Non-UK residents can purchase UK annuities in certain cases, but options are limited.

Tax rules are more complex, and currency risk is a significant factor compared with residents retiring in the UK.

This article covers:

- What do you mean by annuity in the UK?

- How do you buy an annuity in the UK as a non-UK resident?

- How much to buy an annuity in the UK?

- What are the advantages and disadvantages of annuities in the UK?

Key Takeaways:

- UK annuities are possible for non-residents, but provider access is the biggest practical barrier.

- Tax is a two-country coordination exercise, and treaty claims are often required to avoid double taxation.

- A sterling annuity creates real income volatility if your spending currency is different.

- The strongest expat strategy is usually partial annuitisation, not 100% annuitisation.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions. We also offer bespoke structuring solutions tailored to your situation.

The information in this article is for general guidance only, does not constitute financial, legal, or tax advice, and may have changed since the time of writing.

What is a UK annuity?

A UK annuity is a contract where you give an insurance company a lump sum, and they promise to pay you a regular income, usually for the rest of your life.

For most expats, this lump sum comes from a UK pension pot, and the income is normally paid in pounds sterling into a bank account.

In UK retirement planning, annuities are one of the main ways to convert pension savings into guaranteed lifetime income.

They are commonly purchased using defined contribution pension pots once retirement begins.

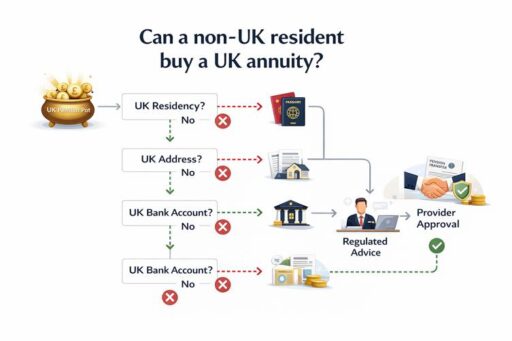

Can a non-UK resident buy a UK annuity?

A non-UK resident can sometimes buy a UK annuity, but many providers restrict sales to UK residents or require a strong UK connection such as a UK pension or bank account.

In principle, UK pension savings can still be used to buy an annuity even if you live abroad.

However, eligibility is largely determined by the policies of individual annuity providers rather than UK pension rules.

Providers assess factors such as regulatory obligations, documentation requirements, and where payments will be made.

In practice, many insurers require applicants to be UK residents at the time of purchase.

Some will allow the annuity to continue if you move abroad after buying it, while a limited number may accept non-resident applicants with clear UK ties.

What are the types of annuities in the UK for non-UK residents?

Available annuity options include lifetime annuities, fixed-term annuities, level annuities, increasing annuities, single-life annuities, and joint-life annuities.

The main annuity structures used in UK retirement planning are still relevant for expats.

Especially if the annuity was purchased before moving abroad or if a provider accepts overseas applicants.

- Lifetime annuity:

A lifetime annuity pays you an income for as long as you live, in exchange for a one-off lump sum from your pension.

If you live longer than expected, you win because the insurer keeps paying; if you die early, the insurer keeps what is left.

- Fixed-term annuity:

A fixed-term annuity pays you a guaranteed income for a set number of years (for example, 5 or 10), sometimes with a maturity value at the end.

It can suit expats who want certainty for a few years but don’t want to lock in for life, for example, while waiting to see where they will settle.

- Level vs increasing (escalating) annuities:

A level annuity pays the same amount every year, while an increasing annuity rises by a fixed percentage or with inflation.

For non-residents, an increasing annuity may help offset both UK inflation and long-term currency erosion if you spend in another currency.

- Single-life vs joint-life annuities:

Single‑life covers just you; payments stop when you die.

Joint‑life continues some or all of the income to a spouse or partner after your death, which can help if your partner depends on that income and may also be a non-UK resident.

How to buy an annuity as a non-resident?

To buy an annuity as UK non-resident, you confirm eligibility with your pension provider, obtain quotes through a UK financial advisor or annuity broker.

You then review the tax treatment in both countries and complete the annuity purchase using your UK pension pot.

If a provider accepts non-UK residents, the process is broadly the same as for UK residents.

This means you usually need:

• An eligible UK pension pot

• Identity documents

• Proof of address

• UK-regulated financial advice before the pension can be turned into an annuity

Defined benefit (final salary) pensions over a certain transfer value require regulated advice before you can move them into a pot that can buy an annuity.

If a provider accepts non-UK residents, the process is broadly the same as for UK residents.

Typical steps:

1. Check if your current pension scheme and potential annuity providers allow non-resident annuitants and what conditions apply (for example, UK bank account, UK address, documentation).

2. Get quotes via a UK financial advisor or an expat specialist who can shop around and confirm which providers will deal with your country of residence.

3. Ensure you understand the tax position in both the UK (source state) and your country of residence, including any double tax treaty relief mechanism.

4. Decide on currency (keep in pounds or convert) and payment logistics (bank charges, FX spreads, timing of transfers), and then sign the annuity contract through the chosen provider.

How much do annuities cost in the UK?

The cost of a UK annuity is the pension lump sum you hand over and the rate the insurer offers, expressed as income per year for every 100,000 pounds you invest.

As a rough rule, the more guarantees and extras you add (inflation increases, spouse’s benefits, guarantees on death), the lower the annual income you’ll get for the same lump sum.

Key points that drive cost for non-residents:

- Age and health: Older or less healthy people often get higher annuity rates because insurers expect to pay for fewer years.

- Type of annuity: Level, single‑life annuities pay more than inflation-linked or joint‑life ones.

- Interest rates: When long-term interest rates are higher, annuity rates tend to be better.

- Provider policy on non-residents: Some insurers won’t offer new annuities if you live abroad, which limits competition and can mean weaker pricing for those who will.

What are the key factors to consider before buying annuities?

The key factors for purchasing an annuity include where you plan to live long term, how stable your other retirement income is, and how your tax situation works across countries.

Before committing to a UK annuity as a non-resident, you should weigh your personal situation more than the headline annuity rate.

These few key questions can guide your decision.

- Where will you live and spend the long term?

If you’re likely to move again or possibly return to the UK, an annuity may fit differently than if you are permanently settled elsewhere.

A fixed sterling income works best when your long-term life is stable or still linked to the UK.

- How secure is your other income?

If you already have inflation-linked pensions (such as state pensions or defined benefit schemes), you may need less annuity and more flexible investments.

If your other income is volatile or market-based, an annuity can be the stabiliser.

- What is your tax profile across countries?

You need to consider UK taxation, any double tax treaty, local tax rules, and whether future residency changes could alter the picture.

Cross-border tax advice is almost essential once income spans multiple systems.

What is the taxation of annuities for non-UK residents?

For non-UK residents, UK pension annuity income is treated as UK‑source pension income and is generally subject to UK income tax under PAYE.

The UK normally taxes at source, but a double tax treaty may give primary taxing rights to the country of residence, in which case UK PAYE can be reduced or stopped after HMRC approval.

Key points:

- UK pension annuities are treated like other pension income and taxed under PAYE in the UK unless a treaty restricts this.

- Non-residents can claim the UK personal allowance if they are UK nationals, EEA nationals, or eligible under a relevant double tax treaty.

- Some countries classify annuity income differently (for example, partly as capital return), which can lower or change local tax.

- Changes to the UK non-dom regime from April 2025 mainly affect UK-resident individuals, but can matter if an expat later returns to the UK.

Because of the moving parts, most expats should coordinate with both a UK-savvy adviser and a local tax specialist before and after buying an annuity.

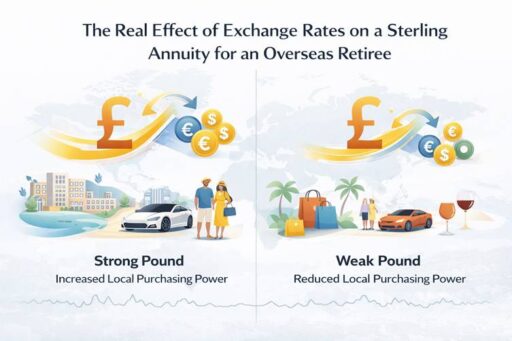

What are currency and payment considerations?

Most UK annuities pay in pounds to a UK bank account, which means non-residents face foreign exchange risk and payment logistics when they spend in another currency.

Exchange‑rate swings can significantly change your real purchasing power in your country of residence, even though your nominal pension income is guaranteed in sterling.

Practical considerations:

- Currency mismatch: If you spend in euros, dollars, or another currency, a sterling annuity can feel like a variable income when exchange rates move.

- Limited foreign‑currency annuities: A few providers may offer payment in major foreign currencies or allow you to choose an overseas bank, but charges and rates vary.

- FX costs and timing: Using specialist FX services or multi-currency accounts can reduce conversion costs and allow you to transfer when rates are favourable.

- Diversification: Some expats reduce currency risk by balancing a UK annuity with local‑currency investments and pensions in their country of residence.

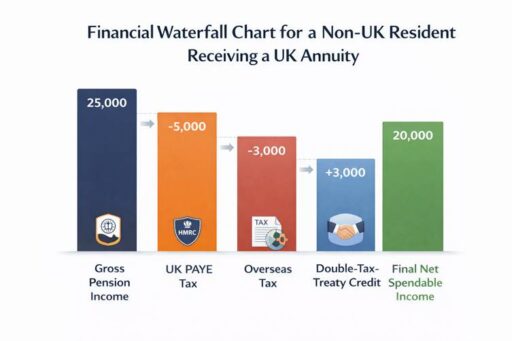

Illustrative Scenario: How Taxes and Currency Affect a UK Annuity

Consider a retiree who lives permanently in an EU country but holds a UK pension pot of £200,000.

The retiree uses the full pot to buy a level lifetime annuity that pays about £11,000 per year in pounds.

Tax impact

Because the annuity is UK-source pension income, it may initially be taxed in the UK through PAYE.

However, a double tax treaty may give the country of residence the main taxing rights.

In that case, the retiree may need to claim treaty relief so the income is not taxed twice.

Currency impact

The annuity is paid in pounds, but the retiree spends money in euros.

If the pound strengthens, the converted income increases.

If the pound weakens, the retiree’s real spending power falls even though the annuity payment itself stays the same.

Simple outcome

The retiree receives a stable income in pounds but faces two ongoing variables: cross-border tax treatment and exchange-rate changes.

These factors determine the real value of the annuity in the country where the retiree lives.

What are the pros and cons of annuities in the UK for non-residents?

For non-residents, UK annuities offer strong security and simplicity but come with reduced flexibility, tricky tax interactions, and currency risk.

They can be a good foundation for a stable income, but they rarely work well as your only retirement solution when you live and spend abroad.

Think of a UK annuity like buying a very sturdy, heavy safe.

Once your money is in, you are protected, but you can’t easily change what’s inside.

As an expat, your life is more mobile: you may switch countries, currencies, and tax systems. That heavy safe keeps your money secure, but it may not move smoothly with you.

Main pros for non-residents:

- Income security: Guaranteed lifetime income in pounds, removing investment and longevity risk.

- Regulatory protection: The UK annuity market is regulated with strong consumer protection and oversight.

- Portfolio balance: Annuities can complement drawdown accounts, tax-efficient investments, and foreign pensions in a diversified retirement income strategy.

Key downsides:

- Limited access: Many providers simply won’t sell to non-residents or have strict limits.

- Tax complexity: You may face UK PAYE withholding plus local tax, with double tax treaty relief needed to avoid being taxed twice.

- Currency mismatch: Your income is in pounds while your spending is in another currency, so exchange rates can boost or cut your real spending power.

What are annuity alternatives for non-UK residents?

The main alternatives to annuities include pension drawdown, overseas pension transfers such as QROPS, and blended strategies that combine guaranteed income with flexible investments.

Non-residents with UK pensions are not forced to buy an annuity; in fact, many choose flexible options or overseas structures instead.

Alternatives can offer more control, better tax outcomes, or reduced currency risk, but place more responsibility on you for managing investments and withdrawals.

Here’s a detailed explanation of the common alternatives for expats:

- Pension drawdown (flexi‑access drawdown)

You leave your money invested in a UK pension and draw an income as needed, rather than buying an annuity.

This lets you adjust income, vary withdrawals with markets, and keep your pot accessible for heirs, but investment risk stays with you.

- QROPS and overseas pension schemes

Transferring your UK pension to a recognised overseas scheme can give more local‑currency options, local tax treatment, and flexible access.

However, transfers carry regulatory, fee, and tax risks, and UK regulators have highlighted concerns about poor overseas transfer advice.

An overseas transfer charge of 25% may apply in some cases.

- Blended strategy (part annuity, part investments)

Many expats combine a smaller annuity to cover essentials with drawdown or other investments for discretionary spending and legacy goals.

This can balance certainty and flexibility, especially when currency and tax issues make a full annuity solution too rigid.

Conclusion

For non-UK residents, UK annuities can still play a useful role, but they are rarely as straightforward as they appear.

Access limitations, tax coordination between countries, and currency risk mean you should treat a UK annuity as part of a wider expat retirement plan.

A sensible approach is often to decide what minimum safe income you want guaranteed and see whether a partial UK annuity can help cover that.

This should be done while keeping some pension money in more flexible vehicles like drawdown, overseas pensions, or local investments.

Before signing anything, it’s wise to get advice from both a UK-regulated pensions specialist and a financial or tax advisor.

By doing so, your annuity works with your residency plans and long-term goals.

FAQs

How are annuity rates calculated for expats?

Annuity rates for expats are mainly based on the same factors as for UK residents: age, health, annuity type (single or joint, level or increasing), and prevailing interest rates.

However, provider policies on non-residents can restrict which products you can actually access.

So, in practice, the rate you get may depend heavily on which insurers are willing to deal with your country of residence.

What affects annuity rates in the UK?

Key drivers include long‑term interest rates (higher rates usually mean better annuity income), life expectancy assumptions, and product features such as inflation increases, spouse’s benefits, or guaranteed payment periods.

Market competition and regulatory capital requirements also influence pricing, and for non-residents, additional admin and compliance risk can make some providers less keen to offer aggressive rates.

Is an annuity 100% safe?

No financial product is 100% risk‑free, but UK annuities from authorised insurers are heavily regulated and benefit from consumer protection frameworks, including compensation schemes if a provider fails.

You still face risks such as inflation eroding a level income, currency swings if you live abroad, and tax or rule changes over time.

Therefore, the safety is mainly about the promise of payments in pounds, not about protecting your real overseas spending power.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.