I often write on Quora.com, where I am the most viewed writer on financial matters, with over 479.1 million views in recent years.

In the answers below I focused on the following topics and issues:

- What are the political impacts on stock markets?

- Why is it so hard to time the stock market?

- Can people live off their savings and never work again, or do they eventually have to start working again?

- What are some common misconceptions about Bitcoin?

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Some of the links and videos referred to might only be available on the original answers.

Source for all answers – Adam Fayed’s Quora page.

What are the political impacts on stock markets?

In the long-term, there is less of a connection than people expect.

There are exceptions. When things are very extreme, of course it has a huge impact.

During certain revolutions, such as the Russian Revolution, the stock markets were closed down.

The Syrian stock market was closed due to the civil war recently.

Likewise, even in some Western economies, the stock market was closed during certain periods of global war, only to reopen a few months or years later.

Yet in less extreme times, it has less of an impact than people think.

A few examples:

– The UK stock market hit a record high a few years after the Brexit vote

– US stock markets did well during the Cuban Missile Crisis.

– Stocks did quite well during the Spanish Flu epidemic and certain periods of war, including World War One, which happened during the same time as the pandemic.

– Most asset prices did well during the recent pandemic in 2020-2021

-US stocks hit records in the aftermath of the disputed 2020 election.

– Various stock markets have gone up during terrorist attacks

– The US stock market hit various records during the North Korea “crisis” of 2018, at the same time as a partial trade war with China.

Even when asset prices have fallen during times of political turmoil, there isn’t often a direct connection.

What may be true is that investors factor in long-term political risk. An example is that price:earnings ratios for the US stock market are higher than many other stock markets.

One of the reasons for this is that global investors perceive that stock market as being less risky compared to most others.

It has a good long-term track record, there has never been a serious threat of political revolution that closed down the markets permanently, and most US firms are international anyway, meaning that investing in the market is more like a global play.

In other words, US firms can still grow if they are doing well globally, even if there is political instability at home.

Conversely, a market like China clearly has more political risk. In a one-party state, it is easier for the party to just close down the markets, or restrict companies, as happened with Jack Ma.

There is just no indication that short or even medium-term political risks always results in lower asset valuations. Look at the UK recently. A historically stable country.

Now is is less stable, but still with the rule of law, democracy and a weaker currency, which makes valuations look more attracted.

That weaker currency means many overseas investors are looking to UK assets, such as stocks and real estate, as being bargains.

So, sometimes, even where asset prices go down and risks increase, investors are willing to get in. That happened during Brexit. It affected prices for a few months, but not two years later.

One of the best papers conducted on this is here – Historically, Geopolitical Risk Has Had Little Market Impact

As per the title, “Historically, Geopolitical Risk Has Had Little Market Impact”.

We also have to make a distinction between individual stocks and the overall index. It is much more likely that an individual name, such as the Chinese firms listed in the US, gets affected by politics.

In extreme cases, they can even get banned. Look what happened to ZTE’s stock after Trump targeted the technology that was essential for their operation.

The overall market of say 500 firms, as is the case with the S&P500, is different, as some stocks in the index can even gain from political instability or changes.

Why is it so hard to time the stock market?

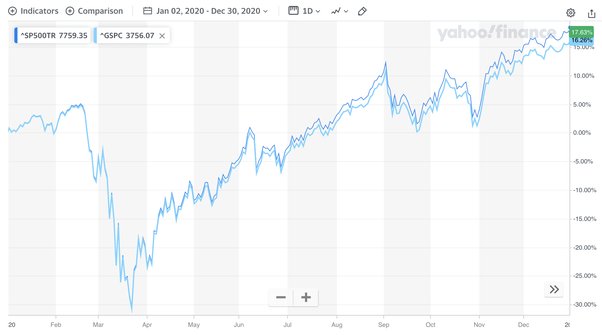

Let’s take the most extreme year in the stock market in recent times…….2020.

As per the graph from Yahoo Finance above, the market was up about 16%-17% for the year.

It started the year trading at record highs. There was a 50% fall, and quicker than average recovery.

Markets had a shaky October and “everybody” was worried about a disputed election between Trump and Biden.

That disputed election happened and markets were up the next day. About a week later, Pfizer’s vaccine was announced.

Markets soared.

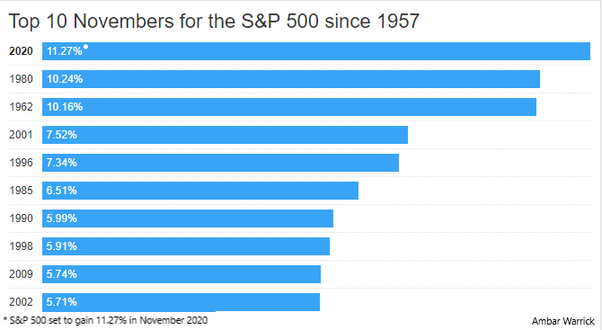

The market was up 11% in November, and people were incredibly pessimistic on November 1:

So, the stock market produced almost 20% in 2020.

Yet only 18 days from 365 days produced those returns. Most days were negative/down, even or very marginally up.

If those 18 days didn’t happen, the market would have been down for the year. Some of those days happened during unexpected moments, such as in November.

The same is true in many years. The vast majority of the gains for the stock market can occur due to a small minority of “big days and weeks”.

I expect something similar to happen this time. It is less extreme than in 2020. Markets are down over 20% from their peaks, and less in markets like the UK.

Yet I expect that the recovery will come during an unexpected moment, and more quickly than people think once it begins. We just never know when that time will come for sure.

That isn’t to mention dividend reinvesting and the opportunity to balance between different positions in a portfolio.

Stock markets, on average, produce 2%-4% dividends per year. That often increases during moments when the markets are sharply down.

Reinvesting that makes a big difference to returns, and you can’t do that if you are in cash:

Just as a good real estate investor doesn’t just focus on capital gains, and instead also looks at rental yields, a stock investor shouldn’t only be focused on capital gains.

Can people live off their savings and never work again, or do they eventually have to start working again?

It is possible, theoretically.

Historically, cash has never beaten certain assets like stocks long-term. It has just been less volatile, but it did pay an above-inflation amount.

In the UK in the 2000s, you could make 2%-3% above inflation with money in the bank, with a relatively stable currency.

Many developed countries had a similar situation. Japan was the outlier with 0% inflation at best and 0% interest rates.

After 2007, inflation was averaging 2%-3% per year, and the banks paid 0.1%. In the last year, inflation has increased to 7%-10% in most countries, and the banks pay 2%-4% in most cases.

Therefore, real interest rates are lower than ever. It is very unlikely that somebody can retire from cash alone, unless they have loads of it.

Even if they have loads of it, it is risky. With age expectancy rising, the number of people who will live to 90 and over 100 will skyrocket.

If you retire at 65, you could easily live for over 35 years. If you early retire, it could be half a century!

Let’s say somebody has $20m in cash and no debt and they plan to spend 200k a year. They get 3% below inflation in the bank.

Here are the results:

- 5 years. Inflation-adjusted (IA)they have 16.2m

- 10 years. 13m (IA)

- 20 years. 7.9m (IA)

- 30 years. 4.1m (IA)

- 40 years. 1.2m (IA)

- 45-46 years – they run out of money.

And that is from 20m. Most people don’t have that, and it is also assuming that something extreme doesn’t happen.

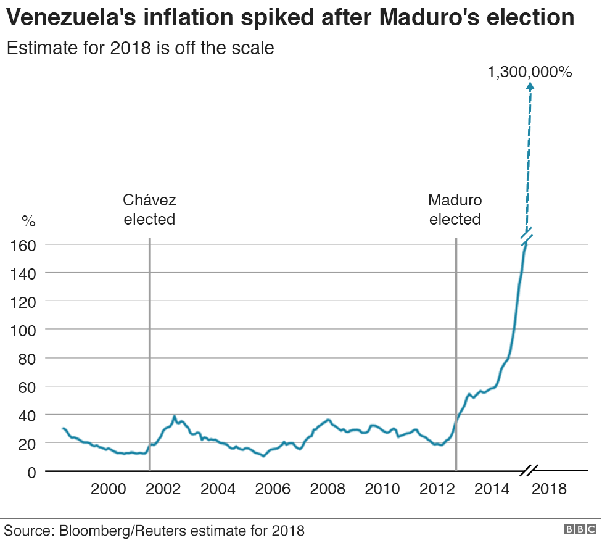

There are many formerly wealthy Zimbabweans and Venezuelans who put too much money in the local currency.

This is what inflation looked like in Venezuela:

The most realistic and safe way to early retire, is to build up a diversified international portfolio, and other take out 3%-4% of the total investment pot long-term.

Avoid too many illiquid assets like property, private equity etc. Some is fine, but liquid assets are essential in retirement.

Doing it this way means it doesn’t matter if one market, sector or asset class performs badly as you haven’t put all your eggs in one basket.

That way, you will see the portfolio fluctuating, but you shouldn’t run out.

Putting all your assets in one currency is as risky, in some ways, as investing it all in just one stock, as your whole wealth can fail if something extreme happens.

What are some common misconceptions about Bitcoin?

This question was asked years ago.

With the benefit of hindsight, even advocates of Bitcoin would admit that Bitcoin hasn’t been:

- An inflation hedge

- A hedge against the stock market falling

- A hedge against central banks printing money

- An asset you can rely on in difficult times. A safe heaven.

- Digital gold.

- A hedge against anything really

Its best periods have been during times when other assets, such as technology stocks, have been doing very well.

The worst times have been during uncertain periods, such as this year, when inflation and interest rates are rising.

Perhaps the biggest misconception people still have is that Bitcoin will separate the state from money.

This is something many libertarians want, and in theory it is a great idea.

Bitcoin, regardless of whether the price goes up or down, is very very unlikely to do this.

Governments will either take over the space with their own digital money, regulate it or find a way to trace it.

The idea that one day we will all pay with private coins for things which the government can’t trace, is for the birds.

Even if Bitcoin eventually succeeds, which is a big if, it is more likely that this is like the early days of the internet.

In other words, most projects fail, just as most technology firms went to the wall. A few succeed.

The space gets more regulated, just as the internet was once the wild fast, and eventually the “big boys” gain from regulation.