Geopolitical events create short-term market volatility but rarely destroy long-term investment returns.

Stocks often recover after crises, while bonds, cash, and real estate often face inflation and liquidity pressures.

Expats and high-net-worth investors protect wealth through diversification across geographies, asset classes, and liquidity channels rather than trying to predict crises.

The key question for investors is not whether crises occur, but how markets historically respond to them.

Watch This: How to Invest Through Geopolitical Uncertainty

Key Takeaways:

- Short-term volatility is normal; long-term growth trends persist.

- Capital controls, withdrawal limits, and inflation can materially impact portfolios.

- Equities outperform fixed-income and real estate during crises, though sector outcomes are unpredictable.

- Planning and historical evidence should guide investment decisions.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions. We also offer bespoke structuring solutions tailored to your situation.

The information in this article is for general guidance only, does not constitute financial, legal, or tax advice, and may have changed since the time of writing.

Why Do Investors Overestimate Geopolitical Risk?

Investors often focus on extreme, improbable events, but moderate, plausible risks usually have a more direct impact on portfolios.

Most headlines highlight world wars, global crashes, or systemic economic collapse.

Yet historically, smaller, overlooked events—like capital controls, banking restrictions, inflation shocks, and currency devaluations—have caused measurable financial disruption.

Many expats and high-net-worth investors assume developed financial systems are immune to these disruptions.

However, the Cyprus Banking Crisis demonstrated that even European banking systems can impose sudden restrictions during financial stress.

Depositors with balances above €100,000 temporarily lost access to a portion of their funds.

Planning for plausible disruptions rather than catastrophic headlines is a more reliable strategy for long-term wealth preservation.

Capital Controls Are More Realistic Than Many Think

Capital controls and withdrawal limits can restrict access to cash, making them a real liquidity risk for globally mobile investors.

Even in stable jurisdictions, governments or financial institutions can impose restrictions to stabilize the banking system during periods of stress.

As seen during the Cyprus crisis, access to deposits can be limited without warning when banks face liquidity pressure.

Similar restrictions have appeared in other markets:

- During the Greek Government-Debt Crisis, ATM withdrawals were limited to €60 per day.

- In the Lebanese Financial Crisis, banks imposed informal capital controls that prevented many depositors from accessing savings.

For expats and internationally diversified investors, these examples highlight the importance of planning for liquidity risks.

Practical strategies include:

- Avoid concentrating large cash balances in a single bank or jurisdiction.

- Diversify liquidity across multiple countries and financial institutions.

- Maintain exposure to liquid assets such as equities, commodities, or professionally managed downside-protected portfolios that can hedge inflation and currency risk.

Which Assets Perform Best During Wars?

Energy, commodities, and defense sectors often outperform early in conflicts, but unexpected winners highlight the importance of diversification.

Historical patterns show:

- Early stage outperformers: Energy, commodities, defense

- Unexpected winners: World War II saw printing, publishing, and alcohol sectors outperform traditional industrials

- Medium- to long-term: Technology and growth sectors may dip initially but recover within 1–3 years

Predicting sector winners during crises is unreliable; diversified exposure remains the most consistent approach.

Bonds and Real Estate During Geopolitical Crises

Fixed-income and illiquid assets tend to be more vulnerable to inflation and interest-rate shocks than equities during periods of geopolitical instability.

Conflicts often lead to higher government spending, supply disruptions, and fiscal stimulus, all of which can push inflation higher.

When inflation rises faster than nominal yields, the real returns of bonds and other fixed-income investments deteriorate.

As a result, fixed-income portfolios can underperform during prolonged inflationary environments triggered by geopolitical shocks.

Real estate also faces structural risks during these periods. Property markets are typically sensitive to interest-rate increases, and leveraged investments become more expensive to maintain when borrowing costs rise.

Because real estate is illiquid, investors cannot easily reposition or rebalance holdings during periods of market stress.

More liquid assets, particularly diversified equities, have historically tended to preserve long-term value better than bonds or highly leveraged property during periods of geopolitical uncertainty.

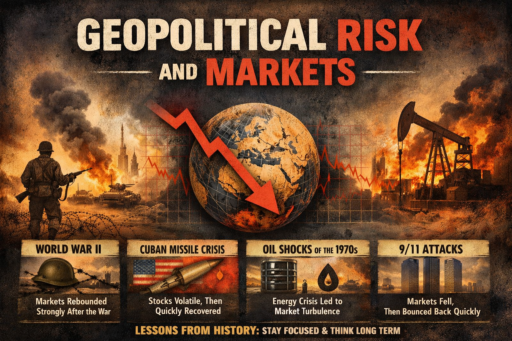

How does the stock market usually respond to war?

Markets dip in the short term during conflicts but usually recover within 6–24 months, and long-term trends remain intact.

Historical data shows:

- Initial market drops of 5–20% are common in the first days or months of conflict.

- Recovery typically occurs within 6–24 months, even after severe geopolitical shocks.

- Large-cap stocks historically maintain ~10% annual returns; small-cap stocks often outperform during crisis periods.

Examples:

- Russia–Ukraine conflict (2022): Sharp initial drop, then recovery within two years.

- Cuban Missile Crisis, Gulf War, Kennedy assassination: Temporary dips with eventual normalization.

Panic selling often locks in losses unnecessarily. Long-term market trends are resilient.

How Should Investors Prepare for Geopolitical Uncertainty?

Resilient portfolios combine diversification, liquidity planning, and evidence-based asset allocation rather than crisis prediction.

Investment strategies for HNWIs and expats:

- Maintain geographic diversification across multiple countries and currencies.

- Diversify asset classes: equities, commodities, alternative investments, and liquid cash.

- Avoid excessive concentration in illiquid local assets such as over-leveraged property.

- Monitor inflation risk and include assets that preserve purchasing power.

- Use advisory-managed products for downside protection while maintaining upside potential.

Reacting emotionally to geopolitical headlines typically undermines long-term performance. Disciplined, proactive planning is more effective.

FAQs

Should I sell stocks during geopolitical crises?

Selling stocks during geopolitical crises is usually a reaction to short-term volatility rather than a sound investment strategy.

Markets often decline when uncertainty rises, but historically they tend to recover once the immediate shock passes.

Investors who sell during the initial downturn often lock in losses and miss the rebound that typically follows.

Are government bonds completely safe?

Not always. Government bonds are often considered safer than equities, but they are not risk-free.

During inflationary periods—especially those triggered by conflict, supply disruptions, or heavy government spending—the real value of fixed-income returns can decline.

If inflation rises faster than bond yields, investors effectively lose purchasing power. Additionally, rising interest rates can cause bond prices to fall.

What is the best way to protect your cash?

Protecting cash requires diversification and liquidity planning rather than simply holding large balances in a single bank account.

Concentrating deposits in one jurisdiction or institution can expose investors to risks such as withdrawal limits, capital controls, or currency instability.

A more resilient approach is to spread liquidity across multiple jurisdictions and financial institutions.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.