Considering short-term global investments can be an effective strategy for growing $200,000 over one year.

I often write answers on Quora, where I am the most viewed writer for investing, wealth and personal finance, with over 243.5 million views in the last few years.

On the answers below, taken from my online Quora answers, I focus on a range of topics including:

- What is the best way to invest $200000 for one year, or should you even reconsider investing for the short-term?

- Why shouldn’t you buy loads of luxury items if you become a millionaire?

- What are some reasons not to buy property during the coronavirus? I speak about numerous risks in the upcoming post-Covid world.

- Is investing 10% of your salary into the stock market a good idea? Assuming it is, is 10% enough for a comfortable retirement?

- Is mentality important for getting wealthy? If so, what kind of mentality is more likely to make you wealthy?

Some of the links and videos referred to might only be available on the original answers.

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

What is the best way to invest $200,000 for one year?

Source: Quora

I wouldn’t invest $200,000 for just one year. I would just put it in a high-paying cash account.

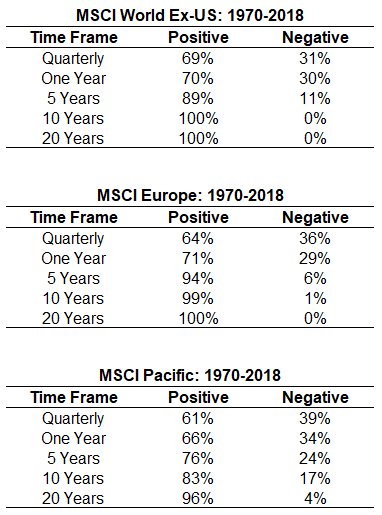

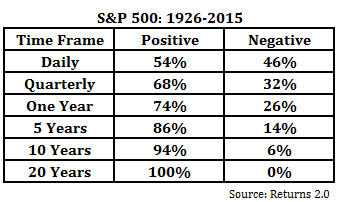

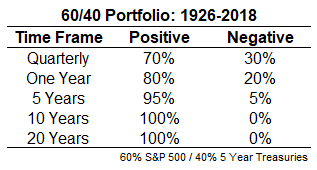

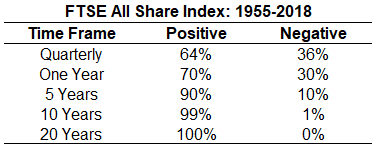

The reason is simple. Your chances of being down are exceptionally low over 20–30 years, but relatively high over a year.

That is the case for all the major markets – the S&P500, FTSE100, MSCI World and even a mixed stock and bond portfolio:

Now it is true that you do face a 70% chance of being up over a year, and probably 80%+ if you invest in a mixed stock and bond market portfolio.

Yet you are taking a risk, and even if that risk pays off, you won’t make hundreds of percentage points.

In comparison, if you invest for decades you have the benefit of lower risk and higher returns due to compounding.

If markets dip, or even crash, you can just buy more and stay the course. You can’t do that if you invest for just one year.

So time is one of the only free lunches in investing. So, invest the 200k for decades.

If you can’t do that because you are saving up for something in one years time, invest a small percentage of decades.

If ever I became a millionaire, why should I not buy unnecessary luxurious things?

Source: Quora

If you become a millionaire, you can spend money however you want.

Yet there are reasons why you shouldn’t go on a spending spree.

Firstly, it isn’t sustainable. $1m = $40,000 of safe withdrawals per year.

Yes there are higher-risk ways of drawing down a portfolio, but 4% has been tried and tested.

$2m = $80,000 a year. That means if you spend considerably more than that, you will be back to square one eventually.

One of the biggest reasons to become wealthy is to have choices and more freedom.

That means the choice to tell your boss where to go if he/she is being obnoxious.

It could mean selling out your business, and retiring, if you have had enough as a business owner.

You lose that choice as soon as you start spending more than is coming in.

That is one of the biggest reasons most inherited wealthy people, and lottery winners, go broke.

The money eventually runs out. What is going out is greater than what is coming in.

Beyond that, also remember that

- Studies show that the experiences we have, even if they are free and cheap, matter more than consumption. I guess we all remember the first time we traveled overseas or even did something like climb a mountain. New experiences last. A new iPhone just gives you a sugar rush for a few days:

- Above a certain level of material comfort, it doesn’t matter as much. No 30 or 40 year old wants to travel to a rat-infested hostel or “hotel from hell”. Yet the difference between a 4 star and 5 star hotel isn’t always huge.

- The straight of our relationships matters more than consumption too.

- People always want what they don’t have. People who don’t have much money usually want more money even if they criticise “the rich”. Once people get more money, they care more about time, experiences etc.

- In this day and age, technology is a game changer. Most people would prefer an iPad , Netflix subscription or phone to a home cinema system if the home didn’t have WIFI or 5G. I also know plenty of people who would prefer to use a cheap tool like Zoom and never travel for business as an owner, compared to flying in business class and five star hotels regularly.

- Sometimes more consumption will results in more problems. A bigger house, as an example, could result in more maintenance issues.

I think that is one of the biggest reason many wealthy people are quite frugal.

Basically if you try out overspending for a few months you realise it isn’t all that it is made out to be.

Don’t get me wrong, everybody needs some material comfort. I don’t believe in extreme frugality.

The odd, occasional, “waste of money” for something you like isn’t a big deal at all.

But I don’t think overconsumption makes people happy compared to the security wealth brings, experiences, more time, exercise etc.

It is your money though. Do whatever feels right provided you don’t negatively influence other people.

What are some reasons that someone shouldn’t buy a house right now?

Source: Quora

When Covid-19 started about a year ago, at least in terms of the first lockdowns, few expected work from home to continue indefinitely.

Fast forward twelve months and there is uncertainly about the following things:

- How long Covid will last for. It seems we are near the end now, at least in developed countries, but with new variants who knows?

- Assuming we are near the end by the second half of this year in most developed countries, people would have became used to a normal way of working for over a year, maybe 18 months or longer. By that stage, Covid might have improved but is still likely to be “endemic”, meaning it could flare up in winters, albeit less than in recent times. Therefore, will people really want to commute to work every day of the week? Will it be replaced by a full-time work from home culture, or a hybrid model?

If we are moving towards a remote world, which seems likely and was happening even before the pandemic, that implies that big cities could struggle.

Why pay 4k a month for rent and up to 50% tax, if you can move to a nearby place, or indeed emigrate?

We have already seen a huge conversation about the number of remote workers leaving California for Texas, and London house prices struggling relative to the rest of the UK.

The point is, there is more uncertainty now than ever. I guess the positive is that smaller towns and cities have struggled for so long, and are likely to benefit from this trend, that prices in those regions could rise.

In addition to that, in some countries there are Covid-related stimulus packages.

This often means that the huge taxes which are associated with real estate purchases have been reduced, or eliminated, for a limited time.

Is it a good idea to invest a 10% salary in the stock market every month?

Source: Quora

This is something most people already do, at least indirectly.

In many countries people pay into a pension, sometimes through auto-enrollment.

Most of this money is linked to the stock market. Even if you don’t pay into a pension, the need to invest at least 10% of your income exists.

To achieve a 75% replacement rate at retirement, meaning you will earn 75% of what you did in work, 10% is a minimum unless you started at a very young age:

So yes, it is a good idea, provided you:

- Are long-term orientated. Stock markets are a great way to build your wealth over time, but can go up, down or sidewards in the meantime or even sometimes medium-term.

- Know what you are doing it hire somebody who does. Many people buy specific stocks for the wrong reasons,

- Avoids putting most of your basket in individual stocks as a non-professional investor

- Have your eggs in different baskets such as bonds and REITS, especially as you approach retirement age. 100% in stock ETFs is fine if you are younger.

- Don’t panic whenever there is a stock market crash or correction.

- Avoid the next big thing and investment fads that come and go. A lot of people lose money in stocks, even though the general market has always gone up, often for this reason and panic selling.

- Keep emotions out of the process as much as possible.

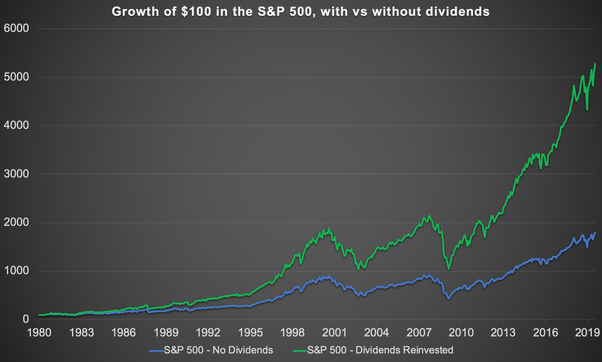

- Reinvest your dividends. As per the graph below, it is an essential component of investing. More than half the S&P500’s returns have been from dividends over the last decades:

Basically, have a plan on day one, and stick to it. If you know on day one that you will invest at least 10% of your income for decades, and you keep to that no matter what, you should do well.

People often make the mistake of changing their strategy due to events outside their control like a crash, even though markets have always came back.

I would also set up a direct debit one day after you are paid. This will allow you to invest more than 10% without really thinking about it.

If you leave it until the end of the month, you might already spend the money.

Do you think that for being rich and making money, it is necessary to maintain a certain state of mind?

Source: Quora

For sure. The reason is simple. The number of people who have had loads of money at one stage in their life, far exceeds those who still have money when they are old.

The main reasons for this are (in no particular order)

- Divorce and the legal costs associated with that.

- Overspending and debt. This can affect even the highest earners.

- Complacency when the going is good. We have seen that during Covid times. Some people, and businesses, never prepared for a downturn and unexpected events, in much the same way few made contingency planning in the hospitality industry before 9/11

- Putting all eggs in one basket. This is linked to complacency and has affected people recently in numerous Latin American countries, Egypt, Tunisia and other places which have experienced political turmoil

When you speak about mindset I have noticed the following commonalities and generalisations.

- Most people think “live for today”. Wealthier people are more likely to think “live for today with an eye for tomorrow” or fully focus on delayed gratification. Think about your own network. Imagine all of them received 200k tomorrow from inheritance. How many would just spend it? Probably at least 50% would within ten years. Wealthier people are more likely to think “what can my money earn me” and not “what can my money buy me”. 200k can be grown, and long-term, you can make more from it rather than just spending it at once.

- Emotions. Loss aversion is when people are obsessed with losses. In other words, loses are more painful than gains are pleasurable. Therefore, most people are too cautious. Better safe than sorry. A few people are too far in the other extreme and take silly risks. Wealthier people are more likely to take calculated risks. In other words, avoid the two extreme of being overly cautious or too adventurous.

- Making money isn’t more important than managing money for most wealthy people, after a certain level of consumption has been achieved. That is the opposite to how most people think. “How would you spend a lottery win” is something many people are asked. Few ask “how would you invest a lottery win to ensure you could grow the money and actually consume, long-term, more than spending it in one go”.

- The world vs local. It is a big world out there. There are far more people globally than in your local community if you are a business owner.

Further Reading

In the answers below I focused on:

- Why does Harry Browne’s permanent portfolio have such a large allocation to gold? Has this portfolio performed well relative to the S&P500 and Ray Dalio’s All Weather Portfolio?

- Why do people believe that property is a great investment and are they right?

- To open a business, do you need loads of money? I offer a different narrative.

- Does having more money mean you are more successful?

- Should you invest in the ARK ETFs?

To read more click below: