A detailed guide for understanding credit score – that will be the topic of today’s article.

Understanding your credit score is essential for effective global credit management to ensure financial stability.

If you are looking to invest as an expat or high-net-worth individual, which is what I specialize in, you can email me (advice@adamfayed.com) or WhatsApp (+44-7393-450-837).

Introduction

One of the major problems faced by a lot of people these days is their credit score.

Why are people facing such issues when it comes to credit scores? What exactly is a credit score and how is it calculated? What are the most important aspects related to a person’s credit score?

These are among the common doubts that arise among people while talking about credit scores. Especially when a person is new to such topics and doesn’t know much about how they work.

What is a Credit Score?

To begin with, a credit score is a number that determines the creditworthiness of a person.

Creditworthiness refers to a person’s ability to pay back a loan if approved.

Let us have a more detailed insight into the definition for having a better understanding of how they work.

Imagine you are trying to get a loan from a lender, let’s say a personal unsecured loan.

Loans such as mortgages are backed by the very property which you intend to buy with the loan.

But when it comes to personal loans, they are unsecured and don’t need any collateral.

In such a situation, how can a lender know that you will pay back the loan you borrow?

That’s why a credit score will determine your ability to pay back the loan you acquire.

Not just unsecured loans, but even some secured loans like a mortgage have credit score requirements.

Most financial institutions, make loan-related decisions based on an individual’s credit score.

Some of the most common loans and debts that require a credit score are Loans, Credit Cards and Mortgages

In some countries, credit score is often considered when they rent a property as well.

Credit History

In layman’s terms, credit history is the history of your debt repayments like loans or credit cards.

In detail, an individual’s credit history consists of the following information.

— The number of debt accounts a person has, which includes both open and closed accounts.

— The categories of those accounts, such as instalment credit, revolving credit, etc.

— The amount an individual owes for each account or used to owe for a closed account.

— An individual’s payment history. This is used to determine whether the borrower has made timely payments when it comes to repaying the debt.

While calculating the payment history, there will be negative points for not making timely payments.

The payment history will also include delinquencies, loan defaults, etc., (if any).

The credit history of a person is considered in many cases such as a loan, job or while renting an apartment.

People with a long credit history as well as responsible credit use have higher credit scores.

Credit Reports

We’ve covered credit scores and credit history, but what is a credit report?

A credit report acts as an insight into an individual’s credit history, basically to provide a reference for lenders.

Credit reporting bureaus are responsible for generating a credit report, and these bureaus vary depending on a person’s nation.

So, how will it help lenders to determine a person’s creditworthiness?

This credit report will consist of useful data to calculate a person’s creditworthiness. Usually, a credit report contains:

— Credit history

— Balance loan amounts

— Loan amounts related to all the open and closed debt accounts

If you want to get your credit report, you can obtain it by reaching out to a credit reporting bureau.

Credit Reporting Bureaus

Credit Reporting Bureaus are also known by other names like Credit Bureaus, Credit Reporting Agencies, etc.

It is a business which handles all the credit-related information of a person.

How can a credit reporting agency get hold of a person’s credit history?

Generally, when you get a loan, the lender will send that information to these bureaus.

All the information received in this way will be combined and made into a credit report.

This credit report would also consist of the credit score, which is used to determine creditworthiness.

A credit reporting agency will maintain all the credit information about a person.

Most lenders partner up with credit reporting agencies for two major reasons.

The first one is to get the details of potential customers who have better credit reports.

Another reason is to allow individuals access to a soft credit check during the pre-qualification process.

For example, let us imagine that you are seeking a loan from a lender for a certain amount. You are not sure whether or not you’ll qualify or if the loan terms are favourable to you.

In such scenarios, you can opt for a pre-approval process that determines these aspects. During this pre-qualifying process, your credit score will not be affected.

However, some lenders do a hard credit check, which can damage your credit score.

How is a credit score calculated?

There are several factors taken into consideration while calculating a credit score.

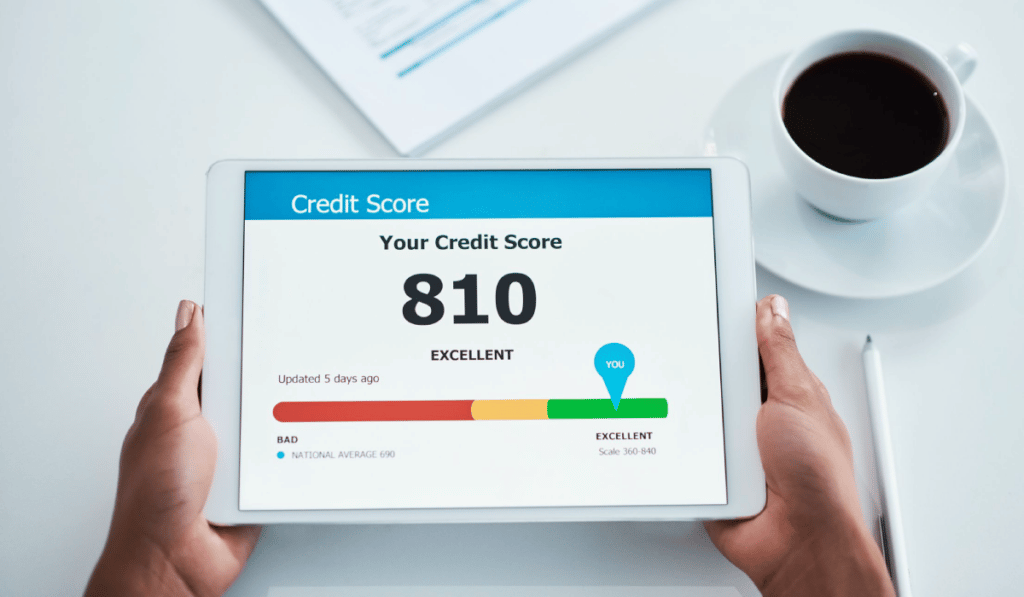

A credit score is a three-digit number that determines a person’s creditworthiness based on their credit report.

In most countries, the number lies between 300 to 900, while higher scores mean higher creditworthiness.

Those with a higher credit score can easily get qualified for various debts like loans or credit cards. That too, with the lowest possible interest rates.

To generate a credit score, the requirements are pretty much the same as those of credit reports. They are:

— Your payment history

— Your current unpaid debts

— Number of loan accounts

— Types of loan accounts

— The duration of loan accounts

— The time for which the loan account has been open

— Available credit limit

— Credit utilization

— New loan applications

— New credit card applications

— A person’s debt, which has been sent to collection (if any exists)

— A person’s foreclosure history (if any exists)

— A person’s bankruptcy history (if any exists)

All of these aspects will be combined into five major factors while calculating a credit score. Such as:

— Payment history

— Credit history

— Credit utilization rate

— Types of credit

— New credit

Credit Utilization is often called by the names Credit Utilization Rate or Credit Utilization Ratio.

This refers to the credit being used by an individual divided by the credit amount they have available.

In simpler terms, the credit utilization rate is the debt amount of an individual divided by the credit limit.

A good credit utilization rate would not exceed 30%, whereas a 10% rate would be deemed excellent.

A person can have different credit scores, which depend on the credit scoring model used.

Although they may vary based on the credit scoring model, there won’t be too much of a difference.

For example, let’s say your credit score was around 700 when you checked with one agency.

If you check it somewhere else, where another credit scoring model has been used, you’ll have 690 or 710. You won’t see 550 or 800 as that much variation won’t be possible.

Credit Scoring Models

A credit scoring model is an analytic approach for calculating a person’s creditworthiness.

All the statistical data of a person is received by credit agencies, which are analysed to generate a credit score.

We already discussed the factors taken into consideration while calculating a credit score.

Let us have a look at the FICO scoring model, which is one of the common scoring models in the US.

Let us look at how much each different factor influences your credit score during calculation. This is according to the FICO scoring model and may differ from other credit scoring models.

— Payment history (35%)

— Credit utilization (30%)

— Credit History (15%)

— Credit use (10%)

— New credit (10%)

The scores offered by FICO range from 300 to 850 and based on the score they have different terms.

If we consider the FICO credit score, the credit scoring is between 300 to 850.

When the credit score is above 800, then the individual is said to have an “excellent” score.

Any score that falls between 740 and 800 would be suggested as a “very good” score.

Those who have a credit score of 670 to 739 are considered “good” scores, and most people have this.

A score between 580 and 669 is deemed as a “fair” score, which is also manageable.

Those who have scores between 300 and 579 are considered to have a “poor” score and may miss out on beneficial interest rates.

Furthermore, such people may find it very hard to secure a loan as they don’t seem creditworthy to lenders.

However, Vantage Scores are based on a different approach, which has been provided below.

— Payment history (41%)

— Type of credit (21%)

— Credit utilization (20%)

— Total balances (11%)

— Recent credit behaviour (5%)

— Available credit (3%)

The credit scores range from 300 to 850 for the Vantage scoring model as well.

300 to 499 (very poor)

500 to 600 (poor)

601 to 660 (fair)

661 to 780 (good)

781 to 850 (excellent)

There are some other credit scoring models in the US, and they have different methods for calculating this score.

Vantage score used to have scoring models with ranges up to 990. However, as per Experian, the newer credit scoring models use a range of 300 to 850.

Some of the common credit scoring models in the US apart from Vantage Score and FICO are:

— TransRisk

— Experian’s National Equivalency Score (0 – 1,000)

— Credit Xpert Credit Score

— CE Credit Score (330 – 830)

— Insurance Score (200 – 997)

Major Credit Bureaus (The Big Three)

In the US, the major credit reporting agencies are Equifax, Experian, and TransUnion.

In the UK, credit bureaus may also be called Credit Referencing Agencies.

There are four major credit referencing agencies in the UK, which include the three in the US and another one called Crediva.

Equifax, Experian, and TransUnion are known as the “Big Three” and offer services in various countries.

Experian offers services in 43 countries in North America, Latin America, Ireland, and EMEA.

TransUnion provides services in more than 30 countries while covering five continents.

Equifax is known to exert its presence in 25 countries worldwide, which includes some of the major countries.

Not just in the US, but the credit scores differ for each bureau in any country. This is because of the varying credit scoring models they make use of.

Credit Rating

We now understand that credit scores are provided by credit bureaus to determine a person’s creditworthiness.

Some people often use the terms credit score and credit rating interchangeably.

It is a misconception as the two terms are different although they have the same use and meaning.

Credit ratings are for businesses or governments just like credit scores are for individuals.

Just like credit bureaus offer credit scores, credit ratings are provided by credit rating agencies.

For individual credit scores, the Big Three were Equifax, Experian, and TransUnion.

However, the Big Three credit rating agencies are S&P Global Ratings, Moody’s, and Fitch Group.

Usually, the credit rating would be an alphabetical (which may include numbers) rating and is provided to borrowers like:

— Corporate entities

— States

— Provincial authorities

— Sovereign governments

— Other similar entities or authorities

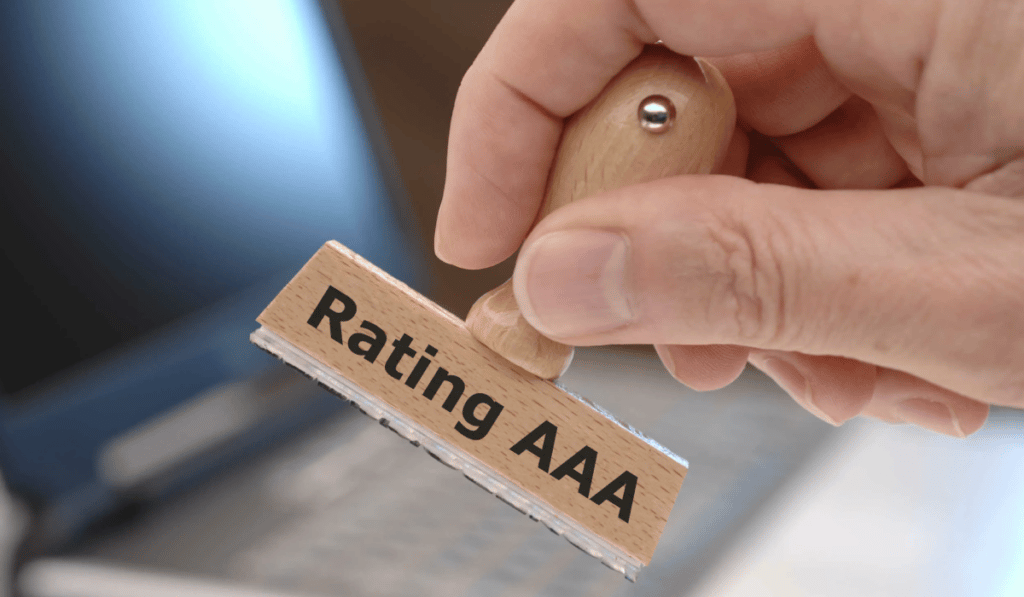

For instance, bonds issued by companies or governments are generally provided with a credit rating. This rating will be provided alphabetically ranging from AAA to D.

To have a better understanding, let us have a look at the credit ratings at S&P’s long-term credit rating scores.

They range between:

• AAA

• AA+

• AA

• AA-

• A+

• A

• A-

• BBB+

• BBB

• BBB-

• BB+

• BB

• BB-

• B+

• B

• B-

• CCC+

• CCC

• CCC-

• D

If a country or an entity is given a rating of AAA, then it is creditworthy and can be trusted financially.

The ratings, therefore, go on until D, which is considered to be a very poor rating. A country or an entity with a credit rating of D is likely to default on financial obligations.

On the other hand, short-term credit ratings range from ‘A-1+’ to ‘D’ while ‘A-1+’ is the best and ‘D’ is the worst.

If we talk about Moody’s, the credit rating scale is from Aaa to C, which is as follows.

• Aaa

• Aa1

• Aa2

• Aa3

• A1

• A2

• A3

• Baa1

• Baa2

• Baa3

• Ba1

• Ba2

• Ba3

• B1

• B2

• B3

• Caa1

• Caa2

• Caa3

• Ca

• C

A credit rating of Aaa by Moody’s is considered great, while C is generally a poor rating.

The credit rating scale of Fitch is almost the same as that of the credit rating scale of S&P. However, instead of CCC+, CCC, and CCC-, Fitch has a CCC rating.

Based on the entity or country, there are different types of credit ratings.

Sovereign Credit Ratings

This is the credit rating used to determine the creditworthiness of a country.

Sovereign credit rating is mostly used to assess the risk involved with bonds issued by a country.

Grades of BBB- or higher are provided to countries which are said to be investment grade.

Whereas the grades of BB+ or lower would generally mean speculative or junk grade, and this is according to the S&P.

If we consider Moody’s, a rating of Baa3 or higher is considered investment grade. Anything that begins with Ba1 and falls under it will be considered speculative.

Corporate Credit Ratings

As the name itself suggests, corporate credit rating is the rating provided for companies.

Corporate credit ratings are reviewed by investors while determining the risk involved with corporate bonds.

Just like the sovereign credit ratings, a higher credit rating would mean investment grade and the lowest would mean junk grade.

Short-Term and Long-Term Credit Ratings

The credit ratings are also provided on the basis of the time horizon being considered.

Any rating provided for a time horizon of one year or less would be called a Short-Term Credit Rating.

Vice versa, a Long-Term Credit Rating is provided for time horizons exceeding one year.

The short-term credit rating scale usually differs from that of a long-term credit rating scale.

For instance, we already discussed the long-term credit rating scale used by the big three.

Now let’s have a look at the short-term credit rating scale used by the big three.

For Moody’s:

— P-1

— P-2

— P-3

— Not Prime

For S&P’s:

— A-1+

— A-1

— A-2

— A-3

— B

— C

— D

For Fitch’s:

— F1+

— F1

— F2

— F3

— B

— C

— D

Just like the long-term rating scale, the short-term scale also starts with the “best in the beginning” order.

Having said that about the credit ratings, now, let’s get back to our main topic “credit scores”.

How to Improve Credit Score?

Before getting to how to improve your credit score, let us take a moment and discuss why you should do it.

As you may already know, a good credit score will often be beneficial for getting low interest rates.

As it determines your creditworthiness, having a higher credit score will make you look trustworthy to lenders.

Therefore, it is very important for a person to have at least a good credit score to appear creditworthy.

Now let us discuss how you can enhance your credit score, especially if you have a bad score.

Study your credit reports

The first thing you are required to do is to have a detailed review of your credit reports.

This will let you have a better understanding of how good or bad your credit situation is.

You can obtain a credit report from one of the big three bureaus, and the process takes up to three hours.

While pulling your credit report, make sure that you opt for a soft credit inquiry.

If you are in the US, you can get a free report from each of the bureaus every year.

Bill payments

Payment history often plays a key role during the calculation of your credit score.

Because of this reason, it is wise to clear existing debts on your report, such as education loans.

Adding to that, keep track of your bill payments and always opt for timely payments.

You can alternatively go ahead with automatic bill payments so that you won’t forget any bills.

To improve your credit score, you must use your credit card for making all the payments.

While doing so, make sure that you pay off the credit card debt on time, so that your credit score has an improvement.

Credit Utilization

Remember? It is always better to have a credit utilization rate of at least 30% for a better score.

If you manage to bring it to 10% or so, it can be highly advantageous for boosting your score.

You can set a high balance alert for your credit card to know when credit utilization is increasing.

Alternatively, you can ask for an increase in your credit limit, which can also improve credit utilization.

Avoid new credit cards and loans for a while

Another important step is to avoid getting new credit cards or loans until your credit score improves.

If you get a new loan or a credit card, your credit utilization rate increases, which is bad for your score.

Simultaneously, hard credit inquiries also have a negative impact on your credit score. Therefore, always make sure that you are going through a soft credit inquiry unless it is necessary.

Credit file management

Most people nowadays often face issues because of having a thin credit file.

This usually indicates that such people do not have enough credit information for generating a score.

There are certain programs such as Experian Boost or Ultra FICO. Such programs allow a credit file to include information such as banking history, bill payments, etc.

Through these programs, you can overcome the problem of having a thin credit file.

There are some other options for renters such as rental Kharma or RentTrack.

These report your rent payments to the credit bureaus to deal with the issue of a thin credit file.

Old accounts and delinquencies

Most people don’t know that older credit accounts can improve the credit score of a person.

So, don’t close your old accounts as it may lower your credit limit.

If you keep such accounts open, the available credit won’t be decreased and your credit utilization will be improved.

Additionally, pay attention to delinquent accounts or collection accounts if any exist.

Such accounts have a massive impact on your credit score making it very hard to improve.

If you are not able to clear them off in a single go, then you can always create a plan.

Cut down on a few things and create a budget plan that’ll assist you in clearing such debts.

Negative accounts are said to have an impact for at least seven years and bankruptcy for 10 years.

Debt Consolidation

Debt consolidation is often a great idea for clearing a number of various loans.

This often allows an individual to bring various loans of different interest rates under a single roof. Mostly at a lower rate.

This will come in handy while improving your credit score as it decreases your credit utilization.

There are certain credit cards known as Balance Transfer Credit Cards, which also serve the same purpose.

The interest rates for such cards come with a promo period where the interest rate is 0% during then. However, be on the lookout for transfer fees that can be around 3 to 5% of the amount being transferred.

Credit Monitoring

Credit monitoring services, also called credit repair services, help improve your credit score.

Credit monitoring services provide various services which even include protection from identity fraud.

Secured loan

If you have a property or an asset that can be kept as collateral, you can get a secured loan.

Such loans will help you build credit while coming with low interest rates and higher amounts.

Bottom Line

Most probably, there is no person who never gotten involved with debt at least once in their lifetime.

Getting a loan can be very essential during times of financial difficulties, and not being able to get one makes the situation hard.

You can always have a plentiful cash reserve so that you can avoid the necessity of getting a loan.

Furthermore, you can even invest money to get returns, which can make your financial situation better.

Are you actively looking for someone who can attend to your investment needs?

Do seek an expert who is efficient when it comes to financial planning or wealth management?

Don’t worry. I’m here to help.

You can get access to the top-notch services that I offer my clients, which help one achieve financial freedom.

Don’t hesitate to contact me if you want to whether or not you can benefit from the best-in-class services I offer.

Have a good day!

Pained by financial indecision? Want to invest with Adam?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.