I often write on Quora.com, where I am the most viewed writer on financial matters, with over 652.2 million views in recent years.

In the answers below I focused on the following topics and issues:

- What would be good investments when interest rates start to rise?

- People say all “get-rich-quick” opportunities are all scams, but realistically, who wants to “get-rich-slow”? Aren’t we already doing that just by working full time for 40 hours a week for someone else?

- How do entrepreneurs use leverage?

- Is the BRICS dead?

- What has been the highest interest rate in the UK?

- Networking doesn’t work for everybody, does it?

- Can I hold and manage my stocks in US after leaving the country permanently? What are the tax implications?

- What is a good investment if China invades Taiwan?

- What do you do if your country is about to experience hyperinflation?

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Some of the links and videos referred to might only be available on the original answer.

What would be good investments when interest rates start to rise?

Firstly, avoid the trap!

What do I mean by the trap?

The trap focuses only on yield.

Apple just became the first company to reach three trillion in market cap. Amazon is almost as big. Both pay little to no dividends.

Neither does Warren Buffett’s, Berkshire Hathaway. All three have been some of the best-performing assets over the last hundred years.

Likewise, the UK’s FTSE 100 and the Australian stock market have high dividends due to the number of energy and banking stocks.

Both haven’t performed as well as the US stock markets, the Dow Jones, S&P500 and Nasdaq, despite the latter paying fewer dividends.

Likewise, interest rates have risen and fallen by over a hundred years, but two things never change:

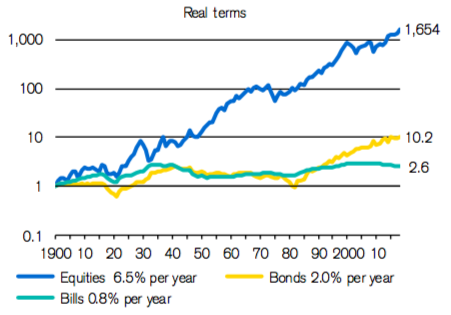

- Cash in the bank doesn’t beat assets long-term. This image from seeking alpha shows the long-term returns, adjusted for inflation, of stocks, bonds and T-bills, which are cash-like:

- There are currency crisis and inflation globally so cash isn’t less risky.

Here is Bridgewater billionaire Ray Dalio speaking about cash. He has regularly said that cash is one of the riskiest assets due to the inflation risk:

Holding cash short-term or for emergencies makes sense.

Investing a year and then selling out to buy a home or pay for a wedding makes no sense.

Yet cash isn’t a long-term solution, and it certainly isn’t safer just because you are getting a fixed return.

So what are the alternatives?

The main ones are:

- Money market accounts. Not a great alternative as this is “cash-like”. They often pay slightly above bank rates. The advantage is they can be held in a broader portfolio together with bonds and stocks

- A-rated corporate bonds.

- Government bonds. Interest rates will fall. When they do, bonds should increase. You do still have the inflation risk-adjusted with bonds, though.

- More sophisticated investments, such as insured fixed-return investments. You often need an advisor to do this though

- Just stick to a long-term plan, knowing that assets like stocks will almost for sure beat cash long-term.

How do entrepreneurs use leverage?

This lady says it best:

You have at least four kinds of leverage:

- Labour leverage

You have 24 hours a day.

You cannot, therefore, work 25 hours a day.

You can buy hundreds of even thousands of hours of other people’s time though.

Historically, this was the biggest form of leverage. You couldn’t create a big firm with few people historically.

2. Capital

If you have capital, you can get capital from the banks, in the form of mortgages, or other individuals, who are more likely to trust those with more resources.

Even if you don’t have loads of capital, you can invest into other firms via stocks and shares, and take advantage of their ability to use capital leverage.

3. Code

With the second kind of leverage, the banks were often the biggest players.

JP Morgan, and others like him, were some of the richest people over a hundred years ago.

When the internet came out, suddenly having access to code could become a form of leverage.

4. Audience and technology

Attention and audience equals monetization opportunities.

If somebody has 100,000 followers, and each of those 100,000 followers has an average of 100 followers, they have access to a potential audience of 10,000,000 every post, or more if it goes viral.

Good paid adverts online are also scalable in a way that traditional means aren’t. For example, if a real estate company makes $20,000 from every $10,000 spent online, they can just increase the amount spent on adverts.

Online networking is also much easier than in-person networking, as you can’t meet millions in person.

Basically, working hard is important, but we can’t get big alone.

Is the BRICS dead?

It is an excellent question because we have recently heard a lot about the BRICS.

Anybody over 32–33 has heard many stories about the BRICS during their lifetime.

It started in the 2000s when the former Goldman Sachs economist Jim O’Neill coined the phrase BRIC for Brazil, Russia, India and China.

After 2008, the worldwide narrative was “wealth is going to the east and south”; therefore, people became bullish about emerging markets.

BRICS became BRICS to include South Africa. We know what has happened since.

South Africa, Brazil and Russia have disappointed in terms of growth. India hasn’t. China didn’t in the early years after 2008 but is now growing more slowly than expected.

The new narrative about BRICS is that they might not grow as fast as expected but will grow as a currency and political block.

In other words, they will grow in terms of political power and will even be able to challenge the USD.

Nobody can predict the future, but it is mostly hype regarding currencies.

Especially laughable is the idea that they will create a currency tied to gold that will challenge the USD.

The idea of returning to the gold standard via the BRICS is laughable.

People should be more careful about investing and losing money due to the hype.

China’s stock market has been one of the worst performers in the world since 2006. All of them have done worse than the US and other developed market stock markets.

That doesn’t mean this will always be the case. The stock market isn’t the economy, and vice versa.

As we have seen recently and historically, stock markets can grow or fall during recessions, pandemics, wars and much else.

Yet it is a mistake to think that the economic potential in some emerging markets means they will outperform in terms of investment opportunities.

People say all “get-rich-quick” opportunities are all scams, but realistically, who wants to “get-rich-slow”? Aren’t we already doing that just by working full time for 40 hours a week for someone else?

Getting rich easily is almost always a scam.

People do get rich quickly, but that doesn’t mean it is easy.

Often, it is due to a combination of:

- Luck/chance/randomness. Right place/right time etc

- Hard work

- Smart work

- Natural talent combined with randomness, hard and smart work.

- Risk-taking.

- Previous work over many years as per the quote below from AZ quotes:

In terms of your comment “Who wants to get rich slow”, that is the issue.

That is why there are so many scams because scammers recognize that many people want to get rich without making that many sacrifices.

That is also why most people who do get rich quickly, from pure luck (inheritance, winning the lottery etc), tend to either lose it or barely hang onto it.

Patience and persistence often pay off because few people want to do it.

For example, people who invest for decades whilst working for somebody else might not get rich, but they will most likely become wealthy.

People who want to get very wealthy and rich do often need to take bigger risks.

That doesn’t mean those risks always pay off quickly or at all.

In reality, few people want to take the risk to work really hard and/or take loads of risk and then make less than minimum wage, which is why so few people become entrepreneurs.

Best to just pick what you want. If you want to get wealthy slowly with very limited risk, then investing for decades works.

If you want the chance to do much better, you need to accept much higher risk in return for the chance for more aggressive growth.

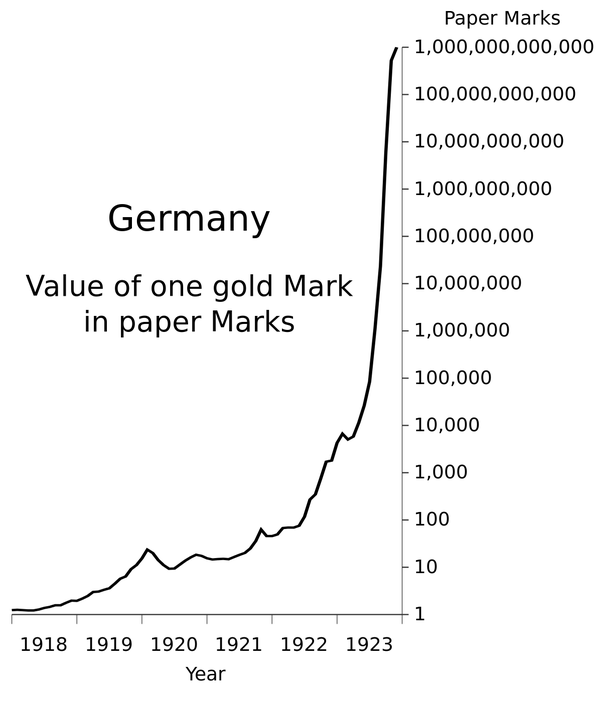

What do you do if your country is about to experience hyperinflation?

Firstly, most people don’t know in advance that inflation will go super high.

Most wealthy people in Germany in the 1920s or Zimbabwe or Venezuela more recently didn’t expect it.

So, it is always better to assume that unlikely risks like this could happen in any country.

Argentina and many countries in Latin America were wealthy in 1945 and the 1950s.

In fact, many of them were inside the top twenty countries globally by GDP per capita, with Venezuela being ranked number three or four.

So, to answer your question, it is best to:

- Have international diversification.

Assets like real estate are better than cash during very high inflation, but they still aren’t great.

One of my friends bought an apartment in Caracas in 2000 for about $120,000. It is now worth about $20,000. So, adjusted for inflation, it has fallen by 90% or more.

Better than cash but not great.

International diversification means holding assets like stocks, real estate or bonds in foreign countries and across numerous markets.

The same for a business owner. It is always best to have clients and entities in different countries.

Don’t put all your eggs in one basket.

2. Hold second passports and residencies

If you are living in an unstable country, it makes sense to have second residencies and even passports.

Remember, when a country becomes more unstable, more countries put restrictions on entering other countries.

In the 1980s, it was far easier for Lebanese and Venezuelans to travel and get second residencies.

Considering some second residencies can be obtained relatively cheaply, it makes sense to diversify if you can.

What is an equally big risk is persistently losing out to inflation. From 2008 until now, the banks have paid 2%-3% below the rate of inflation and most currencies have lost value to the USD.

I was speaking to a friend who is an expat who recently admitted to keeping money in the UK for over fifteen years, and quote, “losing about 70% to a combination of inflation and currency devaluations”.

100,000 GBP in 2007 was worth $200,000. Now it is worth $127,000. Even with some interest obtained, it would now be worth about $140,000-$150,000.

$150,000 now is worth less than half what $200,000 was worth in 2007.

That is why persistent inflation which isn’t beaten is called the silent killer of wealth, as it happens slowly but then compounds over time.

Networking doesn’t work for everybody, does it?

It doesn’t.

What is less often said is that it doesn’t work for most people compared to the alternatives.

Consider this analogy.

Imagine you went finishing with a small rod.

Would you catch some fish? Sure.

Would you occasionally catch some big fish, even if you struggle to control the rod?

You probably would if you were persistent enough.

Yet would you catch as many fish as if you had a huge net?

Obviously not, and you certainly wouldn’t catch as many whales or sharks.

If you go to a networking event every week, you will meet a few people and spend maybe a hundred or more hours of time on this.

At the same time, organic traction from social media and paid ads will get you in front of millions.

Networking, even when it is useful, isn’t scalable like online.

It only works well if you hire hundreds or thousands of minions or you get lucky.

Better to only network in areas which are your hobbies. For example, playing golf if you like it.

Think about it another way. Who would you rather invest in?

A small, profitable, business that does well in the local community, who happens to get clients from referrals or networking events?

Or a small, profitable and fast-growing firm that can (and does) get clients globally due to online, scalable, reach?

The answer is obvious. It is the world versus your local village.

What is a good investment if China invades Taiwan?

Firstly, let’s hope that new wars don’t happen. Not just in East Asia but globally.

However, to answer your question, it depends on how bad things were.

If it was a minor conflict, like China trying to take a small island belonging to Taiwan, then semiconductor firms that are based outside of the region would do well.

However, if it was bigger, then it could be bad for everybody.

Either way, this is speculation.

What isn’t speculation is:

- Many wealthier Chinese and Taiwanese are preparing for tougher times.

I read this on the FT.

“Lynn, a Taiwanese stock trader, has never been to Europe. But, in February, she spent a large part of her savings on a €420,000 flat in Lisbon — without even seeing the property. Everything was handled through a Portuguese agent, who also submitted the paperwork for a golden visa for her family.

“We had to get the application in before Portugal ended the programme,” explains Lynn, who asked to be identified only by her first name. “It is prudent to put some of our money outside Taiwan and to have a place where we can go, just in case.”

The “just in case” scenario the young banker is referring to is war. As China ratchets up its military intimidation campaign against Taiwan, and foreign governments grow concerned Beijing might attack the island it claims as its own, some Taiwanese are quietly exploring options to protect their wealth and prepare a way out. “People are nervous,” says C Y Huang, a veteran Taiwanese investment banker and financial adviser.

Pointing to US investor Warren Buffett’s move to sell his stake in Taiwanese chipmaker TSMC due to geopolitical concerns, he adds: “Even these rich Americans think that Taiwan is dangerous. People here feel that doesn’t mean there will be war, but you don’t make jokes with your own money.”

In addition to that, I noticed something else happening in China, especially from 2012–2013.

I worked in China in 2013 and noticed that whilst most ordinary Chinese were still optimistic about the future, more and more wealthier people were hedging their bets.

They were worried about the general economic and political trends. Even back then, about half of them wanted to emigrate, with many of the remaining half wanting to get more money out of China and get another citizenship.

That has contributed to increasing real estate values in places like New Zealand, Australia and Canada.

More recently, prices in Singapore have skyrocketed due to many wealthy Chinese moving, and getting money out of the country has become more difficult as per the article below.

One reason is that as more people are becoming nervous, there have been increased restrictions placed on sending money out.

2. Wealthier people diversity

At least if they are sensible.

In fact, wealthier and middle-class people diversity if they are sensible.

There are many formerly wealthy people living in places like Zimbabwe and Venezuela now.

For that matter, there are many in China. This woman, Whitney Duan, used to be the wealthiest lady in China.

As per the image above from the Daily Mail, her ex-husband spoke out, via his book Red Roulette, when he explained how politics and business get connected in China.

The point is, nobody knows the future for sure. I am sure Jack Ma also didn’t expect to climb down a few years ago.

Getting second residencies and passports and having assets in countries around the world is much safer than having it all in one country.

Whitney Duan’s ex-husband urged her to diversify overseas and she didn’t listen. She must now be regretting that.

This point is something which goes beyond East Asia.

I am sure Ukrainians who got second residencies and passports + put assets overseas before the conflict don’t regret that now.

It is just like buying an insurance policy, but you also get capital gains and advantages from putting some of your eggs overseas.

Can I hold and manage my stocks in US after leaving the country permanently? What are the tax implications?

This isn’t tax advice, but in general, you should look to remove all US ties if you leave.

That is if we look at this from a purely financial and hassles point of view.

That includes:

- Renouncing the passport like thousands are doing every year

- Getting rid of green cards and other things which could make you a “US-specified person”.

- Anything which could mean you have to comply with FATCA and FBAR (articles on that below).

Of course, there could be certain assets that you can’t easily liquidate, but you should get rid of what you can.

It is simpler and less risky to just cut all your financial ties once you leave.

You never know when things like US estate taxes could come back to bite you, and many US-domiciled funds and ETFs have withholding taxes on dividends for non-residents.

That is why most non-US residents who are sensible buy US funds and ETFs domiciled on the London, Irish, Canadian or other stock exchanges.

You might think tax risks are small but just look at Boris Johnson:

Born in the US. Must have decent legal representation, yet he only renounced his US ties once he paid a huge unexpected tax.

Better to be safe than sorry.

What is more, moving assets isn’t usually that difficult.

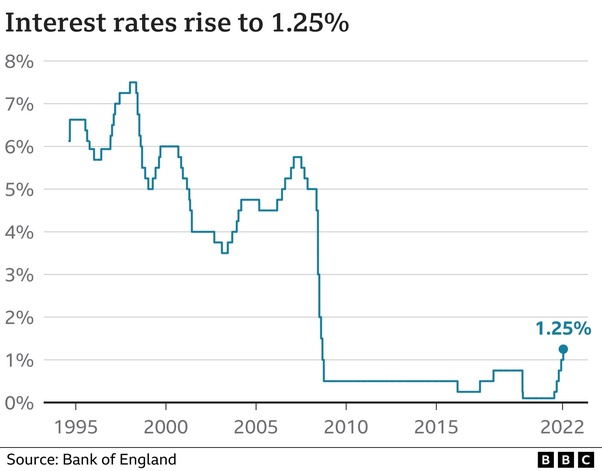

What has been the highest interest rate in the UK?

17%.

We could see interest rates briefly hit 6.5%-7% in the UK soon, before they eventually fall.

That would be the highest in quite some time as per this graphic from the BBC:

It could mean Sterling will rise, but the risks are now higher for investors than before.

We saw that last year when the Pound almost hit parity against the US Dollar.