The more we understand the world to be a global village, the more it depends on acquiring the right platform to receive international payments to the right hands.

In Payoneer vs Remitly article, we’ll show their respective fees, processing time, accessibility, and customer service support.

With our best diligence efforts, we’re looking at providing an evident image of what each platform has to offer for businesses and individual users.

If you are looking to invest as an expat or high-net-worth individual, which is what I specialize in, you can email me (advice@adamfayed.com) or WhatsApp (+44-7393-450-837).

This includes if you are looking for a second opinion or alternatives.

Some facts might change from the time of writing, and nothing written here is financial, legal, tax, or any other kind of individual advice, or a solicitation to invest.

What is Payoneer?

Payoneer was established in 2005 by Yuval Tal in New York to meet cross-border payment requirements of freelancers, small businesses, and online marketplaces.

What does Payoneer do?

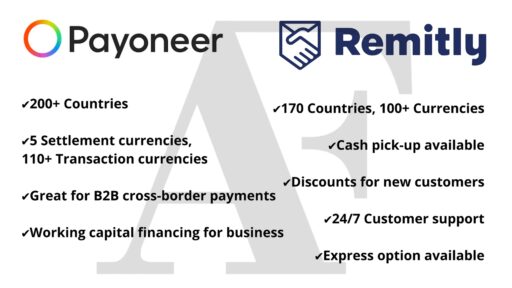

- Acceptance of payments from 200+ countries worldwide

- Mass payout facilities for businesses and marketplaces

- Multicurrency accounts with local receiving facilities

- Prepaid Mastercard for earnings expenditures

- Working capital and financing products

- VAT payment solutions for international businesses

- Wide marketplace integration such as Amazon, Airbnb, and Upwork

What is Remitly?

Remitly, started by Matt Oppenheimer, Josh Hug, and Shivaas Gulati in 2011, is an expert in simplifying global remittances.

Especially for immigrant communities remitting money back to their sending country.

What does Remitly do?

- International money transfers

- Cash pickup services

- Mobile wallet transfers

- Express and Economy transfer services

Which charges less, Payoneer or Remitly?

What does Payoneer charge?

There are no fees to open and hold an account, but Payoneer charges 29.95 USD annual account fee for all customers if your account is inactive after 12 months (less then 2,000 USD received).

Payment received using Payoneer’s Global Payment Service is free when payers send supported currencies via local bank transfers.

Payoneer-to-Payoneer transfers are free, but crediting a Payoneer account using credit or debit cards comes with a charge (1%~up to 3.99%).

Withdrawal fees differ by location: domestic bank withdrawals in the same currency are usually $1.50 (up to a threshold of 50,000 USD/GBP/EUR), while international withdrawals can cost up to 3%.

For cash spending from the account balance, the Payoneer Mastercard imposes a $3.15 ATM withdrawal fee, together with any fee charged by the ATM operator.

Cross-border purchases in a foreign currency different from the card’s base currency incur a 3.5% transaction charge.

Business accounts with more than $1 million in volume possess specialized FX hedging capabilities and batch payment APIs, along with a discounted conversion fee of 0.3%.

Payoneer is investing in real-time payment infrastructure in 15 emerging markets in 2025, a step which can lower correspondent banking expenses.

Refer to Payoneer’s fee overview for precise estimates.

What are Remitly fees?

Remitly has two transfer speeds: Express and Economy, both with varying fees and exchange rate margins that can affect the overall cost. The following is the detailed breakdown:

Express Transfer:

For immediate transfers but with additional fees.

As an example, transferring less than $500 from the United States to the Philippines via debit card costs around $3.99. A transfer of $1,000 to India is also charged the same amount.

Economy Transfer:

Prioritizes cost savings with longer delivery and either no or low fees for most destinations.

Transfers from the Philippines to the U.S. or other countries from a bank account are free up to $500, and for larger transfers of $1,000 to India, they can be free depending on the payment method.

Influence of Payment Method:

Transfers from a bank account tend to be less costly than paid by credit or debit card.

Credit card transactions can also have additional cash advance fees by the card issuer, in addition to the overall cost.

Impact of Destination and Transfer Size:

Economically popular corridors have lower and more standardized fees, whereas unpopular corridors might be higher.

Higher transfers can receive lower or no fees, particularly when transferring via Economy mode.

To get a precise estimate of the transaction, you can utilize the Remitly Calculator.

Additional Fees: Exchange Rate Margins

Along with transfer fees, Remitly also pays an exchange rate margin.

The margin depends on transfer speed and destination and isn’t always fully disclosed. It can short the recipient of the mid-market exchange rate on high-value transfers.

Promotional Offers and Guarantees:

First Transfer Promotion: New customers are provided with a free first transfer, which might be on terms like “new customers only, one per customer, limited-time offer.”

Fee Refund Promise: Remitly assures timely delivery, refunding the transfer fee in case the transaction is not completed on time, giving an additional assurance.

Even though exchange rate margins determine the ultimate cost, Remitly assures transparency by showing a distinct fee breakdown and margin rate markups that come into play prior to completing the transfer.

Which is better, Payoneer or Remitly?

Payoneer seeks to enable the global freelance economy and cross-border e-commerce.

With its Global Payment Service, users are provided with local bank accounts in various currencies (USD, EUR, GBP, JPY, AUD, CAD, etc.), which allow them to receive payments as a local business.

This avoids fees for those receiving regular international payments.

The Payoneer Mastercard also provides instant access to funds without the need for a bank transfer, although foreign transactions come with extra charges.

Remitly carries out two transfer levels:

Express Transfers remit money from minutes to several hours but charge a fee.

Economy Transfers take 3–5 business days and involve low fees.

Aside from bank transfers, Remitly also supports cash pickup and mobile wallet deposit.

Its mobile-first technology is user-friendly and has 24/7 customer service for emergencies.

Conclusion

Our review suggests that both Payoneer and Remitly bring something special to the table.

Payoneer’s strong platform is best suited for business-to-business transactions and freelancers.

Especially those who need a multi-currency setup, while Remitly does quick, seamless remittances with a customer-centric focus.

It ultimately depends on your unique use case and local situation.

Regular due diligence will guarantee that the chosen service will still fit your changing financial needs.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.