I often write answers on Quora, where I am the most viewed writer for investing, wealth and personal finance, with over 224 million views in the last few years.

In the answers below I will focus on countless topics including how to invest in US stocks from Brazil.

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or Whatsapp.

I live in Brazil. Is it possible for me to invest in the US stock market from here? How?

Source: Quora

It depends on the following factors:

- If you have any US-connections (are you a US taxpayer, citizen or tax resident?). Being a US-connected person doesn’t just mean being American in the traditional sense. Some Brazilians and other nationalities, who worked in American in the past, are US-connected.

- How much money you want to invest

- How complicated your situation is. If you plan to live overseas, and become an expat, your situation is much more complicated. High-net-worth individuals also tend to have more complex situations.

- If you want to do it yourself (DIY) invest or use an advisor.

In general, if your situation isn’t complex, it is fine to use “off the shelf” solutions such as Interactive Brokers.

It isn’t for everybody. The fact you can’t pay by card means bank transfer is a must, which makes it expensive for smaller accounts.

Likewise, the American domicile is a small risk when it comes to death taxes in particular.

It serves a purpose though if you have the self-control to DIY invest – which many people with their panic selling during market crashes don’t have but that is another story for another day.

In comparison, if you are very wealthy, an expat, likely to become an expat or have a complex situation, then you often need advice.

In either case, the fundamentals are pretty easy. You just need:

- To find a DIY broker or advisor who can accept you as a Brazilian resident

- Give your proof of ID

- Give your proof of address as well

- Complete any needed application forms

All of these documents helps financial institutions ascertain any risks, such as money laundering.

It is usually easy unless you are a politically exposed person (PEP) or have a special situation which doesn’t apply to most people – for example you own a business which could be related to money laundering like online gambling.

Once the account is approved you need to fund the account and trade.

You might also want to consider a local broker as well. Most people prefer international ones for obvious reasons, and it makes sense for expats and Brazilians who are planning to live overseas.

Yet I know from experience that getting money out of Brazil is either expensive or difficult to do.

I do know some international providers who get around this issue by offering rebates and processing the payments using a local merchant, but there are only a few firms like that.

What is the risk that entrepreneurs take?

Source: Quora

Consider this. Most people don’t consider medical school to be a risk:

Doctors can make good money after all.

Yet consider this

- Medical school can cost hundreds of thousands of USD or Pounds in some countries

- It takes ten years to train in some cases, if you factor in all training

- Many quit or at least do when they are young medical doctors

- The risk of being sued is higher than many other professions

Clearly society needs more doctors. The point I am making is that medical school isn’t framed as a risk.

Nor is becoming a teacher. In fact being a teacher is seen as a stable job in most countries even though an estimated 50% quit within just five years of getting qualified.

So, back to your question. It depends on how you frame it. Is it risky? Yes. You face the following risks:

- Being targeted by criminals in some industries (money laundering for example)

- Not making it

- Going into debt

- Not making as much as you did before.

- Being sued

- Even personal risks if you spend too much time on your business, and it affects relationships like family members.

But is it riskier than other professions? Not necessarily. In most countries in the world you can be let go with one or two months notice.

Those side benefits, like sick pay, indirectly come out of the salary of an employer pays. There are few risk-free options.

It also depends on the stage you are at in life. If you have loads of experience in an industry then sometimes starting your own thing is less risky than working for somebody else, especially if your relationship with your boss is frosty.

In comparison, if you are just starting out, then it can be much riskier to start your own business.

That is one of the biggest reasons why 9/10 businesses fail, alongside the fact that people seem to focus on great ideas and not execution and cash flow.

How do you leverage debt to increase your wealth?

Source: Quora

The two traditional ways of doing this are:

- Asset purchases. Usually real estate investments

- Business investments

For the first option, there has also been a growth in people using debt to buy assets like stocks too.

With real estate, the traditional method has been buy-to-let. You buy a home, put 10% or 20% down, find a tenant to cover the mortgage.

The leverage will help total returns:

The example below illustrates this:

Yet there is no such thing as a free lunch. Leverage has risks. If there was an easy and risk-free way to build your wealth exponentially with leverage why hasn’t Bill Gates and Buffett put 95% of their assets into this asset class rather than stocks?

The risks can be huge. The Lehman collapse showed that. Many firms and individuals struggled to find tenants.

Plenty also were forced to sell off stock to pay the bills, leading to a vicious cycle.

The same is true in businesses. Of course, in some industries, funding is important.

Yet it is much higher risk than building up a business organically through reinvesting cashflow.

We have seen that during the COVID-19 crisis. Several firms have gone out of business.

This has included some companies with long track records and great cash flow before the crisis.

What happened? Well most of these players didn’t take into account the possibility of “black swan risks”.

They were complacent. You see the same things after events such as 9/11 which affects certain industries – most people don’t take into accounts risks which have never happened before.

Many were over-leveraged and had high fixed costs. When lockdowns happened, they couldn’t trade as much apart from takeaways.

Leverage isn’t always bad, but it needs to be used carefully and the risk-reward ratios need to be good.

Taking a risk to make loads of money can make sense in some situations, but leveraging to earn 8% when several non-leveraged options can do better, doesn’t make sense.

We see the same things in financial markets. The asset class does well over-time.

That doesn’t mean leveraged ETFs make sense. They just work really well during certain time periods.

The commonality of all of this is that leverage can wipe you out during the very worst of times if you don’t gurard against it.

What emerging market would you invest in?

Source: Quora

I remember it well. I was relatively new to investing. All the hype was about the BRIC countries.

B – Brazil

R- Russia

India – India

China – China

Later South Africa was added to the list to make the BRICS:

You could see why as well. From 2000 until 2006 and 2007, emerging markets were battering developed markets – especially the tech-focused Nasdaq which was reeling from the 2000 crash.

The Chinese stock market, the Shanghai Composite, even went up by 400% from 2000 until 2006 – and that isn’t factoring in dividends:

What has happened since then?

Well:

- The Chinese stock market has been one of the worst long-term investments in the world since 2006.

- Most of the BRIC stock markets have underperformed. India’s has done relatively well, but none have done nearly as well as the Nasdaq.

- Yet all markets have had their day in the sun. Russia had the best performing stock market performance in 2019, before falling in 2020. China, Taiwan and South Korea (three countries seen in MSCI Emerging Markets) did well last year, with the South Korean market being the best performer.

- The good times for emerging markets has come when people least expected it. The bad times also came unexpectedly.

- There has been no correlation between higher GDP growth and stock market performance. That makes picking an individual country almost impossible.

- Some markets have performed very well during the most unexpected periods in the developed world too. A great example of that is how US stocks soared after the 2016 and 2020 elections. Few expected that.

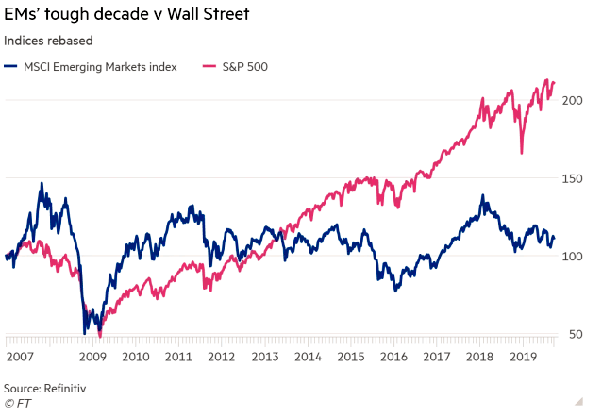

In recent times the S&P500 has beaten MSCI Emerging Markets by a huge margin:

That won’t happen forever. It didn’t happen last year in 2020. It didn’t happen from 2000 until 2008.

Emerging markets will have their time in the sun again. Long-term, however, emerging markets have beaten developed markets.

They have merely beaten them during some time periods. That means you should have a broadly-diversified emerging markets index, rather than picking individual countries.

Hold it long-term. I would keep allocations down to 10% though as it is riskier than developed markets.

Emerging markets do look very cheap compared to the S&P500 and Nasdaq on various ratios like price-to-earnings.

Remember though, markets aren’t always efficient, but they aren’t stupid either.

The reason those valuations are lower is that there is a bigger risk.

Further Reading

In the article below I discussed:

- Can reinvesting stock market dividends make you rich?

- What are the worst stock market investments you can make during the coronavirus period?

- What are the benefits of being cash poor but asset rich?

- How should a recent college graduate invest a small amount of money?

Below is a preview of one of the answer

Even in normal times, stock picking, which means you are trying to pick a specific stock rather than investing in the whole stock market, is very risky.

Or at least it is risky compared to buying the whole market. The history of the market is clear; long-term it will go up, especially with reinvested dividends, but individual names and sectors don’t always go up.

The stock market recovered from the 2020 crash. The airlines and many firms focused on the face-to-face economy haven’t yet recovered.

It took the market three years to recover from 2008. Most major markets hit numerous record highs.

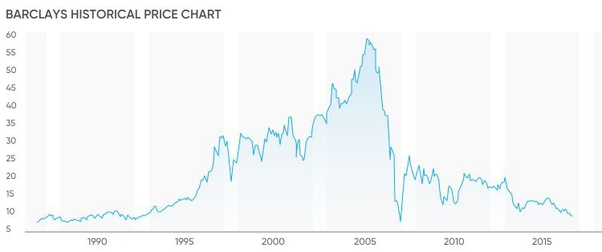

Yet the big banks have never came close to recovering in the UK, US and Mainland Europe.

Take Barclays as just one example of many I could have used:

During periods like the coronavirus and lockdowns, there is more uncertainty than ever before.

Of course a part of that uncertainty has now ended. It has become clear that with the vaccines we will probably be back to “near normal” sometime this year or in 2022, even if the vaccines need to be updated if the virus mutates into something else.

Uncertainty still lingers, however.

That means the following stocks are risky

- The airlines. We don’t know when we will fly regularly again and which airlines will be left. Those airlines which have state support are less risky of course, compared to those that don’t.

- Any hospitality group or any other firm which is reliant on the face-to-face economy, especially in countries which keep locking down

- Any firm which doesn’t have positive cashflow. These kinds of firms are always riskier. Many firms, like Tesla, do show it is possible to run at a loss for years, and eventually turn it around, but it is clearly a speculation to buy firms which aren’t yet profitable.

- Any fads. Fads and fashion change quickly. Similar to the third point, these kinds of stocks are always riskier.

- Stocks linked to commercial real estate. People are working from home these days. These trends were happening before the pandemic as well. Commercial real estate might recover in 2022 or 2023, but uncertainty looms over some parts of the sector.

To read more click below: