Trusts, foundations, and special purpose vehicles (SPVs) are legal structures used by high-net-worth individuals to protect assets, structure investments, and manage wealth across jurisdictions.

While they are often mentioned together in international wealth planning, each serves a distinct legal and strategic purpose.

Key Takeaways:

- Trusts separate legal ownership from beneficiaries, used for succession planning and asset protection.

- Foundations are independent legal entities designed to preserve family wealth across generations.

- SPVs isolate individual investments to limit financial and legal exposure.

- These structures are often combined in layered ownership frameworks for international investors.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions. We also offer bespoke structuring solutions tailored to your situation.

The information in this article is for general guidance only, does not constitute financial, legal, or tax advice, and may have changed since the time of writing.

What is a special purpose vehicle (SPV)?

A special purpose vehicle or SPV is a company created for a specific financial or investment purpose.

Rather than holding assets directly, investors place them into a separate legal entity that exists solely to own or manage that investment.

SPVs are widely used in international finance because they isolate a particular asset or transaction from the investor’s broader wealth structure.

Real estate developments, private equity investments, and infrastructure projects are frequently structured through SPVs so that each project remains legally independent.

Jurisdictions with strong corporate frameworks often attract SPV structures, including Luxembourg, Singapore, and the United Arab Emirates.

Why are SPVs useful to investors?

The primary advantage of an SPV is risk isolation. When an asset is held through a dedicated vehicle, liabilities tied to that asset typically remain within the SPV.

If a property investment held through an SPV encounters legal claims or financial losses, creditors generally pursue the SPV rather than the investor personally.

This concept, often called ring-fencing risk, is one of the reasons SPVs are widely used in institutional finance.

However, the protection depends on proper structuring and governance. Personal guarantees or poorly maintained corporate records can weaken the legal separation between the investor and the SPV.

Can SPVs invest internationally?

SPVs are frequently used to facilitate international investment strategies.

Instead of each investor purchasing assets individually, they can participate in a shared SPV that holds the investment.

This structure simplifies ownership arrangements, particularly in multi-jurisdiction deals where investors may come from various countries.

For example, investors from several countries might participate in a European real estate project through a Luxembourg SPV. The SPV becomes the legal owner of the investment while investors hold shares in the vehicle.

Beyond administrative efficiency, this structure can also support tax treaty access and regulatory compliance when structured correctly.

What are the risks of using an SPV for asset protection?

Despite their usefulness, SPVs are not designed as complete asset protection structures on their own. Their purpose is primarily transactional—isolating the risk of a particular investment.

If an investor personally guarantees loans or fails to maintain corporate formalities, the protective barrier between the SPV and the investor may weaken.

Regulatory oversight has also increased significantly in recent years.

Transparency frameworks promoted by organizations such as the Financial Action Task Force and the Organisation for Economic Co-operation and Development require financial institutions to identify beneficial owners of corporate vehicles.

For this reason, SPVs are usually integrated into broader wealth structures rather than used as standalone protection mechanisms.

How SPVs Can Help With Privacy

SPVs do not provide secrecy, but they can reduce the direct public visibility of asset ownership by placing assets inside a separate legal entity.

This works because:

- The SPV becomes the legal owner of the asset instead of the individual.

- Public registries list the company, not the investor.

- Common in asset-heavy investments, such as real estate, aviation, and private investment vehicles.

- Beneficial owners may still be disclosed to regulators and financial institutions

As a result, SPVs provide asset confidentiality within regulatory frameworks, not anonymity.

What is a trust and how does it protect assets?

A trust is a legal arrangement in which a person transfers assets to a trustee who manages them for the benefit of designated beneficiaries.

Unlike a corporation, a trust is not always a separate legal entity. Instead, it is a legal relationship that divides ownership into different roles:

- the settlor, who establishes the trust

- the trustee, who manages and legally owns the assets

- the beneficiaries, who receive the benefits of those assets

Because the trustee holds legal title, the assets are no longer directly owned by the individual who created the trust.

This separation can provide a degree of protection against personal liabilities, estate disputes, and creditor claims.

Trust structures are widely used in jurisdictions such as Jersey, Cayman Islands, and Nevis, which have developed specialized trust legislation for international wealth planning.

How can expats use trusts for investing?

For expat, trusts can serve as central structures for managing investments across multiple jurisdictions.

Instead of holding shares, real estate, or investment portfolios directly, individuals may transfer those assets into a trust.

The trust then becomes the long-term owner of those investments while trustees manage them according to the trust deed.

This arrangement can simplify succession planning for families whose members live in different countries, while also consolidating asset management under a single legal structure.

How do trusts keep my wealth private?

Trusts can provide financial privacy because the trustee is typically the legal owner of the assets, which can reduce the direct visibility of personal wealth.

This works because:

- The trustee is the legal owner of the assets, not the beneficiary.

- Beneficiaries are often not listed in public registries in many jurisdictions.

- Financial institutions usually record the trustee as the account holder, rather than the individual beneficiaries.

- Regulatory reporting may still apply, as frameworks such as the CRS require certain trust information to be reported to tax authorities.

As a result, trusts provide structured confidentiality rather than secrecy.

What is a foundation and why is it important?

A foundation is a legal entity created to hold and manage assets for a specific purpose, such as wealth preservation, succession planning, or philanthropy.

Once assets are transferred to a foundation, they belong to the foundation itself rather than the individual who created it.

Foundations are widely used in civil-law jurisdictions, particularly for long-term wealth planning by international families.

Common jurisdictions that support private foundations include Panama, Liechtenstein, and Switzerland.

How do foundations protect wealth for HNWIs?

Foundations protect wealth by transferring assets into an independent entity governed by a charter and overseen by a council or board.

Once assets are transferred to the foundation, they are no longer personally owned by the founder.

The foundation manages those assets for specific purposes, which may include family wealth preservation, succession planning, or philanthropy.

This structure can provide continuity across generations because the foundation continues to exist even if the founder passes away.

For wealthy families seeking long-term wealth preservation, foundations can function as stable vehicles for managing investments, businesses, and family assets.

How do foundations support asset privacy?

Foundations do not provide secrecy, but they can reduce the direct public visibility of personal asset ownership.

This works because:

- The foundation is listed as the legal owner of the assets.

- Public records may show the foundation rather than the individual founder.

- Assets can be managed through the foundation structure rather than personal accounts.

- Regulators may still require disclosure of beneficial owners under modern transparency frameworks.

What is the difference between a foundation and a trust?

A foundation is a separate legal entity that owns assets in its own name, while a trust is a legal arrangement where trustees hold and manage assets on behalf of beneficiaries.

Key distinctions include:

- Legal status: A foundation is an independent legal entity, whereas a trust is a legal relationship managed by trustees.

- Asset ownership: In a foundation, the entity itself owns the assets. In a trust, the trustee holds legal ownership for the benefit of beneficiaries.

- Governance: Foundations are typically managed by a council or board, while trusts are administered by trustees.

- Legal tradition: Trusts are common in common-law jurisdictions, while foundations are more prevalent in civil-law systems.

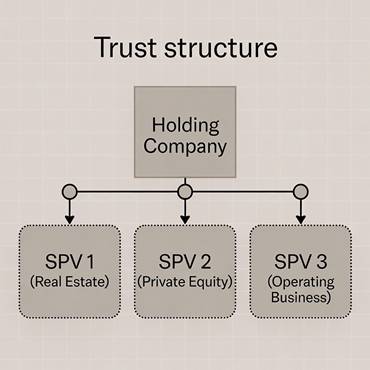

Can trusts and SPVs be combined for HNWIs?

Yes, sophisticated wealth structures often combine trusts and SPVs.

A trust may hold the shares of a holding company, which in turn owns multiple SPVs. Each SPV holds a specific investment or asset, allowing risks to be isolated while the trust maintains overall ownership.

This layered model provides several advantages. Investment risk remains confined within each SPV, while the trust separates personal ownership from the assets themselves.

Such arrangements are common among international investors managing diversified portfolios that include real estate, private equity, and operating businesses.

How do different countries treat trusts and foundations for expats?

Common-law countries typically recognize trusts as standard legal structures. Civil-law countries often rely more heavily on foundations, since traditional trust law may not exist in their legal systems.

Examples of trust-friendly common-law jurisdictions include the United Kingdom, Singapore, and Australia.

Jurisdictions such as Liechtenstein and Panama have developed foundation frameworks specifically designed for international wealth planning.

For expats, the most important factor is how their home country treats these structures for tax and reporting purposes.

The same trust or foundation may receive very different treatment depending on the individual’s residency and tax obligations.

Choosing Between Trusts, Foundations, and SPVs

Trusts are commonly used for asset protection and succession planning, foundations for long-term wealth preservation in civil-law systems, and SPVs for investment structuring and liability isolation.

They are not interchangeable tools, and each serves a distinct function within a broader wealth structure.

For high-net-worth individuals managing international assets, the most resilient strategies often combine these structures.

Layered ownership frameworks allow investors to separate risks, manage global investments efficiently, and preserve wealth across generations in an increasingly transparent global financial environment.

| Structure | Key Role | Ownership | Privacy | Best Use | Confidential & Protective |

|---|---|---|---|---|---|

| SPV | Isolate investment risk | Holds assets | Reduces visibility | Investment structuring | ✔ (privacy only) |

| Trust | Asset protection & succession | Trustee holds assets | Beneficiaries not public | Cross-border wealth, succession | ✔ |

| Foundation | Preserve long-term wealth | Foundation owns assets | Founder not listed | Civil-law succession, philanthropy | ✔ |

FAQs

Who typically uses SPVs?

SPVs are used by institutional investors, high-net-worth individuals, and companies to isolate specific assets or projects.

They are common in real estate, private equity, infrastructure, and cross-border investment deals.

What is the minimum investment for an SPV?

There is no universal minimum; it is determined by the SPV’s purpose, jurisdiction, and governing documents. Some SPVs are created for single large projects, while others pool multiple investors.

Legal and setup costs may make SPVs more suitable for mid- to high-value investments.

What is the difference between an SPE and an SPV?

A special purpose entity (SPE) is a broad legal concept for an entity created for a specific purpose. An SPV is a type of SPE that specifically holds assets or investments.

Essentially, all SPVs are SPEs, but not all SPEs are SPVs.

Who is the best person to manage a trust?

The best trustee is a professional fiduciary or corporate trustee with experience in wealth management, legal compliance, and cross-border investments.

High-net-worth families often combine professional trustees with a family advisory board for oversight.

Who has the most power in a trust?

Power varies based on the trust deed. Typically, the trustee holds legal authority over assets, but the settlor may retain certain powers (like appointing or removing trustees) if allowed.

Beneficiaries usually do not control assets directly but benefit according to the trust’s terms.

Do foundations have an owner?

No. A foundation is an independent legal entity. Assets belong to the foundation itself, not an individual.

A governing council or board manages the foundation according to its charter, while the founder may have influence through the foundation’s rules or advisory roles.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.