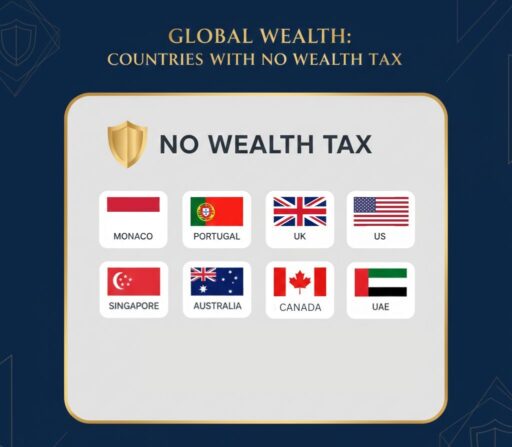

Countries like Monaco and Portugal do not impose a wealth tax, which makes them attractive for high-net-worth individuals and expats.

Countries with no wealth tax allow residents to preserve more of their assets while benefiting from favorable tax systems.

This article covers:

- What is a wealth tax?

- Which European countries have no wealth tax?

- What are the wealth tax-free countries in Asia?

- What country has the lowest taxes for the rich?

- What are the negatives of taxing the rich?

Key Takeaways:

- Countries like Monaco, UAE, and Portugal have no wealth tax.

- Wealth tax can reduce inequality but may discourage investment.

- Even without wealth tax, other taxes like income or property tax may apply.

- Regional differences matter: some areas in Spain and Portugal are tax-friendly.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions.

The information in this article is not tax advice and may have changed since the time of writing. I can connect you with expert tax support for your specific situation.

What is the meaning of wealth tax?

A wealth tax is an annual tax imposed on an individual’s net assets, including cash, investments, property, and other valuables.

Unlike income tax, which targets earnings, wealth tax focuses on the total accumulated wealth.

Governments implement this tax to reduce economic inequality, generate revenue for public services, and encourage more active use of capital.

It is often controversial, as it can influence investment decisions, impact high-net-worth individuals, and sometimes lead to capital flight if rates are perceived as too high.

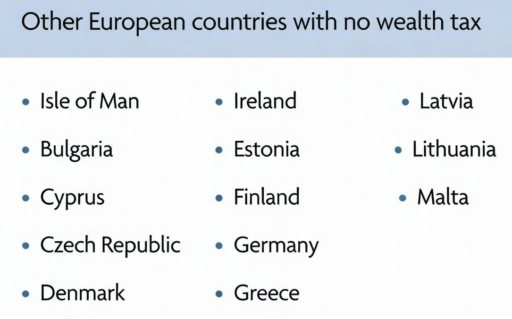

List of countries with no wealth tax

No wealth tax countries like Monaco, Portugal, and Singapore are highly attractive for high-net-worth individuals and investors seeking to preserve their assets.

Across the globe, several nations have either abolished wealth tax or never implemented it, each with unique tax structures and benefits.

Here’s a regional breakdown:

Europe

- Monaco – Residents pay no wealth or personal income tax, attracting global elites. Its favorable tax system is combined with a luxurious lifestyle and strategic location.

- Portugal – Portugal does not impose a wealth tax, though property taxes may still apply on real estate holdings.

- United Kingdom – There is no formal wealth tax, but high-net-worth individuals may still be subject to inheritance tax and capital gains tax.

- France – France abolished its broad annual wealth tax (ISF) in 2018 and replaced it with a real estate‑focused wealth tax (IFI) that applies only to property assets above a threshold (around €1.3 million) with progressive rates historically from roughly 0.5 % to 1.5 %. As of 2026, reforms are underway to expand the tax base and move toward a simplified structure, but personal wealth outside real estate generally remains untaxed in France.

- Austria – Wealth tax abolished decades ago; no recurring net wealth tax.

- Belgium – No traditional wealth tax on total net assets (though some taxes on certain securities accounts exist).

- Netherlands – The Netherlands does not have a traditional wealth tax on total net assets. Instead, it taxes a deemed return on savings and investments (Box 3) above a certain threshold, effectively applying a modest wealth-related levy while classifying it under income tax rather than a standalone wealth tax. Reforms from 2028 will switch to taxing actual investment returns, but total wealth itself remains untaxed.

North America

- United States – Wealth is generally taxed through income, capital gains, and estate taxes rather than a direct annual wealth tax. The absence of a wealth tax, combined with a robust investment market, attracts affluent investors.

- Canada – No federal wealth tax exists, and while the topic has been discussed in political and economic debates, no formal wealth tax law has been enacted; provincial governments tax income and specific assets instead.

- The Bahamas – No personal wealth tax exists, nor income, capital gains, or inheritance tax. Residents benefit from minimal personal taxation, making it a popular choice for wealthy expatriates.

- Costa Rica – Costa Rica does not levy a wealth tax. Its tax system focuses on income and property.

Asia

- Singapore – No wealth tax is levied, and income taxes are relatively low. This policy, combined with business-friendly regulations, makes Singapore a top destination for global investors.

- Hong Kong – Wealth tax does not exist, and personal income taxes are capped at low rates.

Oceania

- Australia – Wealth tax was abolished decades ago. Residents only face income tax, capital gains tax, and property taxes, providing clarity and simplicity for financial planning.

- New Zealand – New Zealand has never implemented a general wealth tax on total net assets. Its tax system focuses on income and property taxes. While no wealth tax exists today, some political parties and advocacy groups have proposed introducing one, though no legislation has been enacted.

Middle East

- United Arab Emirates – No personal income or wealth taxes exist. Combined with free trade zones and residency programs, it has become a magnet for wealthy expatriates.

- Qatar and Bahrain – Similarly, these countries impose no wealth tax, focusing instead on indirect taxes like VAT and business-related fees.

These countries often pair the absence of wealth tax with other favorable conditions, such as low income taxes, investment incentives, and economic stability, making them prime locations for global investors and wealthy expats.

What country has the lowest taxes for the wealthy?

Countries like Switzerland and Norway are known for taxing wealth lightly.

Some other countries also levy wealth taxes but keep rates relatively low or offer high exemptions, balancing revenue needs with competitiveness.

- Switzerland – Wealth tax is charged at the cantonal and municipal level rather than federally, and rates are generally low (often well under 1%), with thresholds that keep many moderate‑wealth households below taxable levels.

- Norway – Norway’s net wealth tax is around 1% to 1.1% on individual net assets exceeding the threshold, making it modest compared with deeper wealth taxes historically seen in some countries.

- Spain – Spain’s wealth tax ranges from roughly 0.2% up to around 3.5%, but some regions like Madrid and the Andalucia offer full exemptions, effectively reducing the burden to zero for residents there. Other autonomous communities provide partial reliefs, so the effective tax can vary widely depending on location.

- Luxembourg – Luxembourg does not impose a personal wealth tax on individuals, but resident companies and branches of non‑resident companies are subject to a corporate net wealth tax. The standard rate is 0.5% of net assets up to €500 million, with a reduced rate of 0.05% on the portion above €500 million. Additionally, companies face a minimum net wealth tax based on their total balance sheet (e.g., approximately €535, €1,605, or €4,815 depending on size) even if calculated tax is lower.

- Colombia – Colombia has introduced a temporary wealth tax under Decree 1474 of 2025, effective for assets held on or after January 1, 2026. The tax applies to individuals with net assets exceeding 40,000 UVT (≈ COP 2 billion), with a progressive rate starting at 0.5% and rising to 5% on assets above 2,000,000 UVT. This emergency measure expands the taxpayer base and temporarily increases the top rate compared with previous years, while other usual taxes like income and property continue to apply.

Why is taxing the rich beneficial?

Taxing the wealthy provides governments with funds and tools to support society and the economy.

It can:

- Generate revenue for public services like healthcare, education, and infrastructure.

- Reduce income inequality by redistributing wealth.

- Encourage broader economic growth through funding social programs.

However, these benefits hinge on implementation and economic context, as poorly designed wealth taxes can discourage investment or cause capital flight.

What are the downsides of taxing the rich?

High taxes on the wealthy can drive them to move to countries with lower taxes. Other potential disadvantages include:

- Wealthy individuals may relocate, reducing the domestic tax base.

- Complex reporting and compliance requirements can increase administrative costs for both taxpayers and governments.

- High tax rates may discourage investment, entrepreneurship, or business expansion.

Careful design is needed to balance fairness with maintaining incentives for economic growth.

Other Taxes to Consider Aside from Wealth Tax

Even in countries with no wealth tax, other taxes may affect the wealthy, such as:

- Income tax – Taxed on salaries, dividends, or capital gains.

- Inheritance tax – Levied on estate transfers after death.

- Property tax – Based on real estate holdings.

- Capital gains tax – Applied on the profit from selling investments.

Understanding the full tax landscape is essential before relocating or investing abroad.

Historical Trends and Abolished Wealth Taxes

Wealth taxes have been part of the global tax landscape for decades, especially in Europe, but many countries that once embraced them have since rolled them back or significantly reformed them.

At the same time, some nations today are considering wealth tax proposals, illustrating a dynamic tug‑of‑war between revenue needs, mobility of capital, and political goals.

1. Why Wealth Taxes Emerged in the First Place

After World War II and through much of the 20th century, many countries adopted wealth taxes as instruments to:

- Reduce inequality by levying annual charges on accumulated assets.

- Raise revenue during reconstruction and welfare expansion.

- Limit concentrated fortunes from dominating political and economic influence.

In this climate, wealth taxes appeared equitable and practical, at least in theory.

2. Administrative and Economic Hurdles That Led to Abolition

Over time, several fundamental challenges emerged:

- Valuation complexity: Accurately valuing assets (especially privately held business interests or real estate) proved administratively burdensome.

- Capital mobility: Wealthy individuals could legally relocate to jurisdictions with no wealth tax, reducing the local tax base.

- Compliance cost: The costs of reporting, auditing, and enforcement often outweighed revenue gains.

These issues were central to reforms in countries that abandoned wealth taxes.

3. Key Examples of Repeal and Reform

France:

- Abolished in 2018, replaced by the Impôt sur la Fortune Immobilière (IFI) — a tax only on real estate assets above a threshold.

Germany:

- Phased out its wealth tax due in large part to constitutional and valuation challenges.

Austria:

- Eliminated its wealth tax decades ago, shifting toward simpler income and property taxation without annual net‑worth levies.

Together, these shifts illustrate why many developed economies moved away from traditional wealth taxation.

4. Renewed Interest in Wealth Taxes

While some countries repealed wealth taxes, a new wave of discussions and proposals has arisen in recent years, largely in response to rising inequality and fiscal pressures:

- Colombia (2026): Under emergency legislation (Decree 1474 of 2025), Colombia introduced a progressive wealth tax on individuals.

- Canada: While no wealth tax has been enacted, policy debates and proposals have resurfaced periodically, with some experts arguing for a levy on top fortunes to fund public services.

- New Zealand: Several political parties and advocacy groups have put forward proposals for a wealth tax, though none have become law.

- Other economies from parts of Latin America to some Nordic think‑tanks, periodically revisit the idea as inequality debates intensify.

This contrast underscores how wealth taxation remains a live policy topic, not a settled chapter.

5. What This Means for High‑Net‑Worth Individuals Today

Understanding historical trends alongside current proposals helps wealthy individuals and advisors:

- Anticipate policy risk: Even in wealth‑tax‑free jurisdictions, proposals can arise (as seen in Canada and New Zealand).

- Evaluate tax mobility: Countries that abolished wealth taxes often compensate with other attractive features (e.g., low capital gains, residency incentives).

- Plan proactively: A nuanced approach combining jurisdiction choice, asset structuring, and compliance strategies, tends to outperform simple tax avoidance mindsets.

Conclusion

Wealth isn’t just about what you earn; it’s about how it’s preserved, grown, and protected.

Countries with no or low wealth taxes offer more than just fiscal relief; they provide choices, flexibility, and leverage for high-net-worth individuals.

But the smartest strategies go beyond chasing low rates. They consider stability, regional differences, and long-term financial planning.

In the end, understanding the full landscape of taxes, incentives, and regulations is what separates opportunistic decisions from truly sustainable wealth management.

FAQs

Which is the most tax-free country?

The Bahamas, Monaco, and United Arab Emirates rank among the most tax-free countries for individuals, offering no personal income or wealth taxes.

Who is richer, Spain or Portugal?

In terms of GDP per capita and wealth distribution, Spain has a higher average wealth than Portugal.

However, both Spain and Portugal are attractive to expats due to lifestyle and regional tax benefits.

Why did France get rid of wealth tax?

France abolished its wealth tax in 2018 to reduce capital flight, encourage investment, and simplify the taxation system.

Where in Spain is there no wealth tax?

Some autonomous regions like Madrid and Andalucia offer a 100% exemption on the regional wealth tax, meaning residents there effectively pay no regional wealth tax on their assets.

However, ultra‑high‑net‑worth individuals may still owe the national Solidarity Tax on Large Fortunes if their wealth exceeds defined thresholds.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.