In this blog I will list some of my top Quora answers for the last few days.

Those questions have included being asked about the Ant IPO, why people shouldn’t keep a lot of money in the bank and covid vaccines.

These questions included readers asking me about global poverty, the best investing books and why (some) poor people blame “the rich” for their problems.

If you want me to answer any questions on Quora or YouTube, don’t hesitate to contact me.

Should I just save my money in a bank savings account or invest it in stocks, mutual funds, etc.?

Source: Quora

It is naturally for people to assume that “doing something” is riskier than “doing nothing”.

This isn’t always the case. Sometimes “doing nothing” can be riskier in investing, business, politics and life.

I was reading a book this morning about political leadership. The author made the point that the former UK Prime Minister Gordon Brown never recovered from one event.

He was considering calling a snap election in 2009. His polls were high.

Not everybody liked him but the public considered him very decisive given his response to the Global Financial Crisis of 2008–2009.

The fact that his polls were up gave him added confidence. Word leaked about a plan for a snap election.

The opposition leader told him to “bring on” the election. He decided against it even though they weren’t prepared and are said to have admitted that in private.

He was seen to have bottled the election and he never recovered.

People made fun of him for his lack of decisiveness with pranks like this……

The same is true in business. Kodak thought the status quo would last forever.

They were at the top of their game. I met somebody who knew some of their executives in Tokyo who were spending $10,000 a month on rent in the 1980s!

They were confident about the future to say the least and didn’t see the need to innovate and take a “risk”

They decided not to invest in digital photography. They paid the price and went bust:

The same is true in business. I have met more people that have lost from “doing nothing” to “doing something”.

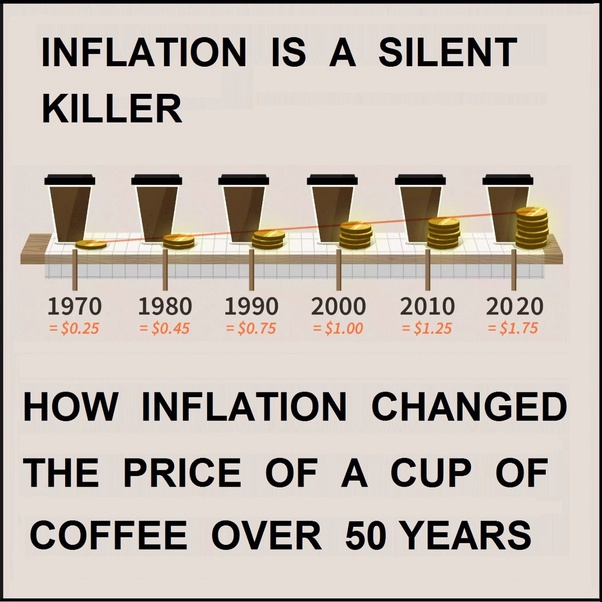

The reason is simple. Doing nothing is a silent killer. If you are getting 0% in the bank and inflation is at 2%, you have only lost 2% to inflation.

You won’t notice if your favourite coffee has gone from $5 to $5.10. Or you will, but you won’t care.

But if you use 2%-3% to inflation for 10 years+, then you are looking at a 35% loss, because inflation compounds.

Currency devaluations are even more brutal. The average South Africa, British, Nigerian and Ghanian investor has lost a lot from this in the last 12 years.

And I could have gone on with that list to include many Latin American countries.

Don’t get me wrong, we should all have some cash for emergencies.

It isn’t an investment though and it will never beat the markets long-term, unless we go through an special period that has never happened before.

Markets are just more volatile than cash. That doesn’t make it riskier if you hold on long-term.

The only reason you shouldn’t invest is if you suspect you would panic sell whenever there is a market crash.

If COVID-19 continues without the vaccines, do stock markets keep going up because people can’t spend on eating out or expensive vacation?

Source: Quora

I am no health expert. Most people who are think there will be a vaccine and it won’t be 100% effective.

Yet that will still bring the pandemic down and eventually we will ensure that covid is endemic like the flu.

In other words, it will continue maybe “forever” like the seasonable flu and loads of other diseases, but it will be manageable.

The thing is though, there is no correlations between health events and markets.

Markets have historically gone up during pandemics. They went up from 1918–1920 during World War 1 and the Spanish Flu.

They once again have done relatively well during this pandemic. Many markets are up, or are stagnant, for the year.

You also have the reality that economic growth and markets aren’t always connected.

China and many emerging markets have done well, economically speaking, in the last 15 years.

Yet the Chinese Stock Market has done very badly in that time, and emerging markets as a whole have lagged.

So, the three things are connected. There might be a vaccine and a great economic recovery and markets fall!

We might also go into a double dip recession, and get bad news about delays in vaccines, and markets might rise.

Markets aren’t predictable in the short-term. Look at the week we have just had.

Most people thought markets would fall if the US Election was uncertain, in the same way they expected a fall in markets if Trump was elected in 2016.

What happened? Markets have soared after the 2020 election just like they did in 2016.

Best to just keep investing for the long-term through all economic and health conditions.

That way you will have good and bad years, but the average returns will be fine.

As a final point I would say that most of the stock market in developed countries at least, is controlled by institutional investors like hedge funds, banks and so on.

That is just one reason why markets can increase even if unemployment is going up.

But that means the contrary is also true. If more people spend more on investing as your question asks, that will only have a marginal impact on markets.

What type of things should people be looking to invest in a post-COVID-19 world?

Source: Quora

Let’s look at the short-term vs the long-term. In the short-term, anything can happen.

That has always been the case and always will be. The only certainty is uncertainty.

Look at this year. Markets have soared during coronavirus (January/early February), crashed during it (late February/March).

They have also gone up during a second European lockdown and uncertain US election (November).

This was very unexpected for most people……although perhaps not for many people reading my answers for any length of time.

After the election was decided and there seems to be a vaccine, markets increased as most people expected.

The point is, sometimes markets behave as ‘the crowd” expects. Other times they behave in the opposite way to how people expect.

That is one reason why even most professional investors try to put money into the markets (stock and bond markets) regularly and avoid trying to time the markets.

We might well see a rebound in traditional industries in the coming months.

It is telling that many European markets are up more strongly than US stocks on news of this potential vaccine.

The UK Stock Market is very focused on financial, oil & gas and other traditional firms.

That is one reason why it is still 25%-30% below its 2018 peak, but that could well change.

Longer-term, I am unsure if the pandemic will change long-term valuations.

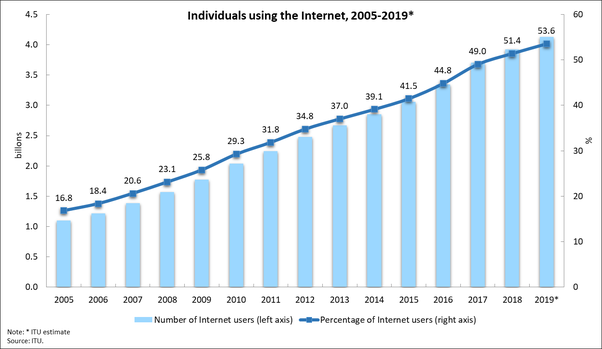

We were using technology more and more even before the lockdowns.

If you look at the percentage of people using the internet, it is one way traffic:

We were seeing an increasing number of people doing “almost everything” online even before lockdown.

I have been dealing with a recruiter since 2015 who I have never met in person.

So, this remote and online trend was going on for years before lockdown hit.

Lockdown just forced the world to press the fast forward button on existing trends.

Therefore, I expect there to be a two stage process once the pandemic is under control:

- People are relieved to be able to “go back to normal”. Face-to-face events skyrocket for a few months or even a year. People might use social media and technology a bit less.

- Once that settles down, we will go back to a 20–30 year trend of more and more tech in our lives. I would be amazed if by 2030 or 2035 we aren’t using much more tech than now and face-to-face interactions are even less than during lockdown of 2020. Some things, like travel and sporting events, can’t be done as easily remotely, so that might fully recover.

I could be wrong though. In any case, the sensible long-term investor shouldn’t focus on speculating on trends.

With proper diversification people can avoid the need to catch trends.

Also, a lot depends on your investment time horizon as well. For example, somebody who is young enough to not need to care about volatility could still make a lot investing in the Nasdaq, despite these high valuations.

If you are older, bonds still have their place in a portfolio, whereas younger investors can focus mainly on equities.

Again though, these things haven’t really changed. Low and bonds interest rates have been a feature of most developed markets like 2008, and Japan for 25 years+.

The fact that the difference between long-term stock returns relative to bonds and cash is likely to be wider than has historically been the case isn’t a new feature.

Why did China halt the Ant Group IPO?

Source: Quora

Nobody knows for sure, although Jack Ma’s speech probably didn’t help.

He criticised China’s regulators openly and accused its banks, many of which are state-owned, of having a “pawnshop mentality” that requires collateral and guarantees to extend credit to businesses.

Having spent a lot of time in China, living there for close to 5 years at one point and visiting 60+ times, I can tell you what Ma said is right.

Anybody who has done business in China in the industry would see his point.

Regardless, what the episode does show is:

- Pre-IPO companies are risky. That sounds obvious but some people forget the basics.

- Pre-IPO companies are even riskier in China and any one party state, because the party can pull the IPO for any number of reasons.

- Private business can never truly be private in a place like China. This is something Ma himself has admitted on several occasions. He commented a few years ago that it is idealistic to be apolitical as a successful private business person in China. You can’t fall out with the party and hope to have the same benefits.

- The party is even more concerned with regulating finance than some “less important” sectors of the economy.

- Regulators and rivals are pushing back against Ant’s growing dominance in the payment space. There are now more payments controlled by Ant than total cash payments in China.

- The message appears to be clear….that no “big business man” will be tolerated on the mainland unless they toe the line. This case appears to be sending a message to other big business leaders and reminds me of the Fan BingBing case which was completely different, but was still sending a clear message.

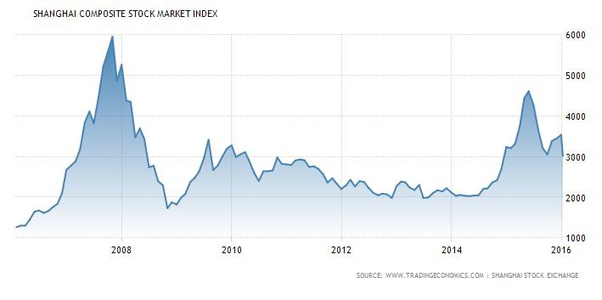

- There were some Chinese consumers who were trying to use debt to buy the stock. This reminds me of the 2015 stock market skyrocketing in China, only to collapse again, which you can see in the graph below. One of the differences between the Chinese Stock Market and the US Markets is that the everyday consumer plays a more important role. Whereas in the US 80%-90% of the money is controlled by institutions such as hedge funds and banks, the Chinese market is more dependent on the consumer. That is one reason why we can see bigger spikes up and down in the Chinese Stock Market vs most developed ones.

I suspect we haven’t heard the end of this drama and Ma will either completely fall from grace and go to prison ( as one exiled Chinese billionaire predicted Jack Ma retiring may signal conflict with Xi Jinping and Chinese govt: reports | Taiwan News) or he will find a way to get back into the parties good books.

A man who is famously persistent, and once applied to Harvard on numerous occasions, is unlikely to give up easily.

Therefore, Ant might come back with another offering which satisfies the government.

Either way, investors should be careful with any future IPOs which could be influenced by politics – – which essentially is any IPO on Chinese Markets.