Taxes in Portugal for retirees are generally progressive, with most foreign pensions now taxed at standard income rates of 12.5% to 48%.

The end of the former NHR regime means Portugal is no longer a low flat-tax pension haven for new retirees.

This article covers:

- Are Portugal’s taxes high?

- What are the taxes for retirees in Portugal?

- What replaced the NHR in Portugal?

- How is my pension taxed in Portugal?

Key Takeaways:

- Portugal taxes residents on worldwide income, including foreign pensions.

- The old 10% NHR pension rate is largely gone for new applicants.

- Pension income is generally taxed at 12.5%–48% progressive rates.

- Portugal remains strong for lifestyle, but no longer a pure pension tax haven.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions.

The information in this article is not tax advice and may have changed since the time of writing. I can connect you with expert tax support for your specific situation.

Is Portugal a high tax country?

Portugal has moderate to high tax compared to some retirement havens, but not extreme by Western European standards.

- Personal income tax rates are progressive, ranging roughly from 12.5% to 48%

- Additional solidarity surcharges may apply to very high incomes

- VAT (IVA) is generally 23%

- Property taxes (IMI) are relatively modest compared to many EU countries

For retirees with modest pensions, Portugal is not necessarily high-tax.

For those with large private pensions or investment income, it can become less competitive without special regimes.

What taxes will I pay as a retiree in Portugal?

Retirees in Portugal are subject to personal income tax (IRS) on pensions and other income sources. As a tax resident, you are taxed on worldwide income.

Common retirement taxes in Portugal include:

1. Personal Income Tax (IRS)

Portugal’s IRS applies to pensions, rental income, dividends, interest, and capital gains.

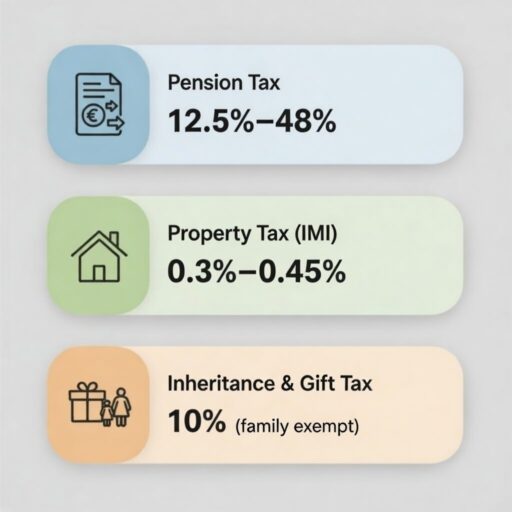

- General income (including state and private pensions) is taxed at progressive rates from 12.5% to 48%, with a possible solidarity surcharge of up to 5% for higher incomes.

- Dividends and interest are generally taxed at 28%.

- Most capital gains are taxed at 28%, though real estate gains for residents are partially included and taxed at progressive rates.

2. Pension Taxation

Foreign pensions are taxable in Portugal if you are resident. Double tax treaties may prevent double taxation, but the income is generally still reportable.

3. Property Tax (IMI)

Annual municipal property tax (IMI) typically ranges from 0.3% to 0.45% of the property’s taxable value.

4. Stamp Duty

Stamp duty of 10% may apply to certain gifts and inheritances, although transfers to spouses and direct heirs are largely exempt.

What has replaced NHR in Portugal?

The NHR regime, which allowed retirees to pay a 10% flat tax on foreign pensions, was phased out in 2024 and replaced by the Tax Incentive for Scientific Research and Innovation (IFICI), also called NHR 2.0.

Impact on retirees:

- Foreign pensions are no longer eligible for the 10% flat tax.

- Pension income is taxed under standard progressive rates, potentially increasing the overall tax burden.

- Portugal is less attractive as a low-tax retirement destination for new retirees.

Key difference:

- The new regime targets highly qualified professionals and innovation sectors, not retirees.

This change means retirees must factor standard taxation into their financial planning when moving to Portugal.

What are the benefits of retiring in Portugal?

The benefits of retiring in Portugal include good healthcare access, a pleasant climate, a relatively affordable lifestyle, and strong safety rankings.

- Mild Climate

Much of Portugal enjoys more than 300 days of sunshine per year, especially in the Algarve and southern regions, which many retirees find appealing for year‑round outdoor living. - Affordable Healthcare

Portugal’s public health system (SNS) is subsidized for residents, and private healthcare costs are lower than in many Western European countries. Consumer healthcare costs in Portugal are relatively low, with public visits costing €5–€15 and private insurance premiums typically ranging from €40–€100 per month per adult, making healthcare more affordable than in many Western European countries while still providing broad coverage. - Safety

Portugal consistently ranks near the top of international safety and peace indices. For example, it typically places in the top 10 of the Global Peace Index, reflecting low violent crime rates and political stability — factors many retirees value when choosing a long‑term destination. - Lower Cost of Living

Overall living costs in Portugal remain lower than in much of Western Europe. Independent cost comparisons show that daily expenses (food, utilities, transport) are often 10–30% lower than in countries like France, Germany, or the Netherlands. A modest retired couple can often live comfortably on €1,400–€2,000 per month, depending on lifestyle and location. - EU Residency and Mobility

Portuguese residency permits access to the Schengen zone and long‑term EU mobility, which can be valuable for retirees who travel frequently or may spend parts of the year in other European countries.

What are the downsides of retiring in Portugal?

The main downside of retiring in Portugal is higher taxes compared to the past.

Other considerations include:

- Rising Property Prices

Property prices in Lisbon, Porto, and the Algarve have risen sharply in recent years. This can make buying a home expensive for retirees, especially in popular coastal areas. - Bureaucracy

Administrative processes, including residency registration, tax filings, and healthcare enrollment, can be slow and complex. Many retirees require professional assistance to navigate these procedures efficiently. - Rental Market Pressure

Demand for rental properties in major cities and tourist regions often exceeds supply. This can lead to higher rents and limited options, particularly for those seeking long-term leases. - Investment and Capital Gains Taxation

Capital gains and investment income are taxed at standard rates, which may be higher than in some other retirement destinations. Retirees relying on investment income may face a larger overall tax burden as a result.

Which country is most tax-friendly for retirees?

Greece offers one of the lowest structured tax rates for retirees, with foreign pensions taxed at a flat 7% for up to 15 years for qualifying new residents.

Other top tax-friendly retirement destinations include:

- Italy – Certain regions impose a 7% flat tax on foreign pensions for new residents.

- Cyprus – Foreign pensions above a low exemption threshold are taxed at 5%, or residents can choose progressive rates.

- Malta – Uses a remittance-based system, taxing foreign pensions sent to Malta at a flat 15%.

- Panama – Employs a territorial tax system, meaning foreign pensions received from abroad are generally not taxed. Personal income tax rates of up to 25% apply only to Panama-sourced income, not to foreign retirement income.

- Costa Rica – Taxes only Costa Rican-sourced income. Foreign pensions are generally exempt, while local income is taxed progressively up to 25%.

- Thailand – Applies territorial-style rules, but foreign income (including pensions) brought into Thailand may be taxable if remitted, with progressive rates up to 35%.

Are there increasing or decreasing numbers of retirees in Portugal?

Portugal continues to see an increase in overall foreign residents, including retirees, even though some retirees reconsider their location due to cost and tax changes.

Official data for 2024 showed about 1.54 million foreign nationals living in Portugal, a record high, and retiree segments especially from the US, UK, Germany, and France, have grown significantly in recent years.

Examples include a reported 239% increase in American retirees living in Portugal from 2017 to 2022.

At the same time, anecdotal reports suggest a smaller group of retirees are relocating from high‑cost areas like Lisbon and the Algarve to inland towns or alternative countries with flat‑tax pension regimes.

Overall, however, the net trend points to growth in the retiree population rather than a decline.

Conclusion

Portugal today rewards retirees who prioritize stability, infrastructure, and European access over aggressive tax structuring.

It is no longer a jurisdiction chosen primarily for pension efficiency; it is chosen for predictability and quality of life within the EU framework.

For some retirees, that trade-off is entirely rational. For others, especially those optimizing large private pensions or investment income, comparative analysis across jurisdictions is essential before relocating.

The key is not whether Portugal is high or low tax; it is whether its overall value proposition fits your income profile and long-term plans.

FAQs

Is healthcare free in Portugal for retirees?

Public healthcare is not entirely free, but heavily subsidized. Legal residents can access the national health system (SNS) for low fees.

Many retirees also maintain private insurance due to shorter wait times.

Why are expats leaving Portugal?

Some expats are leaving because rising housing costs, increasing everyday living expenses, and frustrations with bureaucracy have made life less comfortable than expected.

Others cite changes to tax incentives and the search for better value, healthcare access, or lifestyle conditions elsewhere.

How long can I stay in Portugal without becoming a tax resident?

You generally become a Portuguese tax resident if you spend 183 days or more in the country within a 12-month period or maintain a habitual residence there.

Short visits under 183 days without establishing a home usually do not trigger tax residency.

Is Portugal cheaper than France?

Yes, Portugal is generally more affordable than France, with lower property prices outside major cities and cheaper dining and services.

Utilities and fuel are similar or slightly higher, and Lisbon or the Algarve can approach the cost levels of the French Riviera.

Are medical expenses tax deductible in Portugal?

Yes, certain medical and healthcare expenses can be claimed as a tax credit of 15% of the amount spent.

Eligible costs include doctor visits, hospital stays, prescriptions, and health insurance premiums, but the total deduction is capped based on income and must be properly documented with receipts.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.