Many expats assume Mexico is cheap and overlook tax friction and jurisdictional risk.

Mexico is affordable, yes, and an expat in Mexico can live comfortably on roughly $1,800–$3,500/month.

But tax rules, residency status, and currency exposure quietly shape your financial future. Ignore them, and your savings shrink without warning.

This article covers:

- Why is financial planning important for expats in Mexico?

- Can you open a bank account in Mexico as a foreigner?

- How much money do you need to comfortably live in Mexico?

- Is Mexico a good place to invest?

- Is Mexico tax-friendly?

Key Takeaways:

- Tax residency determines global taxation exposure for expats in Mexico.

- Peso fluctuations impact long-term savings more than local inflation.

- Banking is accessible but compliance delays can affect liquidity.

- Cost of living varies sharply across cities and expat hotspots.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions. We also offer bespoke structuring solutions tailored to your situation.

The information in this article is for general guidance only, does not constitute financial, legal, or tax advice, and may have changed since the time of writing.

What is the importance of financial planning for expats in Mexico?

Financial planning for expats in Mexico is about protecting your income from double tax traps, currency shifts, and banking delays.

Without a plan, retirees and remote workers often end up paying more in fees, fines, and informal fix‑it costs than on their actual rent.

- Poor tax residency decisions can trigger both your home country and Mexican tax filings, even if you technically live abroad.

- Weak banking and currency planning can turn a cheap lifestyle into a logistical nightmare when you cannot access funds or must convert large sums at bad rates.

- Most expats focus on headline‑city prices, not on recurring items like healthcare, internet, and transport, which can quietly inflate a low‑cost budget.

What to know before moving to Mexico as an expat?

Before relocating, you must understand Mexican visa type, currency habits, residency rules, and banking reality. Not just rental prices.

Mexico uses peso‑denominated contracts, and your tax life depends on whether Mexico treats you as a resident or non‑resident.

- Legal status

Temporary Resident (visitante residente): For most remote workers and retirees, lets you stay up to four years and renew for longer.

Permanent Resident: For those who have lived in Mexico several years and meet income/savings thresholds.

- Currency

Salaries, rent, and taxes are quoted in MXN, yet many expats receive USD or EUR; hedging fx risk is essential.

- Residency and risks

Tax residency depends on where you dwell and spend more than 183 days; missteps can trigger Mexican filings even if you think you’re a non-resident.

Digital‑nomad‑style hopping in and out can create gray‑zone liabilities on both sides if you do not coordinate with your home country tax authority.

Can a foreigner open a bank account in Mexico?

Yes, foreigners can set up a bank account in Mexico but only if they have a valid Mexican residency‑type visa or resident‑type status.

Since 2024, most traditional banks have rejected tourists and short-stay visitors, even if they carry a passport and FMM.

- Minimum conditions

Valid passport and Mexican residency card (FM2/FM3) or comparable INM‑recognized document.

RFC tax ID from SAT (required for almost all retail bank accounts).

- Practical hurdles

You must usually visit a branch in person, sign contracts in Spanish, and provide biometric data.

English speaking support is still limited outside major tourist/expat corridors.

Which Mexican bank is best for foreigners?

There is no single best bank in Mexico for foreigners, but BBVA, Intercam, and fintech‑style Hey Banco each suit different needs.

Many expats lose money as they open accounts at national chains with high FX spreads without checking whether fintechs or credit unions offer better conversion rates.

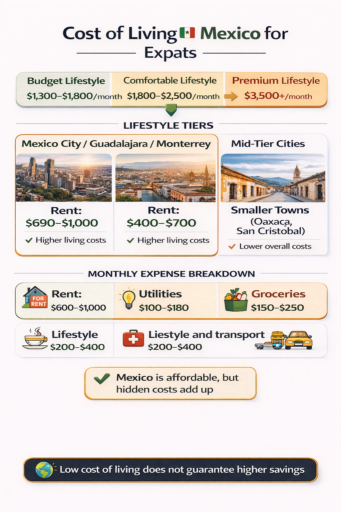

What is the cost of living in Mexico for expats?

A single expat in Mexico can live reasonably on about $1,300–$1,800 USD/month, while a couple may spend roughly $1,800–$2,500/month.

City vs rural/small‑town

Mexico City, Guadalajara, Monterrey:

- 1‑bed center: roughly $690–$1,000 USD/month

- 3‑bed family‑friendly: $2,000–$3,500 USD/month

Smaller towns (e.g., San Cristóbal, Oaxaca, lakeside areas):

- 1‑bed apartment: often $400–$700 USD/month, food and utilities similar or slightly lower.

Typical monthly expenses may include rent, utilities, groceries, transport, and private healthcare.

Prices are lower than in the US and Canada, but imported goods and certain brands cost close to or more than in North America.

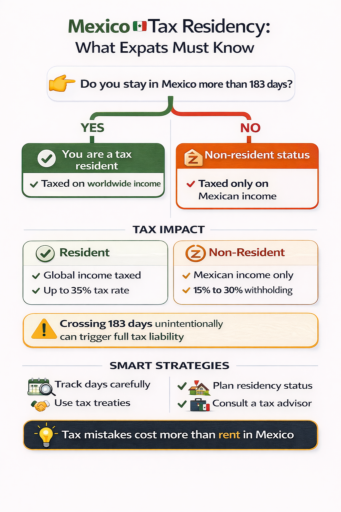

Do foreigners pay tax in Mexico?

Yes, expats pay tax in Mexico if they are Mexican tax residents or earn Mexican‑source income. Foreigners are not automatically tax‑free just because they hold a foreign passport.

- Resident vs non‑resident

Residents pay progressive income tax (ISR) on worldwide income, with a top marginal rate of 35%.

Non‑residents pay withholding taxes on Mexican‑source earnings (e.g., rental, work done in Mexico), often at 15–30%, depending on the amount.

- Double‑tax treaties and credits

Treaties (e.g., US–Mexico) let you claim foreign‑tax credits or exclusion methods to avoid double‑taxing the same income.

Here’s what most expats get wrong: assuming that living part‑time in Mexico keeps them non‑resident, while actually crossing the 183‑day or domicile tests and triggering Mexican filings.

What are the taxes in Mexico for expats?

Mexican taxes for expats revolve around income tax (ISR), VAT (IVA), and foreign‑source‑income rules, all run by SAT (Servicio de Administración Tributaria).

- Income Tax (ISR)

Residents: Progressive brackets, exempt up to about MXN 125,900/year, then 15% up to MXN 1,000,000, then 30% above that. The top marginal rate is still 35%.

Non‑residents: wage‑type income in Mexico is taxed at 15–30%, depending on the level.

- VAT (IVA)

Standard 16% on most goods and services; some basic food and medicine are 0%.

- Global‑income rules and reporting

Residents must declare worldwide income and may have to file annually using the SAT Forma 22.

Using SAT’s online portal (sat.gob.mx) is now the norm for most filers.

Tax friction compounds faster than inflation for expats.

Small compliance lapses, missed filings, or wrong residency assumptions can drag you into audits and penalties even if your headline income looks modest.

Is investing in Mexico a good idea?

Investing in Mexico can make sense for diversification and income, but it comes with currency, political, and regulatory risk that many expats underestimate.

Opportunities

- Real estate in certain Mexican cities has outperformed inflation over the last decade, especially mid‑range and rental‑friendly units.

- Local equity and bond markets offer higher yields than some developed markets, though with more volatility.

Risks

- Peso swings can erase gains in dollar‑terms.

- Mexico’s tax and banking rules change frequently; recent years have tightened compliance, enforcement, and reporting.

For most expats, a modest peso‑hedged position plus an overseas core portfolio is safer than going all‑in on Mexican assets.

Can you buy a property in Mexico as an expat?

Yes, expats can buy real estate in Mexico but with restrictions on restricted zones near the coast and borders. Foreign ownership is usually done through a bank trust (fideicomiso) or via a Mexican corporation.

- Restricted zones

Within 50 km of the coast and 100 km of the borders, foreigners cannot hold direct title; instead, they place property into a fideicomiso administered by a Mexican bank.

- Non‑restricted areas

Outside those zones, foreigners can own property directly via title, similar to Mexican citizens.

- Practical tips

Always run titles and contracts past a Mexican real‑estate lawyer, not only a real‑estate agent.

Understand annual property tax (predial) and maintenance fees, which can be low in absolute terms but still meaningful in a small budget retirement.

Is Mexico a good place to retire as an expat?

Mexico can be a good place to retire as an expat due to its lower cost of living, warm climate, and good healthcare options, yet retirees must plan for currency shifts, bureaucracy, and safety differences by state.

Pros

- Reasonable rent and daily cost structure, especially outside major metros.

- Strong pension type options for those who qualify for certain tax resident programs (e.g., retirees with offshore funds can sometimes benefit from a 15% flat rate regime, if conditions are met).

Cons

- Visa and banking rules are not set‑and‑forget; changes in INM or SAT rules can affect access and compliance.

- Safety and infrastructure vary widely. Some expat‑heavy states are well‑serviced, others are not.

Mexico is best for retirees who are adaptable, somewhat bilingual, and comfortable navigating local institutions rather than expecting a fully North‑American administrative experience.

How much money do you need to retire to Mexico as an expat?

Most comfortable expat retirees manage on about $1,400–$2,500 USD per month.

- Modest lifestyle: $1,400–$1,800/month

- Mid-range lifestyle: $2,000–$2,800/month

- Higher-end lifestyle: $3,500–$5,000/month

A stable internationally linked income source, such as pensions or investment income, may matter as much as monthly spending estimates.

FAQs

How much monthly income do I need to move to Mexico?

Most expats need at least $1,300–$1,800 USD/month for a single person, more in Mexico City or if you want private healthcare and a car.

Is $1,000 a month enough to live in Mexico?

$1,000/month is possible in very low‑cost towns if you live frugally, but it leaves little room for healthcare, travel, or emergencies.

Is it better to rent or buy in Mexico?

Renting is usually safer for new expats or non‑long‑term residents, while buying makes sense only if you plan to stay 5+ years and understand local titles and taxes.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.