I am often asked my opinions about index funds and ETFs.

Index funds, and index-linked ETFs, just track the stock market. For example the FTSE 100 tracks the 100 biggest UK firms.

The S&P500 tracks 500 of the top US firms. Such funds and ETfs, don’t, therefore try to beat the market by investing in companies that could outperform.

They simply give you the performance of the stock market minus a small fee.

I am asked the following questions by my followers on a regular basis:

- Are index funds good investments?

- Are index funds and ETFs the same thing?

- Does the fact that people would be down on a Japanese index fund bought decades ago weaken the argument for index funds? Or if something like the Great Depression happens again, should people be worried about using the indexes?

I have answered all these questions, on various platforms, in recent years. I will list some of these answers in this article.

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to email me (advice@adamfayed.com) or WhatsApp (+44-7393-450-837).

It is especially important for people with very specific financial requirements, like expats or people that live in countries where it is difficult to buy indexes directly unlike in places like the US, to seek professional guidance.

This can avoid unexpected surprises and the typical pitfalls that do it yourself (DIY) investors face.

For people that prefer visual content, I have made videos on how to invest in US index funds from Europe and beyond:

I have also spoken about the best index funds for beginners.

What are generally the best mutual funds, ETFs to invest and the steps to actually get in and be part of one?

Source: Quora Adam Fayed

For the model portfolios below, the best ETFs or funds are often provided by Vanguard, iShares or a few other firms. The fees are very similar. For UK investors, HSBC has some of the cheapest funds, with the HSBC FTSE 250 Tracker being one of the cheapest in its class.

I would advise readers not to get overly preoccupied with choices. Jack Bogle said in an interview that for most investors, choice is a bad thing, “Choice is your enemy because you choose based on one thing: past performance. But past performance does not recur.” So the best thing to do is to look for the cheapest index funds.

With that being said don’t worry about 0.10% vs. 0.09% fees or some small details. Don’t overcomplicate the task at hand. Just focus on building a simple, low-cost, diversified portfolio. With the benefits of time and staying invested for the long-term, the rest will fall into place.

For ultra-simple portfolios, an investor can hold two indexes. An international stock markets ETF and international bond index. I would suggest having 3-4 indexes. One, your home country’s index if your home country has a well-established stock exchange, and also emerging markets alongside international stock and bonds index.

The following example portfolios are also adjusted to a person’s age, and depending on their nationality:

Model portfolios for American citizens and expats under 40 –

60% US Stock Markets,

20% International stock markets,

10% Emerging stock markets

10% US short-term government bonds

Model portfolios for American citizens and expats over 40 –

50% US Stock Markets,

20% International stock markets,

5% Emerging stock markets

25% US government bonds

Model portfolios for American citizens and expats over 55 or close to retirement –

50% US Stock Markets,

20% International stock markets,

30% US government bonds

Model portfolios for British citizens and expats under 40 –

40% UK FTSE All Shares

40% International stock markets,

10% Emerging stock markets

10% Global government bonds index

Model portfolios for British citizens and expats over 40 –

35% UK FTSE All Shares

35% International stock markets,

5% Emerging stock markets

25% Global government bonds index

Model portfolios for British citizens and expats over 55 or close to retirement –

35% UK FTSE All Shares

35% International stock markets,

30% Global government bonds index

Model portfolios for European citizens and expats under 40 –

40% Euro Shares

40% International stock markets,

10% Emerging stock markets

10% Global government bonds index

Model portfolios for European citizens and expats over 40 –

35% European All Shares

35% International stock markets,

5% Emerging stock markets

25% Global government bonds index

Model portfolios for European citizens and expats over 55 or close to retirement –

35% European All Shares

35% International stock markets,

30% Global government bonds index

From the above figures, one can work out what kind of portfolio you should be aiming at, depending on your nationality. If you are from a country which hasn’t got a history of

For investors who want a diversified portfolio which includes REITs and international stocks, I would suggest the following portfolio:

10%- Global REIT ETF. Either iShares or Vanguard

55% – Vanguard Total World Stock Market ETF

35% – Vanguard short-term inflation protection securities ETF

Next step, decide whether to DIY or use an advisor.

What are my options of investing in index funds in Australia and can you provide me with direct links to invest?

Source: Quora Adam Fayed

Some links are below. There are countless options for investing in Australian markets via index funds, or indeed international markets from Australia.

Just like anywhere else, the best thing is just to invest in a manner which are low cost and long-term.

Mainly in equity markets, but also some in bonds, unless you are young, in which case 100% in markets is fine.

I think with the recent housing market correction in Australia, more and more people will consider low-cost online investing.

What is your review of Vanguard Index Funds?

Source: Quora Adam Fayed

Vanguard index funds are some of the best in the market, but a lot of people have certain misconceptions about them.

To confirm, iShares, BlackRock or HSBC index funds, tracking the same index, will perform almost identically to Vanguard.

In fact, iShares is actually slightly cheaper now, on many indexes, but it doesn’t make much difference.

The fees, performance and so on, is all similar. Another huge misconception is that all index investors get better returns.

They only get better returns if they buy and hold…..which they often don’t do!

I was reading the founder of Vanguard (Jack Bogle) book recently. It is the one below;

He was pointing out, that many so-called passive investors, actually trade these index funds.

It is one reason why he opposed index-linked ETFs as per his quote below;

And he is right. Nobody should want to check their valuations daily or trade daily.

These are instruments to buy and hold. That is one reason the index funds can be better than the index-linked ETFs…..people are less tempted to sell instantly.

Is there any reason to not invest in index funds?

Source: Quora Adam Fayed

The biggest reason is an investors mindset. Some people would say “if you are 60, you shouldn’t be invested in index funds due to the risk”.

In other words, markets might go up big style long-term, but there are many negative years and even 5–10 year periods.

So the 60 year old, unless he or she works until 75+, can’t compound and gets a lot of the risk.

That, however, is a good reason to be 40% in bond index funds and 60% in equity index funds.

I think the biggest reason for people to not go into them, is their mentality.

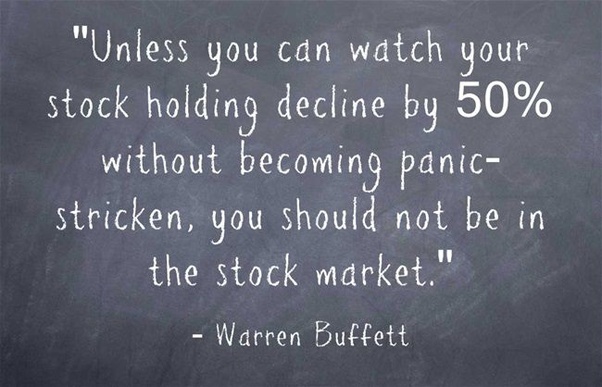

If you will pee your pants every time there is a 20%, 30% or 40% decline in stocks, you will probably not do well in these buy and hold instruments.

This quote sums it up:

And yet that is exactly what people do. 2008–2009 was a unique time to buy stocks at huge discounts.

They recovered 300%+ since then. Yet the outflows from Vanguard index funds were huge.

Inflows were highest during 2009…..and that is the problem. People need to invest through thick and thin, either by themselves or with the help of an advisor who acts as a behavioral coach as well as advisor.

In other words, somebody to stop you panic selling when the times are tough.

Markets go up and down, even if they have always historically gone up big-time long-term.

What should I know about index funds?

Source: Quora Adam Fayed

The main things is they are tools and not a strategy. They are a great way to invest, but the keys are your strategy and not the tool.

Some simple examples about what I mean by strategy:

- Investor A might only be invested in the S&P500 for 5 years.

- Investor B might Investor A might only be invested in the S&P500 for 50 years from 20–50

- Investor C might be 90% in the S&P500, and 10% in government bonds and never rebalance.

- Investor D might be 90% in the S&P500, and 10% in government bonds and rebalance yearly

- Investor E might be 98% in the S&P500, 10% in international and 10% in government bonds and rebalance yearly

- Investor F might try to time when to get in and out of the market using index funds

- Investor G might try to “market hop” every time there is a move in one market or another. For example, the China index-linked ETF, sell it, and go for the MSCI Europe index-linked ETF

- Investor H might not reinvest dividends whilst Investor I does just that.

Many people forget this crucial point. Most people who have read a decent amount about markets know how much money they could have made just tracking the markets for decades had they started earlier.

And that is very true, but it assumes reasonable behaviour from the investor.

I met a guy about a year ago who invested with the Vanguard Group.

He said he was investing for years but, quote, “stopped after Trump got elected as I was nervous about markets”.

This behaviour goes completely contrary to a good strategy and indeed the Vanguard Group’s advice and that of its founder – Jack Bogle.

Studies have shown that investor in the indexes lose to those indexes by 2% per year minimum.

The main reason is they often pour in more money during the good times, and panic during the bad times.

In comparison, dead people’s accounts almost always outperform the living.

So a level-headed, long-term strategy is key. One that doesn’t change based on the news or sensationalist headlines.

Every time there is a crisis, the call is always the same. It usually goes something like this:

Even though every crisis is different, one thing stays the same. The biggest firms, the cream of the crop, will get bigger over time due to the survival of the fittest.

Now sure, we don’t know which companies will go bust and which will get bigger.

Many big firms have gone bankrupt before like Lehman Brothers just 13 years ago.

However, the top 5, 50 and 500 firms are now more profitable than the top firms in 1950.

Likewise, I am pretty sure that barring a nuclear war, the biggest firms on the indexes like the S&P500 and Nasdaq will be more profitable in 2050 than those on it today.

We just don’t know which firms will be on there for sure.

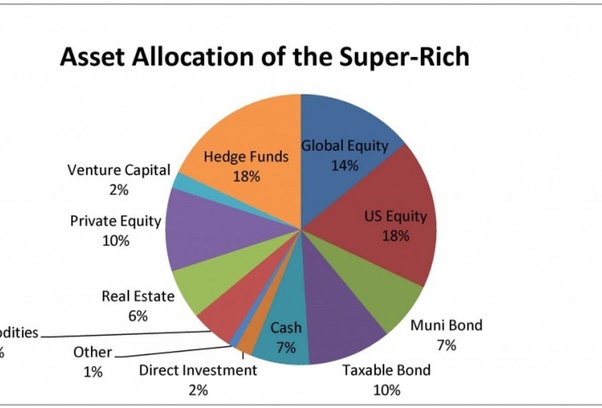

Why don’t the wealthy use index funds?

Source: Quora Adam Fayed

They do. Many people get wealthy from long-term investing, so there are many mid-income wealthy people in index funds.

What is true though is that many ultra-wealthy either want to beat the market, or believe it or not are petrified of losing.

That is one reason they sometimes over diversify and use funds which have lower volatility – they are petrified of declines vermin loses.

It is a huge misconception that ultra wealthy people get better returns.

What is the best way to start investing in index funds?

Source: Quora Adam Fayed

Find a platform or advisor that will accept you. Don’t engage in analysis paralysis. Whether the index funds you decide on is company x or company y, it won’t make much difference.

Also read about why most DIY investors fail when they buy various funds, including index funds.

Could save you a fortune.

Is it really a no-brainer to invest in index funds?

Source: Quora Adam Fayed

Yes but only if you do it right. Using index funds is like using knife. A knife in the hands of a doctor can save your life.

A knife in the hands of a monster can kill you. with investing, it isn’t quite as dramatic as that!

But what is true is that investor A, can get 4% or less, and investor 2 can get 8% or more.

They can get these returns despite being in the same index funds! How is this possible?

The main reasons are:

- Actively trading them

- Just because the returns are high, doesn’t mean they are always high

- They are high on any long-term horizon

- However, there are always year and the odd decade where they don’t do well

- Examples. 1960–1990 was 10% per year average, but 1965–1982 was close to 0% in real terms

- 1990–2011 was also about 10%, but 2000–2010 was stagnation

- Many people look at these figures and say, wow, if I could only just find the right time to buy! In that case, I wouldn’t make 10%. I would make 15%+, because I would buy during the good years (1982–1990 and 1990–1999 in this case) and avoid the bad years (65–82 and 2000–2010 in this case)

- It isn’t that simple. Market timers lose

- Beyond market timing, some people try to be invested 100% of the time but take `active positions`. In other words, sell 100% of US stocks after Trump’s election victory, take a huge position in Chinese Stocks after the crash

- In other words using passive investments to take active positions. That doesn’t work

2. Long-term

- Person A, who invests in index funds for only 5 years, may get +20% per year returns. They may get -10% yearly returns too

- It is more like gambling. Not as much as individual shares.

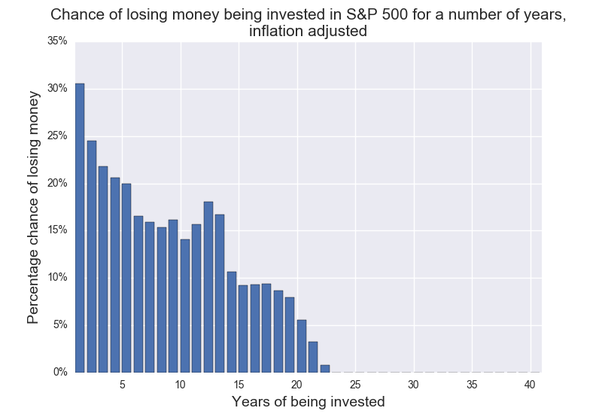

- Indeed as per the stats below, you do have a 80%+ chance of `winning` over a 5 year period

- However, if you buy and hold from your 20s and 30s, until retirement and beyond, your chances of losing are close to 0%

- Historically it has never happened where somebody who has held onto the S&P for 25–30 has lost, never mind 50 years!

So the keys is using index funds in the correct way. Otherwise they are a blunt instrument.

Are index funds overrated?

Source: Quora Adam Fayed

I don’t think they are overrated if they are used correctly. What is overrated is the statement that “index funds investors are all making the right decision”, or are super rational and so on.

What has lead to an increase in indexing? The following things have helped:

- In the last 10 years, many countries have banned commissions (upfront) for advisory companies. So it is normal for firms in Australia, America, the UK and elsewhere, to just charge fees. In other words, the advisors get paid the same, regardless of which funds they pick. So more advisors are putting their clients money in index funds

- Many investors buy on familiarity. In the same way many investors buy HSBC or Morgan Stanley funds because they know the name, I am not sure all Vanguard investors know the difference between active and passive. In fact, I would be willing to bet, globally, at least 30% don’t.

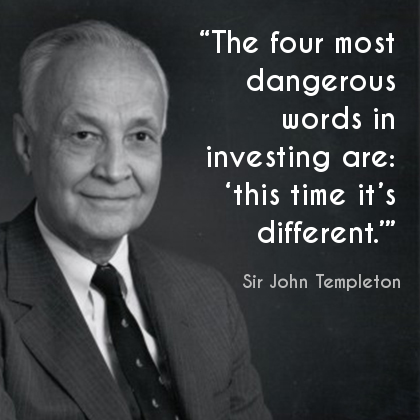

- Even if they do know the difference, many of these investors aren’t using them correctly. Net inflows for Vanguard tend to be highest when the markets are going up (1999 and these days) and lowest when the markets are going down (2018, 2009 etc). Even the founder of Jack Bogle warned how index funds could be used this way, when index-linked ETFs were invented:

Even a few weeks ago, I met somebody who admitted he stopped investing due to Brexit and Trump.

So if index funds are used in the wrong way (used to be active rather than passive) then they are over-rated due to human error and not the funds.

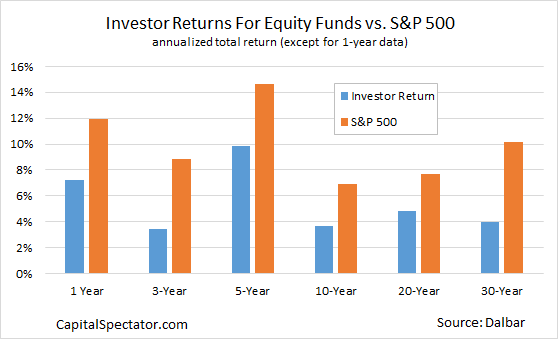

This is the biggest reason for these results:

One of the biggest errors most DIY investors make is chasing recent returns – “recency bias”.

So countless investors lose faith in markets when the going is bad, and get excited when the going is good.

So they buy high and sell low. Best to just invest for decades. You will get great years like this year (+25%), bad years like last year, terrible years like 2008. But your average returns will be good if you use them right.

If they are used as intended, as buy, hold and rebalance they are great, focusing on both bond and stock markets.

Why do people invest in real estate over index funds?

Source: Quora Adam Fayed

If you think about it, with the exception of the generation coming up, we haven’t been used to thinking about intangible products as safe until recently,

In other we are born into a house or apartment. We have the four walls around us.

So it is a tangible product that anybody can understand. That doesn’t mean that most people are professional real estate investors.

Yet we do feel like we know the basics about real estate investing.

This creates familiarity bias. As humans we are more reassured by what is familiar.

This is one reason we are more likely to buy stocks in our own country, even if we aren’t nationalists:

It is the same reason why we are more likely to buy Amazon stocks if we live near the warehouse or buy our own company stocks, even though rationally speaking, we shouldn’t want to double our risk if the firm goes bust.

So with index funds, they have been around for decades, and been very profitable for decades.

But how many people have bought index funds for decades? Very few.

It has only become normal in the last 10–20 years, so only now, are people comfortable with it.

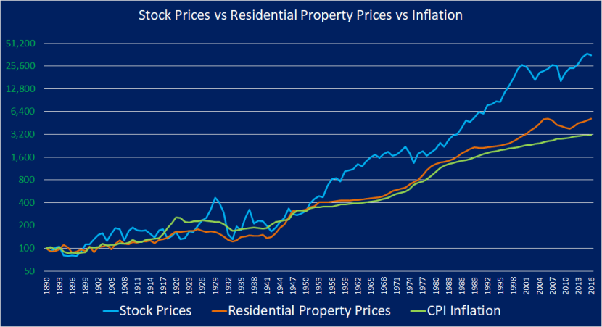

Added to that, and the media always give out ideas like “property is safer than stocks” when long-term, it struggles with highs costs:

I don’t think it has to be either/or. Even though I am not a huge fan of real estate, REITS and rental property can be a great idea, but only if you use it correctly.

With property though, it has to be used in a very careful way, and your primary residence is merely a home and not your pension.

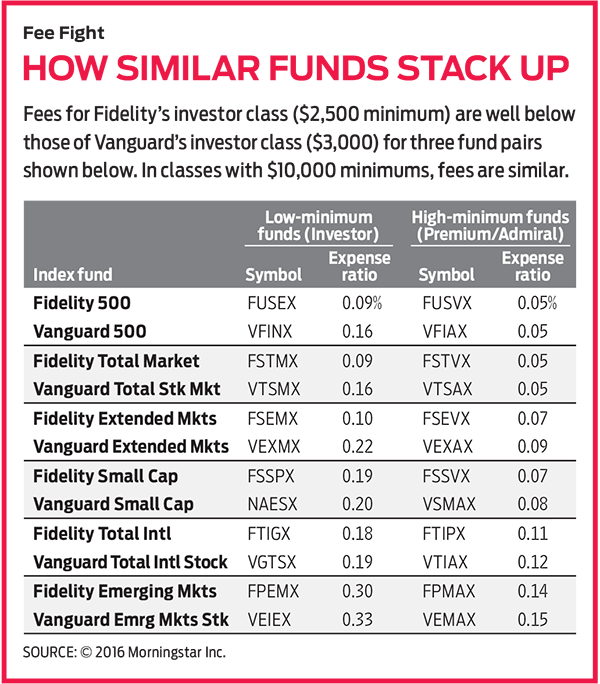

Is Vanguard the best place for index funds?

Source: Quora Adam Fayed

It is no better or worse than most other operators these days. Look at the stats below:

Fidelity has almost identical fees and indeed performance as Vanguard.

So does BlackRock, iShares and countless others. So Vanguard funds are fine for index trackers.

They are merely no better or worse than most of the rest these days.

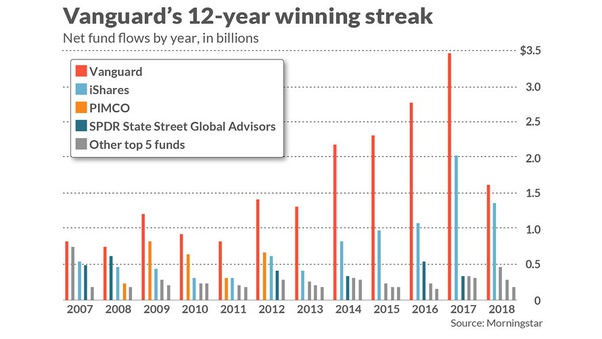

What has happened is that people are reassured by Vanguard’s brand name:

So the gap between them and the rest seems to continue to grow.

How should I invest my money during the coronavirus crisis?

Source: Quora Adam Fayed

This answer might shock you because it will show why investors during the Great Depression, actually could have made a profit barely a few years later……but more on that below.

Firstly, a good investor should imagine they are controlling a catapult.

You need to load it with “balls”. The more balls you loads into the catapult, the better for your “attack”.

This is what an investor often needs to do. In your working years, you need to fill the catapult with units, and then “fire” (sell) these units in retirement.

The lower markets get, during the virus, means the more units you can “fill up on”.

So take the Vanguard Total Stock Market ETF (VTI) as an example.

The price now is $123.31. So if you have $15,000 to invest today, you can buy 121.64 units.

In comparison, imagine the price was $62 – about half of what it is now.

In that case you can buy 241 units. So rationally speaking, a young investor should want markets to fall, and somebody approaching retirement should want them to rise, as they will want to be net sellers.

I will give you a simple example of somebody profiting from the Great Depression.

Let’s say somebody bought the Dow Jones in 1929 right at the outset of the biggest financial crisis ever – I know index funds weren’t available in 1929 but stay with me while I illustrate a point.

Let’s keep this simple and say they invested $10,000 a year (adjusted for inflation) from 1929 until 1960 when they retired.

They would have made an absolute fortune. More than if markets had kept going up in a straight line!

In fact, they would have made about 12x-14x more than they put in, despite all of the deflation of the 1930s.

Why? The markets had a brutal 90% fall from the absolute peak to the absolute bottom and stayed low for years.

So during those years that young investor (or even middle aged person) in the early 1930s, could have “loaded up” his balls for the catapult for a few years.

What about somebody with a lot of money already invested?

You might say, the last example only works because somebody who invested $10,000 a year (inflation adjusted) from 1929 until 1960, only invested during a few “awful years” when they had less invested.

In other words, it wasn’t as if they had 100k invested on day 1. They were only getting started during the worse of the crisis.

So let’s look at another example:

“Person 2” had a 100k lump sum (inflation adjusted again) invested in 1929 + they add 12k a year in each subsequent year.

How scary you might say! They invested 100k just before a 90% decline!

So how many years would it have taken their portfolio to recover?

1930 = 112k contributed. Account value = 76k. A big drop

1931 = $124k contributed. Account value = 54k. A massive drop

1932 = 136k total contribution. Account value = 54k. An even bigger drop!

1933 = 148k contribution. Account value = 90k. Green shoots!

1934 =160k contribution. Account value = 98.7k

1935 = 172k contributed. Account value = 150k

1936 = 184k contributed. Account value =……….232k!

So the account is up substantially within 6–7 years of a Great Depression…..despite having a decent sized lump sum at the beginning!

The reason is simple. Markets might have declined 90% from the very top to the very bottom, but by patiently investing during this down market, this investor has “filled up their catapult with units”.

And that isn’t factoring in:

- Deflation which was huge in the 1930s

- If you rebalanced from bonds the figures above would be huge

- Of course if this investor would have carried on for 10–20 years more, the returns would have been bigger.

A more recent example – The Nasdaq

From 1995 until 2018, the Nasdaq produced about 12%-13% per year for a lump sum investor but from 2000–2002, it fell by 76%!

Yet somebody who bought extra units during that period would have gotten even higher than 13% returns for obvious reasons.

Why? The Nasdaq was 900 in 1995. 5,050 before the crash in 2000.

It hit 1,200 at the bottom in 2002 and stayed low for years, before hitting 10,000 1–2 months ago, before the recent fall. It also fell a lot in 2008.

So somebody who rebalanced from bonds into the Nasdaq from 2000–2002 and 2008–2010, and monthly invested via their salary, could have made up to 15% per year, by taking advantage of the lower valuations.

I am not implying that people should focus on the Nasdaq over the S&P500.

I am merely saying an investor shouldn’t fear big falls if they rebalance and/or are young enough to deal with the volatility.

So surely an investor should just wait for the right time to get into the markets?

It isn’t that simple. Nobody can predict what will happen to markets, even though they have always historically came back to hit record highs.

So the easiest thing is just to buy index and bond funds. Short-term government bonds went up during the last month, but medium term ones fell.

If you have $100,000 invested and $70,000 is in markets and $30,000 is in government bonds, and markets dip again, add more and rebalance from the bonds.

Don’t try to focus on if your portfolio is going up or down during the crisis.

Focus on what things will look like in 20–30 years or whenever you plan to retire.