Understand the pros and cons of investing in bonds and consider them as part of your alternative investment options.

I often write on Quora.com, where I am the most viewed writer on financial matters, with over 330.2 million views in recent years.

In the answers below I focused on the following topics and issues:

- Is investing in government bonds still worth it? Bonds are uncorrelated to stock markets, but no longer pay as much as they historically did. I therefore look at the positives and negatives associated with traditional portfolio construction, which emphasises the need to use bonds.

- Do US stock markets always beat international ones? This is an interesting question as it comes at a time when US stock markets have outperformed for a long period of time. Will it last?

- Tesla’s stock has been soaring in recent days. Will Elon Musk become the world’s first trillionaire?

- Why do many footballers go broke, despite earning loads of money?

Some of the links and videos displayed on the original answers might not show up on here, and if so, you will need to refer to the original answers to view that.

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Is investing in bonds worth it?

It depends what you mean by bonds, but for the purposes of this question I will assume you mean government bonds.

I have partly changed my mind on this question in recent times. Don’t get me wrong, government bonds still have the following benefits:

- They aren’t correlated with stock markets

- The short-term ones still often go up when markets fall, like in 2008–2009. Even during the Covid falls, short-term bonds did relatively OK.

- Just because bonds aren’t performing well now, doesn’t mean they won’t always perform badly. The “death of bonds” has been called many times in history. We shouldn’t judge assets purely on what they are producing today.

- For people who struggle with huge volatility, bonds still help mitigate the more extreme falls. If you are 60% in stocks and 40% in bonds, your portfolio won’t fall as far during the bad times, but it also won’t soar as much in the good times. Experienced investors learn to not fear volatility though.

- They still have a decent place in a portfolio for people close to retire and are in the preservation phase.

- A small amount, say a 10% allocation, can still make sense for younger people.

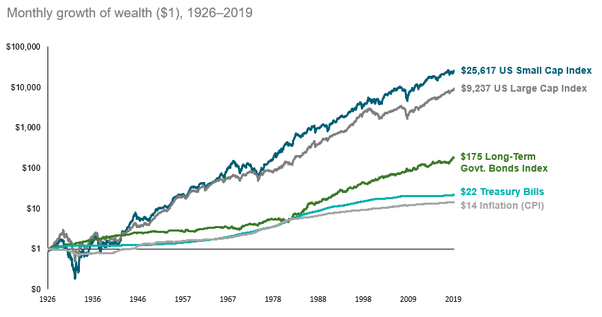

Yet the good quality bonds do pay very little now. What’s more, stock markets (not individual stocks but the whole market) have always beaten bonds long-term:

That meant that it always made sense for younger investors to be light on bonds and heavy in stocks, before going for a 60/40 or 50/50 allocation when they are older.

There was no point in taking risks on alternative, uncorrelated, assets, when bonds could pay 6% per year.

What has changed now is that it is fairly easy to beat government bonds with alternative assets – which can include good-quality corporate bonds.

Especially for people who are more sophisticated, or have access to an advisor, have many smaller alternative investments to partially replace the bond allocation, can increase returns.

Of course, the key is increasing your risk-adjusted return, and not just return, and that takes some thought, skill, research etc.

Will the US stock markets always outperform the foreign market?

I was reading an interesting research paper a few days ago. It spoke about how Canadian investors have behaved in the last few decades.

From 1999–2000 until the Global Financial Crisis of 2008, Canadian stocks thrashed their US counterparts.

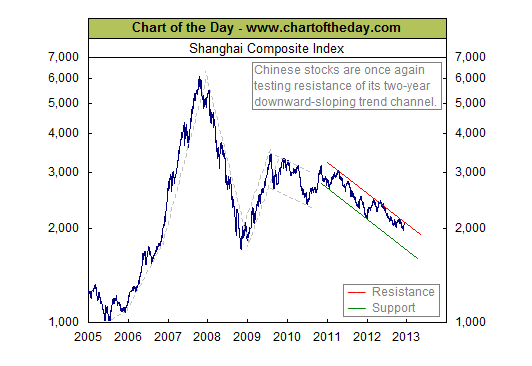

Emerging markets sometimes did even better. Look at how the Shanghai Composite performed. – going from 1,000 to over 6,000 in a short space of time!

During this time, the number of Canadian investors who put 100% of their assets into local stocks skyrocketed, as did the number focusing on emerging markets.

However, this happened after 2008:

US stocks have beaten Canadian ones hands down, and that has continued between 2018 and today.

Now, many Canadian investors are wondering whether they should not invest in local stocks.

I use Canadian investors merely as an example. Similar studies have been done on investors globally.

I am from the UK and see much the same thing. I personally saw people getting into oil and emerging market ETFs and stocks before 2008, and fewer British people wanting local stocks due to the recent performance of the FTSE100 (and even the FTSE250 hasn’t done as well as the Nasdaq and some US indexes).

However, that won’t last forever. It is true that the US markets are some of the best, if not the best, in the world, because they attract innovation from around the world.

Look at all the European, Japanese, and Chinese firms that IPO on the exchanges.

Apple, Amazon, Starbucks and so on also sell more internationally than in the US.

That doesn’t mean, however, that US markets will always outperform. They haven’t beaten international stocks in every single time period historically:

What is true is that US stocks have beaten international ones over most 40–50 year time horizons, but there can be significant periods of time when international wins.

As US stocks have been outperforming for so long, it could be the turn of international stocks to do better.

We already saw that last year. With the exception of the Nasdaq, the other indexes that performed best were previously underperforming exchanges like Taiwan and South Korea.

After reclaiming his title as the world’s richest person, do you anticipate that Elon Musk’s wealth will continue to increase throughout the next five years?

There is a reasonable chance, and indeed there is speculation that he could become the world’s first trillionaire.

However, that doesn’t mean he is the richest person in the world. It merely means he is the wealthiest.

It depends how you define richest really, but I would make a number of points:

1. Unrealized capital gains aren’t the same as realized gains. The media often say that such and such has “lost” or “made” X and Y amounts of money.

That is misleading. What it merely means is that the stock price is fluctuating. If Tesla increases by 10% today, Musk hasn’t made $25 billion in a day.

Likewise, he won’t lose 20 billion when Tesla falls by 10% one of these days. It only becomes a gain or a loss once there are sales.

This isn’t just the case with large sums of money. If your income is 50k, whilst your pension asset soar by 20k and your house goes up by 60k this year, your income remains 50k…..not 130k.

2. The security of the money

There are four types of super-wealthy people

- Those with private companies. Like Trump, and most wealthy people at one stage or another. These are the most difficult assets to value because they aren’t liquid, and finding a buyer is difficult.

- Those with public companies (listed on the stock market). These people have most of their wealth tied to one or two stocks, like Bezos and Amazon or Musk.

- People who gradually moved away from their original business. Bill Gates’ wealth is only partially dependent on Microsoft shares now – it is about 25% of his portfolio. He would have been wealthier today had he kept 100% in Microsoft, but he wanted to diversify, and now has a team managing his investments

- Rulers of countries, like MBS in Saudi Arabia

So, even though on paper somebody like MBS isn’t as “rich” as Musk, he is indirectly richer.

He has more liquid income and a whole country behind him. Even Gates and Buffett are indirectly in a stronger position than somebody like Musk or Bezos, as they have diversified away from one or two companies.

What would need to happen for somebody like MBS to go broke? The whole country would need to go down, and maybe the world economy, considering he probably has money in many countries.

For Gates and Buffett, it would take a lot for their wealth to fall by 99%. That isn’t the case with a founder who has one or two successful businesses, and most of their wealth is linked to that stock.

That doesn’t mean somebody like Musk will suddenly become 99% poorer, but it does mean he is more vulnerable than somebody who has a more diversified portfolio, to unexpected black swan risks.

The point is, the media put out a lot of misleading statistics on this.

Why are most professional football players broke after leaving the game?

I watched a great documentary yesterday from the former Arsenal player Paul Merson.

He lost 7 million Pounds, which is about 12–15 million in today’s money – about $20million.

That is about twenty million USD in today’s money. He mentions how gambling ruined him and many other players.

Gambling often goes together with other vices such as excessive alcohol use, and can indirectly result in divorce.

One of the reasons why people who are earning a lot of money gamble is that there always seems to be fresh money coming in.

Until there isn’t. Professional sports stars tend to earn much less in retirement unless they have a big personal brand or go into management.

That, therefore, means that financial planning is very important. If somebody’s peak earnings are in their 20s and early 30s, planning is essential to make the money last.

Even somebody who was relatively frugal might struggle. Let’s say somebody who has a net worth of $10million on the day they retire.

Realistically, they might be able to get a **safe** income of 400k-500k a year from that.

Very good for most people. Hard to get used to if you got used to tens of millions.

That is one of the biggest reasons why many sports stars, not just footballers, go broke.

A study showed that as many as 78% of former basketball players also become broke, with plenty of boxers like Joe Frazier and Mike Tyson going the same way.

Other reasons are

1. Hangers on. When young people earn a lot of money, they attract the wrong type of people. At a younger age, it is harder for people to judge people as well. People who gradually get wealthier as they age are less likely to make silly decisions.

2. Lack of professional advice. This is changing. Clubs now set up advice, just as the lottery started to do once they saw the problems.

3. One extreme to the other. Many players come from tough, poverty-stricken, backgrounds, and then suddenly make tens of millions.

4. Unexpected events, like early injuries, and not preparing for them financially.

5. Peer pressure. If everybody else is overspending, it is difficult not to be taken in, even subconsciously. You get invited to events and other occasions. Even in a normal office environment, people get influenced by their co-workers. If you share your office with an “everyday millionaire” who got rich slowly, that changes your mentality, compared to being with people who are trying to keep up with the Jones’.

6. Professional players, like business people, are more likely to be risk-takers compared to people who become teachers or doctors. That is good if it is a calculated risk. For some, extreme risks are taken, hence things like gambling.

It isn’t just professional sports stars either. As mentioned, lottery winners often end up broke, as do many inherited wealthy people.

Further Reading

In the article below, I spoke about

- Can people realistically live off dividends in retirement?

- Why are sustainable stocks and ETFs gaining traction and interest?

- What drives private business owners?

- What are the biggest mistakes that small business owners make?

- Was Shark Tank Judge Kevin O’Leary, who I will be interviewing next week on November 2, a skilled businessman or just lucky?

To read more click below