

The rest of the company is widely held by other investors globally.

Is a VUL a good investment?

A variable universal life (VUL) insurance can be suitable for those looking to combine life insurance with investment growth.

Its value depends on market performance, fees, and how long the policy is held, so it works best for long-term investors comfortable with market fluctuations.

What is term plus life insurance?

Term plus life insurance combines a term life policy with an investment or savings component, offering temporary coverage along with some capital growth or benefits.

Is Swiss Life a good company?

Swiss Life is considered a reputable insurance and financial services provider with a long history, strong solvency ratings, and a broad international presence.

However, some customer reviews highlight slow claims processing and limited customer service responsiveness, which can be frustrating for policyholders.

Is VUL a lifetime payment?

VUL policies can last for the insured’s lifetime if premiums are maintained, but policyholders must continue paying premiums or ensure sufficient policy value to cover ongoing costs.

Can I cash out my VUL?

Yes, policyholders can access the cash value through withdrawals or by surrendering the policy.

Early withdrawals or full surrender may reduce the death benefit and incur fees, so timing and strategy are important to preserve value.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.