I often write on Quora.com, where I am the most viewed writer on financial matters, with over 463.9 million views in recent years.

In the answers below I focused on the following topics and issues:

- Why is beating the market so hard?

- Do most millionaires still have their money after five years?

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Some of the links and videos referred to might only be available on the original answers.

Source for all answers – Adam Fayed’s Quora page.

Why is beating the market so hard?

Let me paint you a picture.

Imagine you dropped your phone in Central London, Hong Kong or any other very busy place.

What is the chance of somebody not noticing that phone? Almost 0%. Somebody will notice it. The question is, will they report it, give it to security or steal it.

That is with tens of thousands of people walking nearby. Now imagine the stock market. What is the chance of billions of people, loads of hedge funds, banks and other institutions not noticing that Apple or any big US stock looks intrinsically undervalued?

Even less likely than somebody not spotting your phone. There are people who devote their life to this.

Where you can gain an advantage is

- In private markets. That could be private equity or starting your own business. Private markets and placements don’t work the same as publicly-traded stocks, where all the information is easily accessible. The negative is you will have to spend a lot of time undertaking research if you don’t have an advisor, the risks can be high and it isn’t always liquid.

- In some frontier markets. The US markets are now dominated by the big boys. If you want to stock pick, you might be better in the Vietnamese or Bangladesh small and mid cap market. There is less competition.

- Occasionally, when fear grips the market and institutions need to sell out of positions to cover margin calls, even US and other developed market stocks can get incredibly cheap. Look at 2009. Even with all the uncertainty, the Dow was incredibly cheap ay 7,000, never mind some of the individual stocks. The ability to control your emotions when everybody else is panicking can be priceless.

As an aside, it isn’t that beating the stock market is incredibly hard. A more accurate description would be that beating it consistently, and with the same amount of risk, is very difficult, and that isn’t factoring in time to the return on investment (ROI) calculation.

For instance, if you use leverage/margin loans on an index, you have a great chance of beating the unleveraged index long-term.

The S&P500 has done 11% per year, on average, since 1945, unleveraged. A leveraged investor would have done much better.

But by using debt/leverage, you are also increasing your risks and uncertainties – interest rates could rise or many other things could happen.

This is one reason why even many wealthier investors just focus on having good asset allocation, and controlling risks.

Do most millionaires still have their money after five years?

It is a good question. Most people wrongly assume that “the rich always get richer”, which implies that the same people and families always get richer.

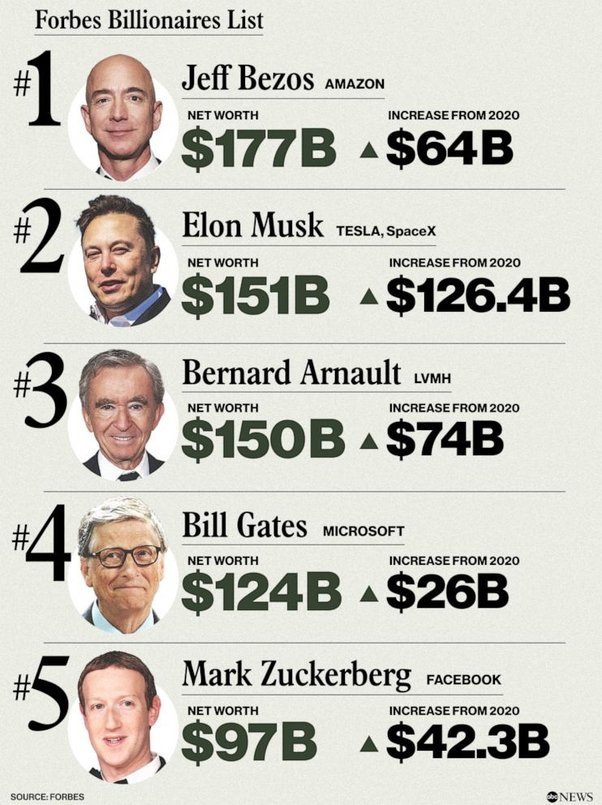

The reality is that doesn’t usually happen. Look at the Forbes and the 2020–2021 list, and other rich lists today.

Few of the people on that list had wealthy great grandparents.

However, most wealthy people still have money after five years. Even fifty years is common.

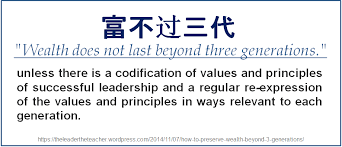

What is less common is having wealth which lasts many generations as this ancient Chinese expression says:

In a UK episode of Dragons Den (Shark Tank), the grandson of the famous founder Cadbury came to ask for money.

His grandad gave the money to charity.

Other reasons why wealth ends is:

- Putting all your eggs in one basket. There are many formerly wealthy people from Zimbabwe and other countries where the political winds changed

- Not planning for unexpected events such as pandemics , ill health, wars etc.

- Family disputes including divorce

- Not adapting to changing market preferences if the bulk of your assets are in a business. Look at Kodak.

- Not having enough liquidity. This can affect business and property owners more than those who own ETFs, cash and other liquid investments.

But losing wealth in five years? You really have to do something majorly wrong to see your wealth disappear so quickly.

The main reasons for such a sudden fall in wealth are likely to be using too much leverage.