Expats generally need IPMI if they expect to live, work, or travel across multiple countries, while local health insurance is usually enough for those settling long-term in a single country.

The right choice is based primarily on your international mobility, where you want to receive treatment, and how much flexibility you need if your circumstances change.

This article covers:

- What is IPMI in healthcare?

- What is local health insurance?

- What is the difference between IPMI and local health insurance?

- When should you choose local insurance?

- When should you choose IPMI?

Key Takeaways:

- IPMI is generally best for internationally mobile expats because it provides portable coverage across multiple countries.

- Local health insurance is usually the more affordable option for expats planning to remain in one country.

- IPMI typically offers broader benefits, including international treatment and medical evacuation.

- The best choice is based on your expected mobility, healthcare needs, and long-term plans, not simply the premium.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions.

The information in this article is for general guidance only. It does not constitute financial, legal, or tax advice, and is not a recommendation or solicitation to invest. Some facts may have changed since the time of writing.

Expats can compare international health insurance plans through insurance.adamfayed.com to find coverage that best matches their healthcare needs, destination, and budget.

What is IPMI health insurance?

International Private Medical Insurance (IPMI), commonly known as international health insurance, is a private health insurance policy designed for people living, working, or travelling outside their home country.

Most IPMI (international health insurance) policies offer:

- Worldwide or regional medical coverage

- Inpatient and outpatient treatment

- Specialist consultations

- Hospitalization and surgery

- Cancer treatment

- Emergency medical evacuation

- Optional maternity benefits

- Mental health coverage

- Access to large international hospital networks

Many insurers also allow policyholders to choose whether to include coverage in the United States, where healthcare costs are significantly higher.

Excluding US coverage often reduces premiums considerably.

Another key advantage is portability.

IPMI is commonly used by:

- Long-term expatriates

- International executives

- Digital nomads

- Business owners

- International retirees

- Globally mobile families

What does local health insurance mean?

Local health insurance is private medical insurance designed specifically for residents of a particular country.

Coverage generally applies only within that country's healthcare system and provider network.

For example, someone living in Thailand may purchase a Thai private health insurance policy, while a resident of the United Arab Emirates would typically buy a UAE-based health insurance plan.

Local health insurance commonly includes:

- Hospital treatment

- Day surgery

- Outpatient consultations

- Diagnostic tests

- Prescription medication

- Specialist care within the country

Some policies may include limited emergency treatment abroad, but they generally do not provide comprehensive international coverage or long-term protection outside the country where the policy was issued.

They may also be designed to complement a country's public healthcare system where available.

For expatriates who intend to settle permanently in one country and rarely travel internationally, local health insurance may provide sufficient protection at a lower cost than IPMI.

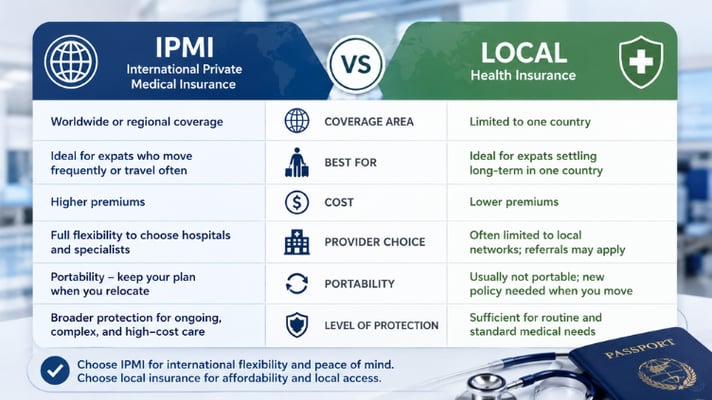

What is the difference between local health insurance and international health insurance?

The main difference between local health insurance and international health insurance is where you can receive treatment.

Local health insurance is primarily intended for healthcare within one country, while International Private Medical Insurance (IPMI) is designed to provide ongoing medical coverage across multiple countries.

Other important differences include portability, benefit limits, access to international hospital networks, and emergency medical evacuation.

Some of the key distinctions include:

| Feature | Local Health Insurance | International Health Insurance (IPMI) |

|---|---|---|

| Coverage area | Usually one country | Multiple countries or worldwide |

| Portability | Limited | High |

| Hospital networks | Domestic | International |

| Medical evacuation | Often limited or excluded | Frequently included |

| Policy continuity after relocation | May require a new policy | Often remains valid after moving |

| Annual benefit limits | Usually lower | Often higher |

| Premiums | Lower | Higher |

| Best suited for | Permanent residents | Internationally mobile expats |

Local insurance prioritizes affordability for residents, whereas IPMI prioritizes flexibility for people whose lives span multiple countries.

Which is cheaper?

Local health insurance is almost always cheaper than IPMI.

Because local insurers only cover treatment within one country, they face more predictable healthcare costs and can charge lower premiums.

Several factors influence the price difference, including:

- Country of residence

- Age

- Medical history

- Level of benefits

- Deductibles

- Coverage region

- Whether US coverage is included

While local insurance generally has lower premiums, it may become more expensive in the long run if you relocate and need to purchase a new policy or undergo fresh medical underwriting.

Which offers better coverage?

IPMI generally offers broader and more comprehensive coverage than local health insurance.

Many international policies provide higher annual benefit limits, wider access to specialists, international second opinions, emergency medical evacuation, and treatment at leading hospitals around the world.

Some plans also include preventive care, wellness benefits, mental health services, and optional dental or vision coverage.

Local health insurance can still provide excellent protection, particularly in countries with well-developed private healthcare systems.

However, benefit limits may be lower, and treatment is usually restricted to providers within the country.

If access to international medical facilities and continuity across borders is important, IPMI usually provides greater protection.

If your healthcare needs are expected to remain within one country, local insurance may be entirely adequate.

Which is better if you move between countries?

IPMI is generally the better choice if you expect to move between countries.

Many expatriates relocate every few years because of employment, business opportunities, or lifestyle changes.

Purchasing a new local insurance policy after each move can involve new waiting periods, exclusions for pre-existing conditions, and repeated underwriting.

This continuity can be particularly valuable for:

- International executives

- Diplomats

- Offshore workers

- Digital nomads

- Global entrepreneurs

- Families relocating for work

For expats whose careers involve international mobility, portability is often one of the strongest reasons to choose IPMI.

Which is better for long-term expats?

IPMI is generally better for long-term expats who expect to relocate between countries, while local health insurance is often sufficient for those planning to remain in the same country for many years.

The answer is based on what long-term means in your situation.

If you intend to build your life in one country, local health insurance may provide adequate protection at a lower cost, particularly where the private healthcare system is well developed.

However, if your long-term plans remain uncertain, or you expect to relocate again, IPMI generally offers greater flexibility by allowing you to keep the same policy instead of replacing your insurance after each move.

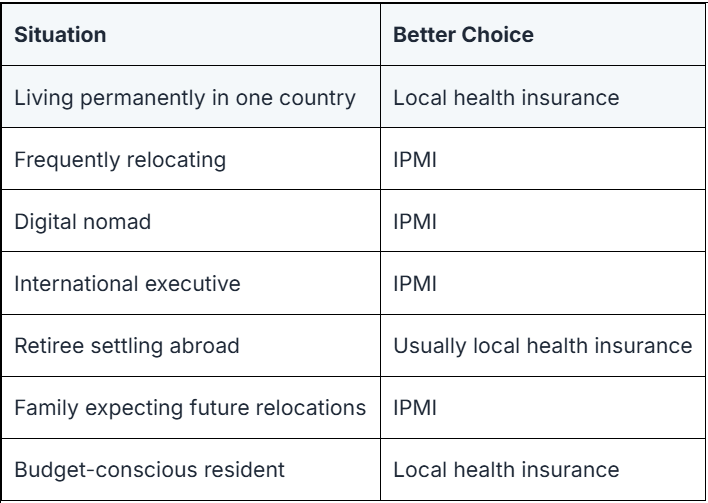

Do you need IPMI or Local Health Insurance?

If you expect to build your life around one country, local health insurance is often the more practical and cost-effective solution.

If international mobility is part of your career or long-term plans, IPMI usually provides better long-term value despite its higher cost.

The following guide can help:

Conclusion

Neither IPMI nor local health insurance is inherently better; each is designed for a different type of expatriate.

Rather than choosing the policy with the lowest premium or the broadest list of benefits, consider where you are most likely to receive medical care over the next several years and how easily your plans could change.

Buying insurance that matches your expected lifestyle can help avoid unnecessary costs, coverage gaps, and the need to replace your policy after relocating.

As your circumstances evolve, reviewing your health insurance regularly can help ensure your coverage continues to meet both your medical needs and your long-term plans.

FAQs

What are the 4 types of insurance coverage?

In the context of health insurance, the four common types are public or national health insurance, local private health insurance, International Private Medical Insurance (IPMI), and travel medical insurance.

Each serves a different purpose, with IPMI generally providing the broadest long-term coverage for expatriates living or travelling internationally.

What is the difference between HMO and traditional health insurance?

An HMO generally limits you to a network of healthcare providers and often requires referrals to see specialists, while traditional health insurance offers greater flexibility to choose doctors and specialists without referrals, usually at a higher cost.

Does private health insurance cover diabetes?

Yes, private health insurance can cover diabetes, but coverage is based on whether the condition existed before the policy began.

Pre-existing diabetes may be excluded, subject to waiting periods, additional premiums, or special underwriting, while diabetes diagnosed after coverage starts is often covered according to the policy terms.

Is psoriasis covered under health insurance?

Yes, many health insurance policies cover the diagnosis and treatment of psoriasis, although the level of cover depends on the policy and whether the condition is pre-existing.

Some insurers may impose exclusions, waiting periods, or underwriting conditions for existing psoriasis, and cover for advanced treatments such as biologic therapies may be subject to policy limits or pre-authorization.

Related Articles:

- International Health Insurance for Expats in Panama: Coverage, Costs & Providers

- International Health Insurance for Remote Workers Guide

- Health Insurance for Expats in Qatar

- Overview of Health Insurance Cost in the US

- Health Insurance for Retired Expats: Best 8 Options for Expats Over 60

- Does Your Employer Health Insurance Actually Cover You Abroad?

- What to Do When Your Cigna Global Premium Increases