I often write on Quora.com, where I am the most viewed writer on financial matters, with over 601.1 million views in recent years.

In the answers below I focused on the following topics and issues:

- Why do rich people keeps on working while they have enough money to spend their entire life?

- When will the US inflation stop going up?Why do rich people keeps on working while they have enough money to spend their entire life?

- Do you think that BRICS will replace the United States Dollar (USD) as a global reserve currency?

- What is the best way to invest in real estate properties in the US from overseas?

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Some of the links and videos referred to might only be available on the original answer.

Why do rich people keeps on working while they have enough money to spend their entire life?

It depends on the persons character.

There are some people who make their money and retire young.

Many keep working, or retire, and then realize it isn’t for them.

This is especially the case for people who run their own businesses.

Kevin O’Leary retired young, and visited as many beaches around the world, before coming back.

There are many people like him.

The reason is simple. It is almost impossible to replace running your own business.

Sure, you can have fun by traveling, partying or learning a new skill.

Yes, you can reconnect with long lost friends.

And absolutely you can have lower levels of stress or “good” pressure.

But what you can’t have is the same intellectual stimulation from building teams and the other things that go along with being a business owner.

It is like a legal high/a legal drug. Stopping doing it is a bit like how many sports stars probably feel when they stop performing in front of a crowd.

I remember Dwayne Johnson was once asked why he sometimes came back to the WWE, despite earning so much as an actor.

His response? Acting is great, but nothing beats performing in front of a crowd.

What is more, if you become semi-retired, you can still have the time needed to pursue hobbies without having the same pressure as when you were thirty.

For salaried employees, it is different. I imagine you reach a certain age and realize that you don’t want people telling you what to do.

That isn’t to mention that it is more difficult to do certain jobs at say 80, compared to taking it easy as a semi-retired owner.

We also have to remember that some “rich” people just have high incomes and aren’t wealthy, so they can’t retire young.

With that being said, everybody should aim to be in a position to retire young, because we never know when our health or desire might go.

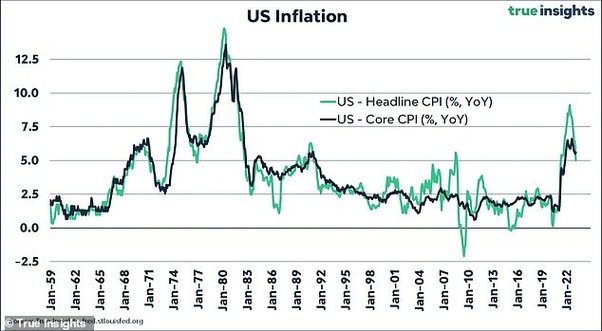

When will the US inflation stop going up?

Not sure if you watched the news yesterday.

Inflation is already falling. Is now at just over 5% in the US, the lowest rate since 2021, as per this graph from This is Money:

That doesn’t mean inflation is “literally falling” – that can only happen if we hit deflation.

Merely, the pace of inflation increases has started to fall from a peak of close to 10%

We are seeing other falls in some advanced countries, even if it is still higher in places like the UK.

As inflation is measured year-on-year, it seems likely that it will continue to fall.

Energy prices are a good example. Petrol prices hit a record in the UK and US last summer, which means that come summer, the inflation read will compare prices to the peaks of last summer.

Therefore, as others have stated, US inflation falling to around 3% by the end of the year seems baked in.

The UK expects similar falls, as do many other economies.

This will likely be good for stocks and certain bonds medium-term.

This is because we should be near the top of the current interest rate cycle, and we can expect rates to start falling sooner than some expected.

If something “breaks” and we get a severe recession, the pace of decelerating inflation will only intensify.

The caveat to that is if some external event happens, such as an oil price shock due to a war.

There are always several unknown variables.

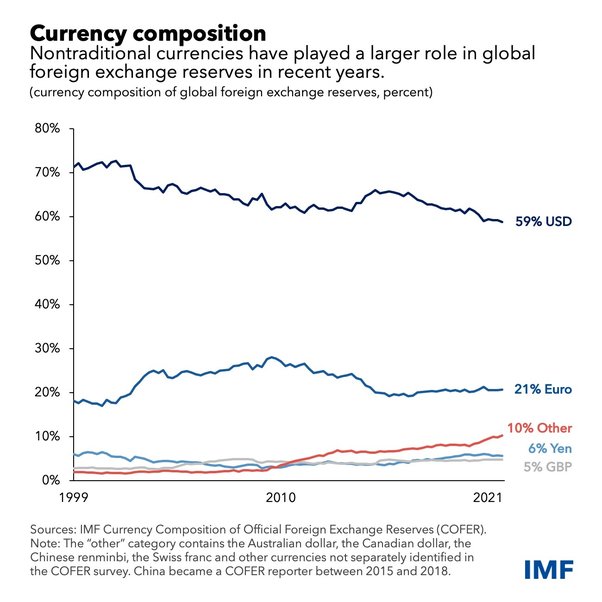

Do you think that BRICS will replace the United States Dollar (USD) as a global reserve currency?

Anybody who is old enough to be over 30, would have heard many stories like this before.

Those over 50, have probably heard such stories on numerous occasions.

People forget now about the talk of the town when it came to the Euro, just as many people forget the predictions about Japan in the 1980s and 1990s.

The Euro went from having 0% market share in 1999 (because it didn’t exist) to well over 20% in 2007, before the Global Financial Crisis.

Many people speculated that the “real reason” Iraq was invaded was because they wanted to use the Euro to trade oil with.

The Euro does still have over 20% of the market, making it comfortably the second most used reserve currency.

That is, however, comfortably below the 28%-29% peak it hit over a decade ago.

Now to come to your question more directly.

I am not saying it can’t happen, merely that it is very unlikely anytime soon or ever for that matter, and that predictions about how things might change are almost impossible to get right.

Remember something – there was another wrong prediction made about the BRICS.

In 2008-2010, after the 2008 crisis, the narrative was that money GDP growth was moving to the global south, and especially the BRICS.

Since then, South Africa, Brazil and Russia have struggled. India has done well. China has grown less slowly than expected in 2010, at least in the last five years, which has resulted in many people doubting whether they will ever overtake the US.

Countries in Latin America and the emerging Middle East have also struggled to live up to expectations set at that time.

Even the founder of the term BRIC (it was known as BRICS before it was made into BRICS), admitted that he only got 2/4 right in 2016.

Now it is 1.5/4 or 1.5/5 due to China’s recent subpar growth and fading future ones.

However, what is true is that given nobody can predict the future with certainty, it makes sense to diversify.

An example of that is buying assets that are globally diversified.

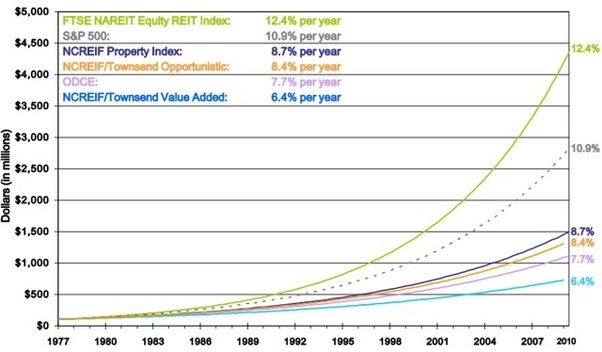

What is the best way to invest in real estate properties in the US from overseas?

‘The best’ is always subjective.

On average, however, I would say through real estate investment trusts (REITS).

The reasons are:

- They have performed well versus more conventional real estate long-term

- They can be held in a portfolio with stocks and bonds so it is convenient.

- You don’t need to arrange a mortgage or worry about all the procedures associated with conventional property such as finding tenants

- Most REIT ETFs are liquid meaning they can be sold or bought instantly. Therefore, if you have an emergency, it is easier to sell $1,000 worth of it rather than release a small amount from a house.

- You can invest in both residential and commercial property.

The only major drawback is that you can’t leverage with a mortgage.

Yet non-residents buying in the US or UK usually pay higher interest rates and need to put down bigger deposits.

That makes a leverage/debt fuelled real estate strategy more difficult.

Some types of real estate debt projects can also make sense.

Of course, in the post-Covid world, commercial real estate has been disrupted by trends such as home working.

Therefore, you do need to analyse the best REITs for your needs