I often write on Quora.com, where I am the most viewed writer on financial matters, with over 666.5 million views in recent years.

In the answers below I focused on the following topics and issues:

- Why do rich people keep most of their wealth in assets instead of cash?

- What is an easy way to get a 32% return?

- Why do some experts believe that China’s market performance will pick up in the coming months?

- Which businesses have the least chances to fail?

- What makes you the most mad about today’s economy?

- What aspect of modern life is most overrated?

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Some of the links and videos referred to might only be available on the original answers.

Why do rich people keep most of their wealth in assets instead of cash?

There are numerous reasons:

1.Assets create cashflow

If you invest in assets, you will either make more cash straight away (through a fixed return or dividends) or you will be able to accumulate and then make more cash long-term.

So, it isn’t “assets vs. cash”. It is more a case of assets creating more cash long-term.

2. Prior experience

Most wealthy people have made money from putting cash to work, for example by starting a business.

Most highly-paid salary workers also only got to that position by investing in things like education, which together with experience, helped them get promotions.

So, it logically follows that cash should be put to work.

3. Risk

Cash has more risk than assets, at least if you do it correctly, which means:

- Being long-term

- Having diversification.

It is true that having 100% of your assets in one stock or bond isn’t safe.

Yet holding assets in different baskets for the very long term is.

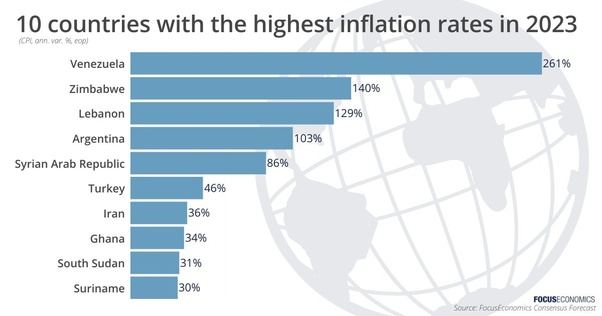

Inflation is a huge risk.

I saw this on Twitter recently:

This doesn’t even factor in the fact that the banks defaulted in places like Lebanon.

Over the last hundred years, most countries have seen at least one period of high inflation or bank failures which governments couldn’t insure against.

Which businesses have the least chances to fail?

Any business that few others want to do.

An example is laundromats and launderettes

This kind of business is:

- Essential for some people, such as businesses

- Not that difficult to set up

- Not overly complicated or regulated

- Not glamorous so few want to do it

- Quite resilient to recessions.

- Not easily affected by new technologies

- Not very capital-intensive.

Some studies show that they have a success rate of over 90%.

Of course, though, one of the reasons for such a high success rate could be that very pragmatic people set up such businesses to begin with.

The same can be seen in trash businesses. They have a low failure rate.

Of course, if you have experience in any industry, that is also a great way to start a business that is less likely to fail.

It is more difficult to fail if you have contacts, experience and clients you can move across.

What is an easy way to get a 32% return?

32% per year or over several years?

Every year is almost close to impossible.

If you start with just $100,000 and get 32% per year for 40 years, you will have $ 30 billion….from a 100k investment!

If you also add 20k a year in those 40 years, you would have 47 billion!

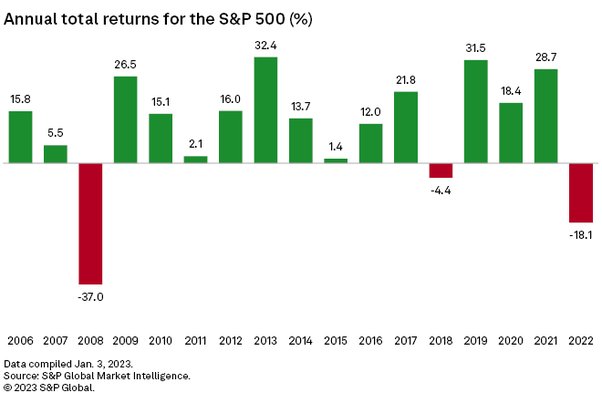

The S&P500 has been one of the best investments historically.

Yet as per the S&P 500 global stats, it has seldom made 32% over a year.

Getting 32% over several years is much easier.

A compounded average rate of return of 8%-10% per year will be a total return of thousands of percentage if you do it for decades.

There are many cases where multi-million dollar or Pound fortunes have been made gradually over decades, by investing relatively small amounts of money.

That is why Einstein referred to compounded interest as the world’s eighth wonder (source AZ Quotes)

An alternative is private investments.

For instance, if you start your own business, you can make 32% per year on investments, but not forever.,

And it is riskier and indeed not easy.

Why do some experts believe that China’s market performance will pick up in the coming months?

There are a few reasons why China’s stock market could do well.

Firstly, the Chinese economy is struggling. Almost for sure, the figures are much worse than the government’s official stats, as Larry Summers and others have mentioned.

In a one-party state, never trust the statistics! We saw that during Covid-19, as well as the recent announcement that the government would stop collecting data on youth unemployment.

The upside of this is that the government might need to stimulate the economy.

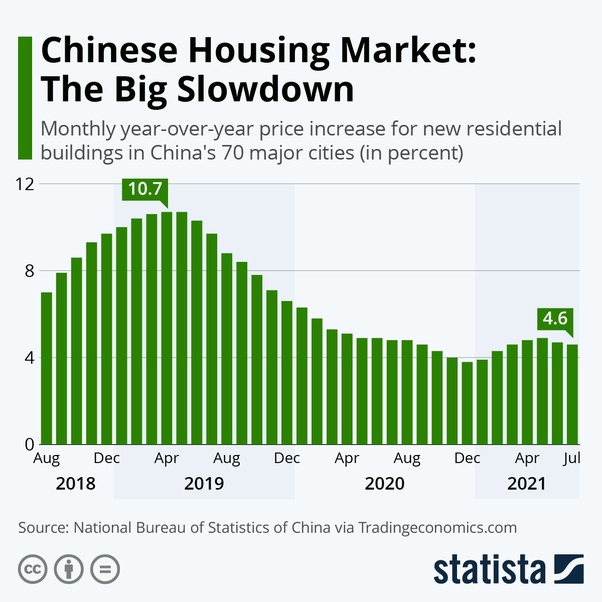

What is more, China’s real estate sector is struggling.

As per the below stats from Statista, the bubble is bursting:

Therefore, we see more Chinese people:

- Saving. In both USD and RMB

- Looking for second residencies and passports overseas (for wealthier Chinese)

- And some will look at parking a percentage of money in the international and even local stock markets. The Chinese stock markets look cheap compared to Chinese real estate right now.

None of this means that the Chinese stock markets are low risk compared to their American and European counterparts.

However, the economy isn’t the stock market and vice versa.

Look at Japan. The Nikkei has soared, and performed better than most stock markets since 2008–2009, after an awful period before that.

What makes you the most mad about today’s economy?

There is one thing I have learned:

Complaining about somethings is like complaining about the weather.

It is pointless as you can’t affect it.

What is more, it allows people to make excuses and give themselves a pass for their own shortcomings.

So, many of the people who are mad at “today’s” economy, are just mad as they didn’t take the right actions.

For instance, many people complain about businesses going online and therefore “the rich getting richer”, because they didn’t adapt themselves.

The sensible people took action and adapted themselves.

That isn’t the same as passing comments or making valid points.

The wider point is that getting mad doesn’t make sense, when you could use the same energy to do something about it for your own life.

What aspect of modern life is most overrated?

Social media.

Let me qualify my statement.

Social media isn’t overrated when it comes to leveraging it for business or staying in contact with long-time friends who have moved away.

However, social media is over-rated as it has made the spotlight effect worse.

The spotlike effect, to quote Wikipedia, is “the psychological phenomenon by which people tend to believe they are being noticed more than they really are.

Being that one is constantly in the center of one’s own world, an accurate evaluation of how much one is noticed by others is uncommon”

It is human nature to believe we are being noticed more than we are because this was our experience as kids.

Yet many people in business and life don’t put themselves out there because they are afraid of getting noticed, or being laughed at.

How many people do you know who didn’t start a YouTube channel, or something else like that, despite it being useful in their business, because they were worried about negative comments and being noticed by friends and family?

It is common.

Yet people don’t really care.

This quote has been accredited to Churchill. Some people say he never said it. Regardless if it is true whoever said it:

Apart from some key people, few care about your posts.

So, it is better to just actually try to put yourself out there to get what you want.

The more traction and attention you get, the more your life will get better, if you are using social media to get a job, improving your network, having a bigger personal brand and growing your business.

Using social media for the below is very over-rated. You will just end up broke, with less financial freedom, for no good reason.

Picture credits: AZ quotes.