Canadian taxes are generally higher than US taxes, particularly when it comes to income and social contributions.

Getting a clear picture of Canadian taxes vs US taxes helps cross-border residents, investors, and anyone planning to relocate make informed financial decisions.

This article covers:

- Who pays higher taxes, Canada or the US?

- How high are property taxes in Canada?

- How much are property taxes in the US?

- Is there an exit tax if you leave Canada?

- Is there an exit tax when leaving the US?

- Is there a tax exemption in the US?

- What is exempt from tax in Canada?

Key Takeaways:

- Canada has higher income taxes, but provides universal healthcare and social benefits.

- Property taxes vary, with some US states exceeding Canadian rates.

- Both countries have exit taxes for high-net-worth individuals leaving the country.

- Tax treaties and exemptions can prevent double taxation for residents of both countries.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions.

The information in this article is not tax advice and may have changed since the time of writing. I can connect you with expert tax support for your specific situation.

Are Taxes Higher in Canada or the US?

Taxes are generally higher in Canada than in the US because federal and provincial taxes together often create a higher overall burden.

In contrast, the US has lower federal income tax rates, though some states impose significant additional taxes.

Canadian taxes also fund universal social benefits like healthcare and education, which partly explains the difference.

Overall, while some US states may have high taxes, Canada’s system typically results in higher average taxation for residents.

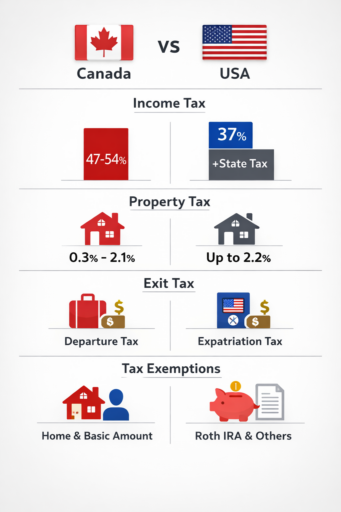

Are Property Taxes Higher in Canada or the US?

Property taxes are generally higher in the US than in Canada.

In the US, the average effective property tax rate across states is about 1.1% of a home’s value, with top states like New Jersey (~2.2%) and Illinois (~2.1%) among the highest in the country.

In Canada, property tax rates tend to be lower on average, with typical municipal rates ranging from roughly 0.3%–1.5% of assessed value in most cities.

For example, many cities like Vancouver average around ~0.30% while others like Fredericton and Saint John can be closer to 1.8%–2.1%, but overall Canadian rates remain lower than the highest US rates.

As a result, while some Canadian municipalities may approach US levels, most homeowners in the US face higher property tax bills on average, especially in high‑tax states.

Is Income Tax Higher in Canada or USA?

Income tax is generally higher in Canada than in the US once you combine federal and subnational taxes.

- Canada’s top federal rate is 33%, but when you add provincial taxes, combined marginal rates for high earners often reach roughly 47%–54% in provinces like Nova Scotia and Ontario.

- In the US, the federal top rate is 37%, and many states add additional income tax, but several states (e.g., Florida, Texas) have 0% state income tax, keeping total rates much lower for residents there.

Overall, most Canadians especially middle and high earners, face a higher combined income tax burden than most Americans due to provincial/state taxes and lower thresholds for top rates.

Do You Have to Pay an Exit Tax When Leaving Canada?

Yes, Canada imposes a departure tax when you cease to be a tax resident.

When you leave Canada, the Canada Revenue Agency (CRA) treats certain assets as if you sold them at fair market value the day before departure, which can trigger capital gains tax on the unrealized gains accumulated while you were a resident.

Only 50% of those gains are included in taxable income, though this rate can change based on current rules, and that amount is then taxed at your marginal rate.

The departure tax applies to most investments like stocks and mutual funds, but exemptions exist for things like RRSPs, TFSAs, and your principal residence.

Is There an Exit Tax in the US?

Yes, the United States also has an exit tax, but it applies only to certain covered expatriates.

Under Internal Revenue Code Sections 877 and 877A, US citizens who renounce their citizenship and long‑term residents, e.g., green card holders who held status for 8 of the last 15 years, may be subject to a mark‑to‑market expatriation tax on their worldwide assets.

To be a covered expatriate, you must generally meet at least one of these tests at the time you relinquish citizenship or residency:

- Net worth of $2 million or more.

- Average annual US tax liability exceeding about $211,000 for the five years preceding expatriation.

- Failure to certify compliance with US tax obligations for the previous five years.

If you are a covered expatriate, the IRS treats your worldwide assets as if sold at fair market value the day before expatriation, taxing unrealized gains above the 2026 exclusion of roughly $910,000 at US capital gains rates.

Not everyone who renounces US citizenship pays the exit tax — only those who meet the covered expatriate criteria — and if your net gain is below the exclusion threshold, you may owe nothing even if you are subject to these rules.

Are There Tax Exemptions in Canada?

Yes, Canada provides several tax exemptions and credits that reduce your overall tax burden. One of the most important is the Basic Personal Amount, which allows individuals to earn a set amount of income tax-free at the federal level.

Canada also offers credits such as the GST/HST credit, Canada Child Benefit, and various provincial tax credits that lower payable tax for eligible residents.

In addition, certain capital gains are exempt; most notably the principal residence exemption, which can eliminate capital gains tax when you sell your primary home.

Is There Any Tax Free in the US?

Yes, the US offers several tax-free income options and exemptions under federal and state law.

One of the most well-known is the Roth IRA, which allows qualified withdrawals in retirement to be tax-free if conditions are met.

Interest earned from most municipal bonds is also exempt from federal income tax, and sometimes from state tax if you reside in the issuing state.

In addition, homeowners can exclude up to $250,000 (single) or $500,000 (married filing jointly) in capital gains from the sale of a primary residence, provided ownership and use tests are satisfied.

State-level exemptions vary, meaning some residents may benefit further depending on where they live.

Can You Be a Tax Resident of Canada and the US?

Yes, you can be considered a tax resident of both Canada and the US at the same time.

This typically happens because the US taxes based on citizenship (and green card status), while Canada taxes based on residency ties and physical presence.

As a result, a US citizen living in Canada, or someone who meets residency thresholds in both countries, may have dual tax filing obligations.

The Canada–US Tax Treaty contains tie-breaker rules and foreign tax credit provisions that help prevent double taxation by allocating taxing rights and allowing credits for taxes paid in the other country.

Top Tax Hotspots in Canada and the US

Taxes in both Canada and the US vary dramatically based on where you live, making location a key factor in overall tax liability.

In Canada, provinces like Nova Scotia and Quebec have some of the highest combined federal and provincial income tax rates, often exceeding 50% for high earners.

In contrast, provinces like Alberta offer a flat provincial rate of 8%, making the total tax burden significantly lower for residents with similar incomes.

In the US, state taxes range from 0% in states like Florida, Texas, and Wyoming to over 13% in California for top earners.

Property taxes also differ widely. New Jersey averages 2.23% of home value, while some Canadian cities, like Vancouver, average only 0.3%, though smaller municipalities in Atlantic Canada can reach 1.8%–2.1%.

Other local levies, such as sales taxes, further affect the net cost of living.

For example, Quebec has a combined GST/HST and provincial sales tax of 14.975%, while several US states have no state-level sales tax at all, and others like Tennessee charge 9.55% in some cities.

Understanding these tax hotspots helps individuals and businesses plan strategically.

Choosing the right province or state can save tens of thousands of dollars annually, particularly for high-income earners, property owners, or those with significant investment income.

Even small differences in marginal rates, property taxes, and local levies can add up over time, making location a crucial part of tax optimization in both Canada and the US.

Conclusion

When comparing Canadian taxes vs US taxes, the real difference isn’t just how much you pay. It’s how each system is designed.

Canada leans toward higher taxation paired with broader public benefits, while the US offers more variation by state but maintains strict worldwide taxation for its citizens.

For cross-border individuals, the stakes are higher than simple rate comparisons. Residency status, reporting obligations, asset structure, and timing of a move can significantly affect your net outcome.

A poorly planned relocation can trigger departure taxes, expatriation taxes, or dual filing burdens that outweigh any expected savings.

The key insight is this: tax efficiency between Canada and the US is highly individual.

The better system depends on where you earn, where you invest, where you live long term, and how your wealth is structured.

Strategic planning, not geography alone, ultimately determines the tax result.

FAQs

Why is Canadian Income Tax So High?

Canadian income tax is higher because it funds universal programs like healthcare, education, and social services.

Provincial taxes also add to the federal rate, making the combined rate higher than in most US states.

Do I Have to Pay Canadian Taxes if I Live in the US?

If you are no longer a Canadian resident, you generally do not pay Canadian taxes on worldwide income, but you may be taxed on Canadian-source income like rental property or investments.

How to Avoid Double Taxation Between the US and Canada?

You can avoid double taxation by relying on the Canada–US Tax Treaty and claiming foreign tax credits for taxes paid in the other country.

Proper filing in both jurisdictions is essential to ensure the same income is not taxed twice.

Do I Have to File Taxes Both in the US and Canada?

Yes, if you have income or assets in both countries, you may need to file taxes in both Canada and the US, even if you claim exemptions or credits to reduce double taxation.

Is It Cheaper to Live in the US or Canada?

The US is generally cheaper from a tax perspective, but overall living costs vary by city and region.

Canada has higher taxes that fund public healthcare and social benefits, while in the US many costs like healthcare and retirement are paid privately.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.