I often write answers on Quora, where I am the most viewed writer for investing, wealth and personal finance, with over 243.5 million views in the last few years.

On the answers below, taken from my online Quora answers, I focus on a range of topics including:

- I was asked “can I apply for a mortgage in the UK as a non-resident?” This answer applies for both UK expats living overseas and other nationalities. Buying property in the UK when abroad is something many expats are looking for.

- Why is China cheaper than Japan? Is the premise of the question even true? I explain why China is no longer as cheap as people assume, at least in the big cities.

- What’s the biggest cause of irrational investment behaviour? The media, peer pressure or something else?

- Is it a good idea to lend money to friends and family members?

- Am I willing to take a risk in the stock market? Are the stock markets even risky to begin with?

Some of the links and videos referred to might only be available on the original answers.

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Can I apply for a mortgage in the UK as a non-resident?

Source: Quora

The simple answer is yes you can – both as a British expat or non-Brit living overseas.

Of course whether you are likely to be accepted depends on many things including:

- What kind of job you do. Is it something vanilla, like a salaried position in a low-risk industry, or higher risk like a self-employed person?

- Where you live. If you live in Iraq in oil&gas, you have less chance of being accepted compared to if you live in a more typical expat location

- How much you want to take out as a mortgage relative to your income

- Which lender you are dealing with. Some are stricter than others

- The size of your downpayment

- Your previous credit history and many other factors.

The bigger question is whether you should apply for a mortgage.

It is true that the UK is very friendly to overseas investment and has now stimulated the housing market by eliminating stamp duty on most home purchases for a limited time.

The UK’s rental yields, at least outside of London, are also far superior to many countries.

Yet the biggest negative about real estate is the risk and time adjusted returns.

What I mean by that is that unless you are a professional in real estate, or can outsource it to a professional company, you need to work very hard for a return which isn’t always better than say the S&P500.

I personally know several people who have made 6%-8% net of taxes and costs, which are higher for property compared to other investments, for doing a lot of work.

You can invest tax-free in many countries in an investment structure.

You can include real estate investment trusts (REITS) in that structure.

With property the taxes are even higher than usual capital gains in the UK and other countries.

So, my advice would be to leave it or completely outsource the whole process.

If you can find a company which will find tenants for you, manage it and then plan the exit (selling) you have eliminated one huge negative associated with property.

Why is China cheaper than Japan?

Source: Quora

Having lived in both places, I can say that it isn’t universally cheaper.

The following things are cheaper

- Things which are in public ownership like the trains, subways etc

- Some of the absolute basics like say rice

- Anything which is a foreign brand but manufactured in China – like Coca Cola as an example.

- Rents for the most part

- Many service-sector activities like staying at hotels

- Online purchases are cheap in both places but more so in China

- Anything at the lower end in terms of quality.

- Buying things in bulk if you are a business and manufacturing.

The following things are more expensive

- Buying real estate in many large Chinese cities

- Many imported goods including plenty of imported cars, consumer goods like cheese and this is sometimes reflected in foreign bars and restaurants as well.

- Anything considered on the luxury end. So sending your kids to international school, as an example, will cost even more in Shanghai than Tokyo.

So basically, if you are young and single, and can avoid luxury and foreign tastes, then China is much cheaper.

If you want to go to foreign bars and restaurants and send your kids to international school, then China might be more expensive.

Of course China is a big place, but the first tier cities can be expensive, and some of the above items are expensive pretty much anywhere.

Taxes are also about the same, and sometimes more in Mainland China.

That is one reason why many highly paid expats prefer Hong Kong and Singapore to Mainland China, as taxes are part of the cost of living.

The things that cost less have been influenced by government policy, low labour costs in those specific sectors and economies of scale due to the large population.

Let’s not forget as well that per capita income is about six times higher in Japan than China, and there are a lot of people living on a relatively small island.

What causes irrational investment behavior?

Source: Quora

The short answer is human emotions. The long answer is it is difficult to know what causes those emotions to begin with.

Some would point to the media and associated sensationalist headlines:

Some would point to peer pressure. In the same way that people buy in “because everybody else is”, people are more likely to panic sell if they see their friends and family do the same:

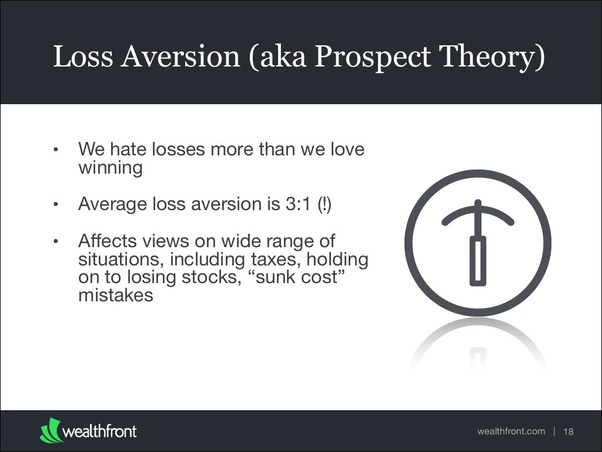

Others would say it is human nature, pure and simple, to care less about gains compared to avoiding losses.

Even though a loss and a decline isn’t the same thing of course and nobody loses money before they sell, and markets have always came back, that doesn’t always register in the moment.

Wealthfront have a good explanation of this theory, also known as Prospect Theory, below:

I think it is a combination of all of those things. One thing as do know is that people who don’t check their investment accounts often do better than everybody else.

That implies something. We are less likely to do anything, which is often the best thing once we have started investing, if we don’t think about it too much.

Do you mind lending money to family members with the risk of not being paid back?

Source: Quora

I do mine lending money to family and friends. I almost lost my closest friend at 18 over this issue.

Consider this startling fact – the chances of a complete stranger paying you back is 80%-90%, but friends and family only 50% in full.

Kind of ironic considering people are very suspicious of strangers (most people assume only 50% of strangers will repay) but not people closer by.

Don’t get me wrong, that is only a broad average and might not apply to your circle, but the reason is fairly simple.

On day one, everybody apart from sociopaths want to repay the money.

Not only do they want to repay and think it is a certainty, but they feel grateful.

Then things happen.

Simple example.

Let’s say you lend a cousin a few thousand. You bullied this cousin a bit when you were younger and kids. Pretty normal for kids but some people don’t forget.

You are now earning much more money than him. He comes to you looking for money.

The money is lent and your relationship is now strong, so both sides feel comfortable.

A few months later, he has only paid back a bit, and less than expected.

You approach him about it, and he feels angry. In this situation he might be able to justify his non-payment in the future.

You bullied him when he was a kid, and now you are being too assertive and not patient enough.

That is a simple example. I could have used hundreds but you get my point.

If you lend money online, and anonymously, to Gina from New York or Tom from Bradford in the UK, you can’t personalise that person much.

That is assuming they aren’t a celebrity or somebody famous. In this situation, it is hard to justify to yourself why you should refuse to repay to somebody who has never harmed you personally even in small ways.

So, I am not saying that people intentionally set out to not pay on day one, but it is easier to justify not repaying to somebody you know and might have “wronged you” in the past.

For the same reason, I suspect that less people would repay a very rich person like Bill Gates if he joined an online lending club, compared to an anonymous person, as they can justify it in their own mind, compared to an anonymous person.

In addition to that, even if they repay, your relationship can be strained for years.

Better to keep money out of family and personal relationships as much as possible.

If you want to lend money, you have a better chance of being paid back by joining some anonymous online community (like lending club) where you are matched with people who will need to repay with interest.

There are risks but less than borrowing to people you know.

Are you willing to take risk in the stock market?

Source: Quora

I am often asked what the biggest misconception is when it comes to investing.

The idea that the stock market is riskier than most investments, and keeping the money in cash, is probably number one.

Now, don’t get me wrong, you can make it risky if you want to.

How can you make it risky?

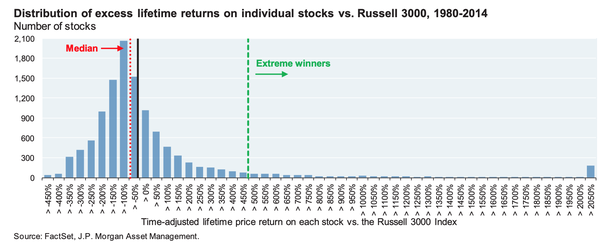

First by picking individual positions rather than invest in the whole market

As most stocks don’t beat the market as a whole, and a few extreme winners distort the average, your chances of beating MSCI World or the S&P500 over forty years is slim:

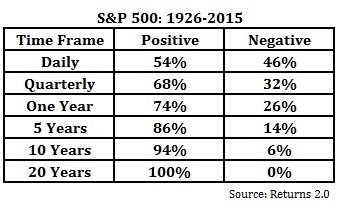

Second by being short-term

if you invest for one day it is very very risky

1 month – very risky, just less so than 1 day

1 year – very risky but much less so than 1 day

5 years – not very risky but considerable risk is there

10 years – not very risky at all. Small risk.

15 years – not risky at all

20 years – exceptionally low risk

50 years + from age 20 until death – so low risk, that if you are down, despite regularly investing, something is very wrong in the world. It would truly be unprecedented.

Third, you can panic every time the stock market crashes and sell out :

Basically, you can speculate. That is risky. You might be rewarded. You might pick the next Amazon, but you might also pick the next Lehman Brothers.

If you don’t do the things above, you would have to be exceptionally unlucky not to make money long-term.

The same can’t be said for assets like cash. Countless people have lost out with that historically.

It is also guaranteed to lose to inflation these days. It is just less volatile. That doesn’t mean it is less risky.

Further Reading

In the article below I looked at the following issues:

- What is the best way to invest $200000 for one year, or should you even reconsider investing for the short-term?

- Why shouldn’t you buy loads of luxury items if you become a millionaire?

- What are some reasons not to buy property during the coronavirus? I speak about numerous risks in the upcoming post-Covid world.

- Is investing 10% of your salary into the stock market a good idea? Assuming it is, is 10% enough for a comfortable retirement?

- Is mentality important for getting wealthy? If so, what kind of mentality is more likely to make you wealthy?

To read more click below