I watched an interesting video a few days ago.

As you can see from the participants, most are in their 50s and 60s.

There is no indication that most of the people contributing had lived overseas before, and most of the advice wasn’t linked to business or investing directly.

It got me thinking. Having lived overseas for over a decade, and in eight countries including my birth nation of the UK, what advice would I have given to my younger self?

Here is a list of 25:

1. Take as many risks as possible

You do have to take older people’s advice with a pinch of salt (more on that later), but when a commonalty comes up again and again, you should take notice.

The older people on the video above said that “we should have gone for it more” and “taken more risks”.

It is a pity that most well-meaning parents and general society encourage their kids to remember that “it is is better safe than sorry”.

In reality, few people regret what they do, only what they don’t do, and we won’t live forever.

Taking that trip, investing a small portion of your assets into a high-risk investment or venture and emigrating are just three examples of things we are unlikely to regret when we are ninety.

We are more likely to regret not trying.

Needless to say, being reckless doesn’t make sense either, but it is easy to be too cautious.

2. Experiment

In business, firms have to be ahead of the curve. You can only do that by experimenting and relying on previous experience.

Relying on customer research alone also doesn’t make sense.

In one of my latest Forbes articles, I mentioned how relying on customer research isn’t the best way to gauge public preferences, because few people will admit that they prefer not speaking to people in-person (as an example).

The same is true in your personal life. If you want to life overseas, it is more likely you will find a suitable place if you experiment and live in many locations.

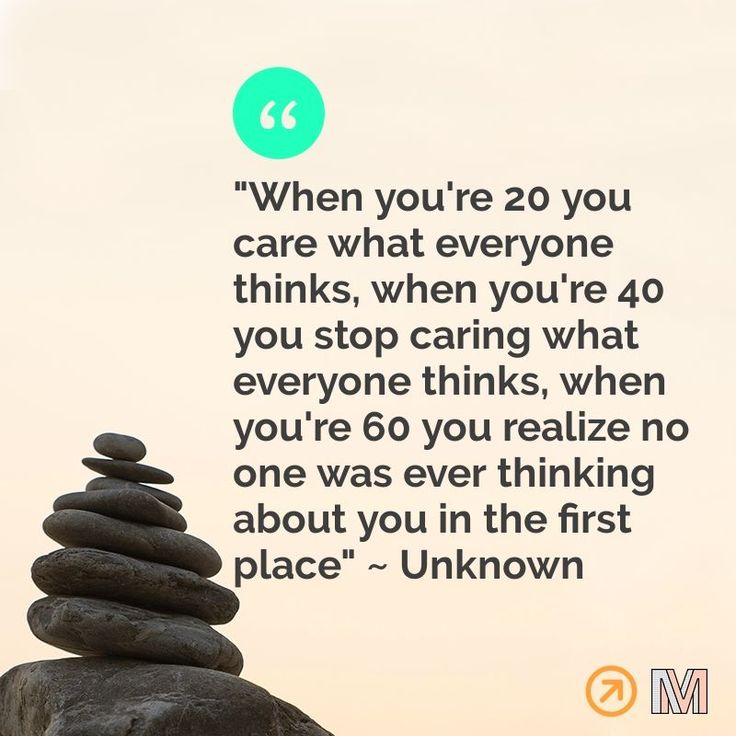

3.Don’t care about what others think.

More than likely nobody is thinking about you to begin with

4. Break industry norms.

Norms stand for normal. Normal actions will result in normal results. As a newbie in an industry, you won’t be encouraged to break norms.

Over time, you will see what things could be improved and changed.

When I started an online, and remote, business in 2018, people laughed. Now I get called a visionary and more pleasant things, and invited by the media to give my opinions on digitalisation trends.

The big returns in business are in doing things which make both yourself, and your competitors and industry, a bit uncomfortable.

Nothing good comes from the comfort zone – whether that is your comfort zone or your industries.

Ignore the naysayers.

5. Everybody can do well in investing and business

You don’t have to be a genius to do well in business or investing.

6. Get a job first and then start a business.

This follows up from the last point.

You don’t need to be a genius to start a business. You just need to know how to execute.

You are more likely to know how to execute if you have experience in a particular domain.

7. Focus on time and ROI

Return on investment (ROI) is important, but time is the only non-replaceable resource.

Beating the stock market by 1% per year isn’t worth it if you are spending hours a week achieving that.

Likewise, as a business-owner, it can make sense to make less money short-term, by outsourcing some tasks.

8. Production beats perfection

Some best-selling books are full of typos. Some products and services that have sold millions have had the same issue.

Few people care. That doesn’t mean typos are good per see, but spending tens of hours solving them, is less efficient than getting out content today.

The same is true in many domains. If you wait for perfection, you will always wait. There is no perfect time to invest, start a business or do many things.

The best time is usually yesterday and the second best time today.

9. Be persistent

No matter how hard and smart you work, you will have to be persistent.

The longer you try, the more likely you are to succeed, due to the numbers game.

In much the same way that cold calling traditionally worked because one person would say yes out of a hundred, the same is true for business ideas.

Most successful business people have failed many times. Even once you have a successful business and want to expand into other services, you might need to try twenty ideas for one new idea to work.

10. Not all debts are bad

Debt can be dangerous, but a lot of financial fortunes are built on leverage.

11. Ideas don’t count. Only execution does.

Everybody has multi-million dollar ideas.

12. Be mindful of confirmation bias.

There will always be evidence pointing in different directions. The key thing is what is the net effect of your actions.

Let’s give a simple example. When I started an online model in 2018, I had numerous people in that pre-Covid world who didn’t want to deal with me, because they preferred meeting face-to-face.

Yet business in 2018 and 2019 skyrocketed. Therefore, the right decision had been made to change my business model, because the net effect of my actions was positive.

It is all too easy to let a few rejections or failings stop you from seeing the bigger picture.

13. Get rid of shallow people.

The quote below is attributed to Churchill, even if it is disputed.

Whoever said it is irrelevant.

The point is that we often spend too much time with shallow people who we assume are our friends.

Fortunately, if you move cities or countries, it is easier to see who your real friends are before the age of 60.

14. Focus

If you do a joint major at university, such as politics and German, you probably think you will spend 50% on both majors.

What will happen is each side wants 70% of your time, and therefore you work 40% harder than those with a conventional major.

The same is true in investing or business. If you have ten side hustles, they will each take up 20%-25%, rather than 10%, of your time.

You will become a generalist and not a specialist.

It will be different to do well in any of those ten businesses, as you will be competing with specialists.

Better to focus on one thing, even if it seems riskier, at least early on in your career.

Working hard is important. But working hard and smart in a focused way is much more effective.

15. Don’t just listen to older people in your industry

It is normal, and sometimes sensible, for new graduates to seek the advice from more experienced people when they graduate.

In some domains this makes sense. If you are an engineer in oil & gas, or a teacher, then this is probably sensible.

In some industries, such as sport and business, things are always changing, to a much larger degree than in other industries.

Therefore, it is important to be selective about who you listen to, as some people become dinosaurs quickly, if they fail to adapt.

It is best to seek advice from people who are accomplishing what you want to achieve, and have done so relatively recently.

For instance, taking advice from somebody who has cracked social media in the last five years, is more likely to be relevant than somebody who started in 2008, and has mainly been living off that first mover advantage ever since.

If you want to get fit, listen to fit people. If you want to get wealthy, listen to self-made wealthy people.

Don’t just listen to somebody because of age.

16. Delay gratification

There is nothing wrong with being impatient, but accepting less money can sometimes make sense.

When you are 20 or 25, it is better to focus on where you will be at 30, rather than at 26.

What is more, you can afford to take more risks, assuming you don’t have kids and responsibility.

Some of the highest-paid 30-year-olds I knew took big risks in their 20s, and often made little money at that time.

Examples of this include getting paid on performance and not time. As a pure example, it is difficult at first to be a commission-only real estate salesperson, but if it works, you will eventually make much more money than your peers, and be able to make your own schedule.

What is more, if you fail at a young age, it probably won’t matter.

Don’t compare yourself to others. What your university classmates are doing, and earning, at 25, won’t matter at 35 or 45.

17. Seek forgiveness and not permission.

With one or two big exceptions, seeking forgiveness and not permission, usually works.

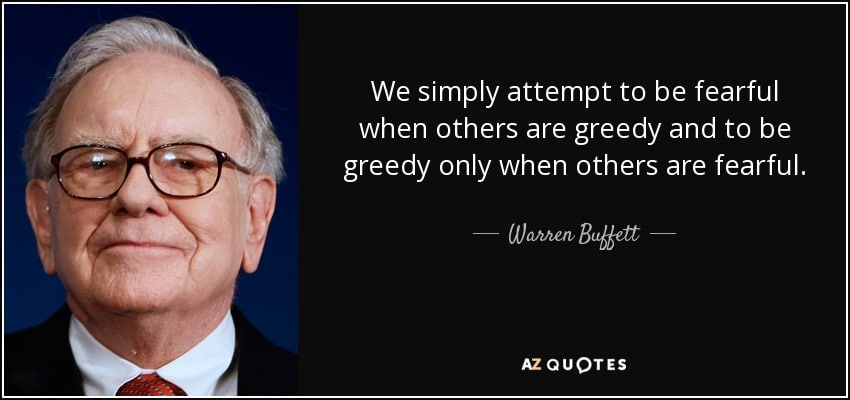

18.Be greedy when others are fearful

Many people have heard of this famous Buffett quote:

The part about being greedy part when others are fearful, is the aspect that most people struggle with.

As per the first point, taking risks in general is important. However, the more risks you can take when you are young and when others are fearful, the more likely they are to pay off.

Let’s give a simple example. Imagine the stock market crashes by 50% in the next few months, like it did in 2000, 2008 and 2020.

If you are 30-years-old, with no kids and major responsibilities, your downside is protected by leveraging yourself/using debt like a Lombard loan in a responsible way.

In comparison, if you have semi-retired and are 65-years-old, the incentives are different.

19. Don’t listen to the media too much.

Remember the media exists to make us fearful – whatever bleeds leads. We are the product and they need to keep us hooked, which is why they make up sensationalist headlines.

Many people failed to invest during various stock market crashes due to the mantra that “this time is different”.

20. Invest in yourself.

Personal investments are good, but it is important to remember that learning doesn’t stop when you leave university. Often it has just started.

21. Be grateful

Being ambitious is great. In fact, we probably don’t have enough of it in most developed countries, now we all live such easy lives compared to hundreds of years ago.

However, being grateful for what you have, is always important, provided it doesn’t stop you being ambitious.

22. Accept people for who they are.

Don’t try to change people. Accepting people for who they are doesn’t mean agreeing with them, or liking them.

It just means that it is pointless to try to change them. Just be selective about who you deal with.

23. Ask the right questions.

Questions such as “what would you do if you knew you couldn’t fail”, and “if you only had 1 hour to work per day, what activities would you focus on”, can clarify your thinking.

24. Focus on the world.

The world is your oyster as the saying goes, yet it is only relatively recently that people focused on selling their services internationally.

Investing, and doing business, globally, is one of the few ways to reduce your risks and increase your gains by not putting all your eggs in one basket.

25. Trust your instinct.

A reasonable percentage of the things listed above, are things that I was aware of as an 20-year-old.

Staying true to yourself and your instincts, especially if you get the tough knocks early on, is important.

Pained by financial indecision? Want to invest with Adam?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.