Understanding investment principles is fundamental in achieving long-term success in the global market.

In this blog I will list some of my top Quora answers for the last few days, which focused on many interesting subjects.

In the answers shared today I focused on:

- What should you do to invest successfully, and for that matter, see improvements in your financial life? It isn’t all about big sudden improvements either. The answer below looks at how incremental improvements makes a huge difference long-term.

- What happens once people have money and power? What motivates them? Of course it depends on the person, but I consider some of the main reasons some wealthy people give more money to charity as they get older.

- What percentage of your wealth should be invested in “risky” assets, if any, and how do I define risk? Too many times people confuse volatility as risk.

- Was investing just “created” as some kind of conspiracy to make the rich get richer? I tackle this ridiculous suggestion in my last answer.

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me via email or Whatsapp.

What should you do to invest successfully?

Source: Quora

It is a very broad question, but let me start with an analogy. Let’s say you want to lose weight.

You don’t want to do anything extreme, so you gradually reduce your calorie intake:

Cutting say 1% from your calorie intake and increasing your exercise levels by 1%, won’t make a big difference in a day or a week.

Even in 3 months, you might not notice it that much. Yet over 10 years it will all compound and make a huge difference.

The same is true in anything to do with investing or personal finance.

Every decision you make, be that income, spending habits or investing habits, compounds over the years.

Examples include:

- Starting to invest from a young age, as opposed to an older age, could add millions to your investment pot, even if your returns aren’t spectacularly better than your peers.Simple example. Let’s say Andy started investing in 1950, when he was a young man, until now, when he is an old guy. He invested just $400 a month on average for that 70 years. Ben invested $2,000 a month for 15 years. They both got the average return of the S&P500 index – so neither did anything special in that regard. The figures are all inflation adjusted of course. The results? Andy would have about $72million, yes $72million, and Ben $900,000. Now it should be obvious why even some cleaners can become multi-millionaires – A janitor secretly amassed an $8 million fortune and left most of it to his library and hospital

- Just being a good negotiator and getting an extra 1% per year than most people in your industry get, could make a huge difference long-term. Same as a private business owner. That extra 1% can make a difference.

- Knocking just 1% of your speeding, and reinvesting it, could also make a huge difference long-term.

- Just staying cool through every market crash, and not panic selling, could save you millions in your lifetime. I was speaking to one of my friends about this. He was mentioning how some of the people he knows never got back into the stock market after the 1987 stock market crash. Stocks have subsequently gone up more than 20x including dividend reinvestment.

- Consistently taking slightly more calculated risks long-term than your peers, will make a huge difference over the decades. Just taking one more calculated risk in a lifetime than the average person is unlikely to yield a great return.

- Reading even slightly more often than others will make a huge difference long-term.

- Focusing on implementation rather than ideas makes a huge difference. If you get into the habit of making more decisive decisions more often, and consistently, than other people, this advantage will also compound.

- Adapting just a little bit better than other people, and businesses, can make a huge difference long-term. Look at the last 20–30 years. Firms that went online more quickly, have seen bigger improvements over time, compared to more conservative firms. Then the lockdown came along and the difference has been huge.

- If a business reduce their spending by 1% and increase closure rates by 1%, it can increase profitability by more than 30%, if the results are replicated over many years.

- Improving sleep and taking care of your healthy even a bit more can help your finances indirectly as well.

Of course, not everything is about gradually improvements. There are some ways to improve more dramatically.

The point is that it isn’t all about “hitting home runs” and being amazing 24/7.

Sometimes consistently good behaviour can equal something huge long-term.

So, in answer to your question, I would say good investing requires consistently good behaviour for the long-term.

What do people want after they have wealth and power? What is the next step to the unreachable “happiness”?

Source: Quora

People are motivated by different things. Wealthy people aren’t a monolithic group that think the same.

Just like other groups, some people are relatively content and others aren’t.

You are right in one sense, that it is human nature to always want something you don’t have.

That could be time, money, influence, power, fame, status, a family or many other things.

As a broad generalisation., most wealthier people care less about money and material things as they get older, and they care more about family and giving back to the community through charity.

There is a simple reason for this. When you have more of something, adding more of that something has declining marginal utility.

The first cup of water after a run tastes fantastic. The second less so. The fifth doesn’t taste nice at all, but it is the same product.

The same is true of wealth and money. Going from poverty to middle-income can make a huge difference to your mental health.

It can lead to less worries and more choices. Going from middle-income to upper-middle can make a difference too, as can converting some of that income into wealth, because wealth gives you security which income alone doesn’t give.

Somebody isn’t economically secure if they can’t live without an income for a few months, even if they are earning millions.

The point is though, once you go beyond a certain threshold, it doesn’t matter as much.

Going from earning $500,000 after tax to $3m doesn’t make that much difference.

Going from $10m wealth to $100m doesn’t make as much difference as people think.

That is one reason why many older wealthy people seek to leave a legacy.

Buffett and many others didn’t get involved in charities until they were into their 50s, 60s or even 70s.

Younger wealthier people are more likely to want to keep growing their wealth, which is a rational decision, considering compounding will ensure it gets bigger.

I remember Buffett mentioning how his first wife wanted him to give money to charity in his 50s.

He explained that it would be rational to delay giving for another decade or more due to compounding – the charities would get more money if he delayed giving.

I am generalising of course though. People are different and motivated by contrasting things.

As an aside, I think people are more likely to be depressed if they slow down, regardless of their income and wealth.

So oftentimes just keeping active in a core business, charity or hobbies can help prevent depression.

What percentage of your wealth would have to be invested in the risky asset?

Source: Quora

It depends on the following things:

- How you define risk

- How long you will invest for

- How wealthy you are

- How much you can afford to lose

- Sometimes your personal situation like if you have any dependents

Firstly, risk isn’t volatility. The Nasdaq has been one of the most volatile index, at least in the developed world.

It has been up, down and sideways. It was stagnant or falling for 14–15 years from 2000 until 2014–2015.

Yet somebody who just bought and hold it for decades has done well.

Even somebody who bought at the top of the 2000 peak and didn’t add a penny when it was cheap in 2001–2006, has done well.

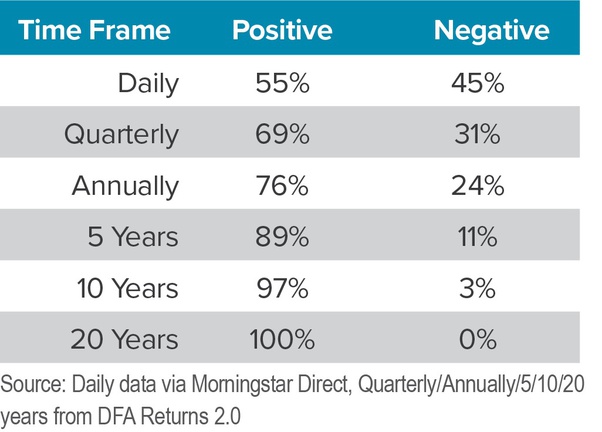

Same with the S&P500. It has been volatile, albeit less than the Nasdaq, but not one person who has bought and held it for decades has lost money:

I don’t know about you, but I don’t consider an asset class risky that has never let down a long-term investor.

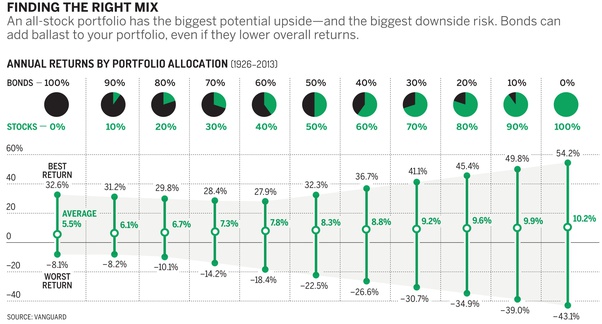

People assume bonds are less risky. All bonds do is reduce the volatility as the graph below shows:

That doesn’t mean you shouldn’t be in bonds. They are a great rebalancing tool when stocks are doing badly, merely lower volatility assets aren’t always less risky.

Some forms of corporate bonds are very risky but have low volatility.

In general, I would define a risky asset as:

- Something which has a good chance of actually losing money. Not going up and down but eventually going higher long-term (volatility), but something which could go to zero. For that reason, property can be riskier than people assume. Professional real estate investors know how to reduce risks. Many DIY investors buy in the wrong places. If they leverage themselves too much or buy in the wrong area, they might default, fail to sell the property and/or fail to find a tenant. Private equity would be another example of a risky asset for a non-sophisticated investor.

- A speculation. Buying an individual stock not based on analysis but due to liking the company or the CEO, would be such an example. Buying oil ETFs just because the price is low is another.

Ideally, even if you have the gambling gene inside you, which most of us do, pure speculations should be kept to 0%. 10% at most.

For the first type of investments, they can sometimes be worth a punt for wealthier investors, if they are about 10% of a portfolio.

The bottom line is that you need to be compensated for your risk.

Taking a big risk to get 10% isn’t sensible. You could have gotten that by buying and holding a Nasdaq or S&P500 index.

Taking a risk to start your own business and making 100,000% makes sense, if you are using money you can afford to lose.

A lot of people know that getting rich slowly from investing is very possible, yet a quicker route to success remains what many people want.

There is not automatically anything wrong with that if you know what you are doing, or are only using money you can afford to lose, but pure speculation is never a good thing.

Was the concept of “investing” created as a way for the rich to get richer?

Source: Quora

No, investing in stocks was created to get capital for firms that need it.

Businesses that want to grow, and the owner can’t raise it themselves, wanted finance.

That included publicly-listed companies and private companies as well.

In addition to that, the majority of people who get rich in investing do it slowly, and are middle-income.

That person that has a $5m portfolio at the age of 65, often started with tiny amounts.

By doing it consistently for decades, and by increasing how much is invested with time, compounding can create a massive portfolio.

This janitor/cleaner had a $8m fortune:

This secretary also had $6m-$8m:

All they did was bought assets for decades – half a century or more in the case of these two.

Most people on modest incomes don’t get to $6m-$8m but remember that 14% of the world’s millionaires are said to be teachers, so you don’t need a high-income to get richer investing.

Often notions like “the rich” is just peddled by certain sections of the media.